The Fed’s Balance Sheet: What Does it Mean for Money Markets?

Key Takeaways

Kevin Warsh, the new Fed Chair nominee, has consistently outlined his desire to shrink the central bank’s large balance sheet.1 This view—relatively uncommon across current policymakers—could have a sizeable impact on short-term funding and liquidity management for financial institutions and investors.

What is the impact of Fed’s balance sheet on liquidity in the banking system?

The Fed’s balance sheet affects systemwide liquidity via the composition of its liabilities, which fund the Fed’s asset portfolio (primarily US Treasuries and mortgage-backed securities). Within liabilities, deposits by other banks—also known as ‘reserves’—are the major line item over which the Fed has direct control, and amount to almost $3 trillion currently.2 The level of reserves in the banking system directly influences funding markets by influencing rates for securities such as floating-rate notes, as well as rates on repurchase agreements and other front-end assets.

Since 2008, the Fed has operated under an “ample reserves” framework,3 a policy construct designed to keep the level of reserves plentiful enough that small changes in their level will have minimal effect on money market rates.

The result of the shift to the ample reserves framework is a larger balance sheet with assets primarily in the form of government and mortgage-backed securities (MBS).4 The larger asset base has, in turn, meant larger liabilities which, in the form of reserves, have helped to satisfy the banking system’s demand for greater levels of liquidity.

It is important to note that the ample reserves framework differs from another policy goal, quantitative easing (QE). While both are associated with expanded balance sheets, QE is the process of easing financial conditions by directly removing interest rate risk from the Treasury market—by buying longer-dated bonds to push yields down, for instance—therefore encouraging investors to seek higher yielding assets elsewhere, reshaping portfolios and hopefully stimulating economic activity.

How does the Fed’s balance sheet policy impact funding markets?

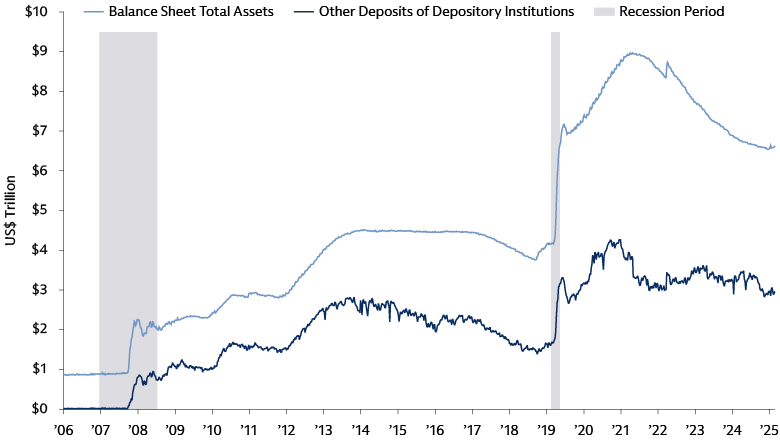

The Fed's ability to purchase assets—or allow them to mature—has a direct impact on the liability side of its balance sheet, namely by either injecting or draining liquidity into the system.

During past crisis periods, the Fed has used its balance sheet alongside lowering the federal funds rate target to help stimulate economic activity.5 This has included growing its asset portfolio through QE, where the Fed purchased trillions in Treasuries and MBS (~$4 trillion from 2008-2014, and ~$4.8 trillion during the COVID-19 pandemic) to ease financial conditions, increasing reserves in the process. Reserves themselves reached an all-time high of more than $4.2 trillion in December 2021.6

The Fed has brought the size of the balance sheet down from its pandemic highs by letting assets mature without replacing them,7 a process known as quantitative tightening (QT). The knock-on effect of this is that the level of reserves in the banking system has decreased:

Source: Federal Reserve Economic Data. As of February 11, 2026

Funding rates remained largely unaffected by this until the fourth quarter of 2025, when upward pressure on benchmark funding rates indicated cash had approached scarce levels.8

How do funding market conditions impact money market fund yields?

Benchmark rates including the Secured Overnight Financing Rate (SOFR) and Triparty General Collateral Rate (TGCR) can rise when reserves in the banking system are low relative to what is required. This most recently occurred in the fourth quarter of 2025, when SOFR-Interest Rate on Reserve Balances spreads reached their highest levels since 2020.9 10

In this type of scenario, money market funds can potentially benefit from relatively higher yields in securities that are more directly linked to SOFR, such as floating rate securities and repurchase agreements.

What is the current path of balance sheet policy?

The Fed announced several balance sheet policy changes at the October and December 2025 Federal Open Market Committee (FOMC) meetings, partly to alleviate funding pressure as illustrated by the quarter’s high SOFR.11 In October, the Fed stopped QT,12 and in December, announced it would buy $40 billion of Treasury bills per month through April 15, 2026.13

To date, these actions have stabilized funding market benchmark rates and helped ensure the system is operating with ample reserves. Other policy changes include renaming the Standing Repo Facility the Standing Repo Program (SRP) to combat stigma and drive usage among banks, as well as eliminating the aggregate limit on standing repo operations to help enhance liquidity during future periods of funding market tightness.

Is it possible that a Kevin Warsh-led FOMC could reshape the balance sheet?

We expect notable balance sheet reduction would take some time should this be one of Warsh’s top priorities, as a combination of committee buy-in and regulatory approval will be necessary.

- Meaningfully reducing reserves will require changes to regulatory policy and enforcement allowing banks to reduce their liquidity on hand.

- We could see more regular use of the SRP, which has generally seen limited use in part due to stigma around institutions borrowing from the central bank.

- Conducting additional open market operations—a process where the Fed will engage in repo transactions with the primary dealer community by either executing repo or reverse repo to add or drain liquidity from the system—could also become necessary, especially around times of funding pressures such as month end.

- In addition, the Fed may look to reduce the duration and alter the composition of its assets, owning a greater proportion of short-term securities (such as Treasury bills) and eventually moving away from owning MBS; however, we expect any such shift would happen gradually and over the course of several years.

Advocates for a smaller central bank footprint likely welcome Warsh's nomination and views on the balance sheet but we expect that building consensus around such a fundamental change to the Fed's operations will take time.

1 Bloomberg, Goldman Sachs Global Investment Research. As of February 2026.

2 Federal Reserve Economic Data. As of February 11, 2026.

3 New York Federal Reserve. As of September 29, 2025.

4 Federal Reserve. As of May 4, 2022.

5 Federal Reserve. As of June 30, 2020.

6 Federal Reserve Economic Data. As of February 11, 2026.

7 Federal Reserve. As of May 4, 2022.

8 Federal Reserve. As of October 14, 2025.

9 Bloomberg, Federal Reserve Economic Data. As of December 31, 2025.

10 Interest on Reserve Balances is the rate at which the Federal Reserve pays interest on funds that eligible depository institutions hold in their accounts at Federal Reserve Banks. A widening spread between SOFR and Interest on Reserve Balances may signify funding stress in the banking system.

11 Federal Reserve. As of October 14, 2025.

12 Federal Reserve. As of October 29, 2025.

13 Federal Reserve. As of December 10, 2025.