Taking The Keys: A Closer Look at the European Private Credit Market

Key Takeaways

Headline default rates in both private credit and syndicated loans have remained around 2% in 2025. However, these rates understate the stress under the surface. For instance, in broadly syndicated loan (BSL) markets, default rates increase to 4.3% when including liability management exercises—initiatives, such as distressed exchanges, that have historically had a mixed success rate in avoiding outright defaults.1

Data on defaults and liability management exercises is more challenging to come by in private credit. Goldman Sachs Alternatives conducted a proprietary detailed review of credit events noted publicly, specifically insolvencies and debt-for-equity swaps in senior direct lending.2

Often described as "taking the keys," these swaps arise when a borrower can no longer service its debt, or materially breaches loan terms. Lenders then assume partial or full ownership of the company in exchange for reducing its debt. This crystallizes losses for the original shareholders but can stabilize the company by lowering its leverage and giving it a fresh start under new ownership. The outcome for lenders depends on the subsequent trajectory of the company and the lender’s ability to successfully run the company and then sell it.

Our Analysis and Observations

Our analysis of such credit events in Europe offers clues about the magnitude and location of stresses. The data leads to two major conclusions.

Stress events reflect evolving macro environments and underwriting discipline

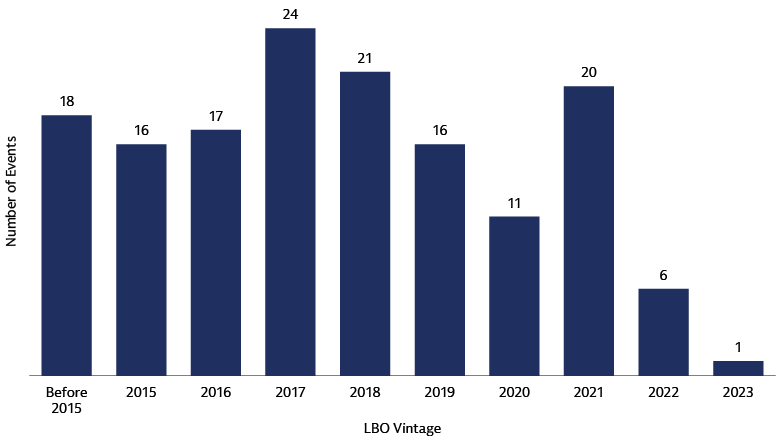

Our research has found 150 European companies representing ~$38 billion of aggregate leveraged buyout (LBO) financings have been subject to credit events since 2017. Four of these have been bankruptcies / liquidations; the rest are debt-for-equity swaps.

However, the timing and underlying vintage year patterns underscore that these events are not random or evenly distributed. Rather, they reflect an evolving macroeconomic backdrop.

Examining the largest pockets of stress shows that LBOs completed in 2017-2018 have been the most vulnerable so far, having had to manage through the disruptions of COVID, inflation, rising rates, Russia/Ukraine conflict and an evolving tariff environment.

Source: Debtwire; KBRA Report, Octus, 9fin, LCD, public information and proprietary sourcing. Note: Analysis includes credit events since 2017.

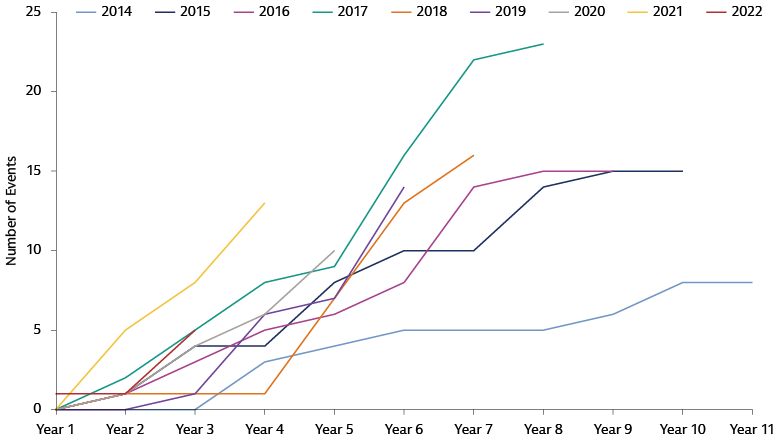

2021-vintage deals are close behind and have seen the steepest trajectory in the number of credit events experienced in the first three years. This vintage may be particularly vulnerable because the loans were structured for a very different rate environment than the one that the borrowers quickly found themselves in. Interest rates rose sharply before many borrowers had time to grow EBITDA enough to offset higher debt service costs.

Source: Debtwire; KBRA Report, Octus, 9fin, LCD, public information and proprietary sourcing. Note: Analysis includes credit events since 2017. Incl. investments which are Sponsor-backed and including LBO cohorts from 2014 only.

While 2023-2025 vintages are not yet seasoned enough for meaningful default events, we expect to eventually see more stress events in these vintages, given the amount of capital managers put to work in this period and a potentially slower path of rate cuts than may have been underwritten in some cases. These deals also featured tighter spreads, providing investors with smaller compensation for credit risk.

Source: Debtwire; KBRA Report, Octus, 9fin, LCD, public information and proprietary sourcing; Note: Analysis includes credit events since 2017.

Stress has not been market wide; rather, it appears concentrated in specific segments of the market

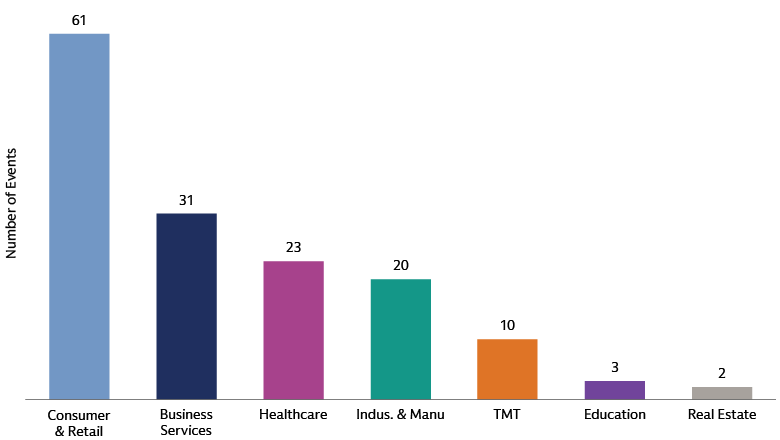

Altogether, the data point to concentrated pockets of stress, among smaller companies and cyclical sectors, rather than to a looming system-wide crisis.

Cyclical industries have been disproportionately affected: consumer, retail, industrials, and manufacturing sectors represent over 50% of all European credit events since 2017.

These companies are often more exposed to shifts in consumer demand, input costs, high fixed operating costs, and broader economic cycles. High leverage can make it harder for borrowers to withstand these types of external shocks.

In the past few years, the stressed companies had to contend with a consumer spending squeeze affecting purchasing power, cost-base inflation, and changing consumption preferences. A sub-optimal capital structure and higher interest expense left some borrowers with a lot less room to maneuver.

Source: Debtwire; KBRA Report, Octus, 9fin, LCD, public information and proprietary sourcing. Note: Analysis includes credit events since 2017.

Healthcare and business services defaults suggest the importance of looking beyond the sector label. For example, IT services are considered non-cyclical on the assumption that IT upgrades or implementation spending are sticky, but in periods of stress companies can delay projects, revealing more cyclicality than anticipated. Some software businesses may be vulnerable to disruption from AI.

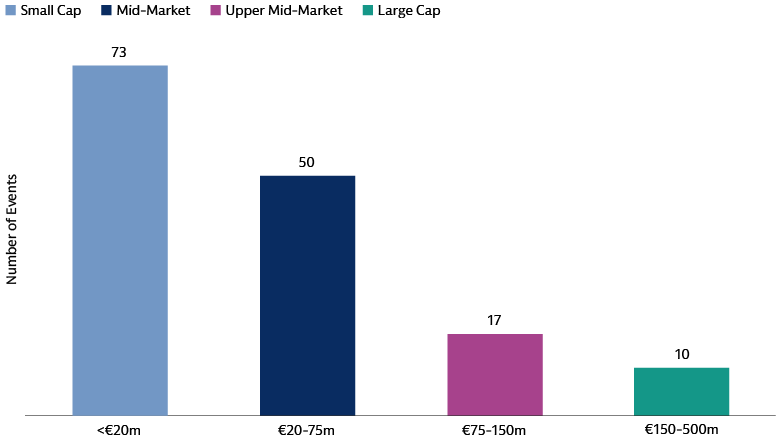

Company size is another key dimension of risk. Small-cap companies (EBITDA <€20m) accounted for close to half of credit events in the dataset; firms generating less than €75 million of EBITDA accounted for over 80%. Smaller companies typically have less pricing power, making it harder to pass on higher costs, and often have less flexibility to absorb shocks (for example, fewer levers to cut costs or diversify revenues). Their access to capital markets and alternative financing options is usually more limited.

Source: Debtwire; KBRA Report, Octus, 9fin, LCD, public information and proprietary sourcing. Note: Analysis includes credit events since 2017.

By contrast, lending to larger, higher-quality companies in less cyclical sectors appears to have provided some insulation against defaults.

The experience of recent years suggests that careful selection along dimensions of both size and sector can significantly influence portfolio outcomes. Yet, a longstanding low-rate, benign macroeconomic environment may have led to an under-appreciation of this dynamic in some cases; a more challenging macroeconomic and geopolitical backdrop subsequently exposed these issues.

One advantage of private credit is the ability to underweight or avoid certain parts of the market, since portfolios are not constrained by public benchmarks. The data in our analysis underlines the importance of this selectivity lever.

Future Market Dynamics and Investment Considerations

We anticipate the rate of credit events to remain elevated relative to the last decade, due to macro and market dynamics and sponsor incentives.

We believe the macro environment should be supportive but not easy for every borrower. Our economists are forecasting 1.0-1.3% real GDP growth in Europe over the next three years, with inflation tracking at 1.8-2% annualized. In the US, after a strong 2026, real GDP growth is forecasted to revert to 2.1% per year, slightly above inflation.3 While this growth is constructive, individual companies’ trajectories should diverge more based on inflation sensitivity and degree of exposure to themes and market sectors vulnerable to disruption from long-term secular trends.

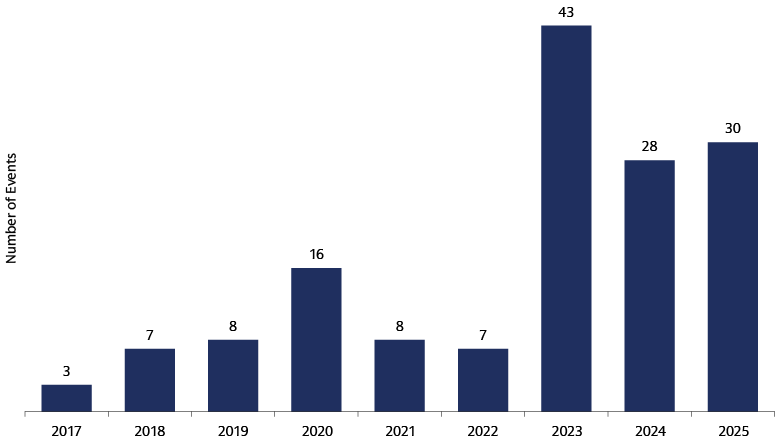

In the past three years, an active refinancing market, driven by strong capital inflows against muted new deal activity, has helped borrowers to manage their financing costs as rates rose, and to extend maturities. However, as the M&A environment recovers, supply of capital should tilt more towards financing new transactions.

Thus far, LBO sponsors of troubled borrowers have generally been willing to engage with lenders on recapitalizations, contributing equity capital where needed. However, if the number of stressed borrowers increases, they may begin making tougher choices, rationing resources and deciding when to hand over the keys.

Implications for LPs

Our data shows that credit events have not been evenly distributed across managers, underscoring the importance of manager selection. Our market views support our belief that manager selection will be even more critical than it would be in a more benign environment.

Understanding the manager’s credit events and loss profiles should be central elements of due diligence. Investment discipline, prudent underwriting, a risk management culture, and workout capabilities are critical to evaluate, especially in an asset class predicated on capital preservation.

Unlike private equity, where strong winners can sometimes offset weaker deals, private credit strategies are generally designed to deliver a relatively fixed return profile with limited upside. Losses from defaults can therefore erode overall performance quickly.

Stress events will also matter for portfolio construction. Converting too many positions from debt into equity alters the fundamental nature of the portfolio, from a fixed income strategy to something that behaves more like equity. If a manager is not structurally set up to manage equity-like positions, this shift can be a significant distraction from the rest of the portfolio. These equity positions also tend to remain on the books longer, complicating investors’ cash flow and liquidity management strategies in private market portfolios.

The recent European experience highlights that the dispersion of outcomes across managers is likely to widen.

With a wider dispersion of outcomes for portfolios may come a wider dispersion of outcomes for GP organizations. If fund performance puts carry at risk, the GP may face morale and motivation issues among team members, making it more challenging to retain top talent.

Manager Selection: Evaluating GPs

We believe the following aspects are critical to examine:

- Length of manager experience: In our view, experience through a full market cycle can give managers an important perspective, and can support deployment discipline, risk management, and workout capabilities.

- Strength and quality of GP pipelines: Strong, diversified pipelines allow managers to be selective and avoid a “race to the bottom” in underwriting and pricing in order to deploy capital.

- Number and profile of credit events relative to the manager’s overall deployment: Stress situations are to be expected in any manager’s portfolio—the spread over base rates is intended to compensate investors for credit risk. However, a higher-than-expected number of credit events is a signal that the underlying selection and underwriting assumptions did not hold up as anticipated. The key question is whether the compensation for the risk has been fair, and whether the manager’s underwriting and portfolio construction processes have been robust enough to keep default and loss rates within acceptable bounds.

- GP’s capabilities in managing and ultimately exiting equity positions acquired through swaps: Taking the keys does not necessarily mean a full write-off. The equity acquired in a restructuring may appreciate in value, and managers can ultimately realize gains through sales or dividends, much like a traditional private equity sponsor. However, doing so requires skill that is distinct from credit underwriting skill. Firms with adjacent private equity units may be able to draw on that expertise to support portfolio companies and maximize recovery values.

Investing globally across the capital structure, Goldman Sachs Alternatives Private Credit platform combines deep expertise and long-standing relationships with sponsors and issuers with the aim to directly originate attractive risk-adjusted return opportunities.

1 Source: Proskauer (private credit), LCD (leveraged loans), as of Q3 2025. Private credit default rate is averaged from quarterly private credit default rates in 2025. Leveraged loans default rate is the LTM default rate tracked by LSTA US Leveraged Loan index. Data on U.S. markets.

2 Goldman Sachs Asset Management built a database aggregating European debt equitization and bankruptcies involving direct lenders (“credit events”) since 2017. The analysis covers both Sponsor and Sponsor-less deals. Credit events are European defaults (i) when a debt restructuring led to into direct lenders taking ownership (partially or fully) of the company they financed or (ii) the company filed for bankruptcy, insolvency or liquidation. Given the private nature of equitizations, the subsequent process to a change of control is largely dominated by out-of-court settlements. There is no guarantee the database captures the complete set of credit events.

3 Source: Goldman Sachs Global Investment Research macro forecast, as of February 20, 2026.