Market Pulse August

Macro Views

Globally we expect GDP growth to slow in 2026 amid lingering headwinds from the rise in energy prices. In the US, we see growth near 2% with the AI boom supporting business investment and contributing nearly 0.5pp to consumer spending through equity wealth effects. We see AI-driven above trend growth in EMs as well, but below-trend growth in developed markets ex-US.

Core inflation has undershot in recent months and now stands at 2.1% in the G10 ex-US, despite energy prices surging in March. In the US, we expect core inflation closer to 3% in Dec 2026 given the effects of tariffs, energy prices, and AI measurement issues, with it falling closer to 2% in 2027 as those subside.

The usual rationale for raising rates is to prevent economic overheating by bringing aggregate demand into balance with supply. The challenge for central banks today is that most inflation is supply driven and rate policy becomes a less effective tool. As such, we expect the Fed to hold for evidence of price passthrough and the Bank of England to watch the labor market, while the European Central Bank may still hike in September to guard inflation expectations.

Source: Bloomberg and Goldman Sachs Asset Management. As of July 31, 2026. Past performance does not predict future returns and does not guarantee future results, which may vary.

Market Views

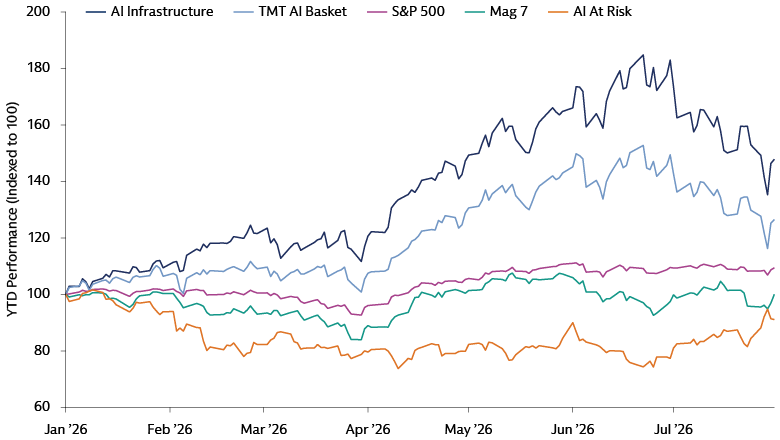

From a top-down perspective, index performance has been strong this year and global markets are within striking distance of all-time highs. Under the surface, rapid rotations have challenged portfolio stability. AI has been at the epicenter, with trade-offs emerging between software vs hardware and hyperscalers vs infrastructure providers. Low correlation and high dispersion markets are ideal conditions for alpha generation, in our view, with a preference for quality earnings and balance sheets.

Significant AI capex requires a mix of financing, with hyperscaler issuance accounting for 16-23% of gross issuance in USD IG, HY, and leveraged loan markets YTD, and a growing share of non-USD and private markets as well. Technology spreads have widened, in part reflecting heavy supply, but credit fundamentals appear reasonable – particularly for the top of the capital stack.

The sharp increase in US rates and strong US equity performance has given legs to the dollar rally, even as geopolitical and energy risks have normalized. We expect divided dollar performance to continue, with strength to be more pronounced against DM than EM currencies given strong EM equity performance and relatively higher yields.

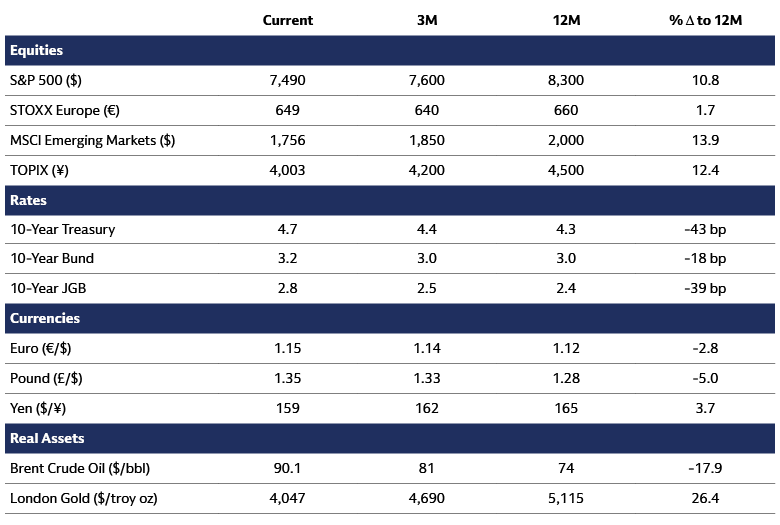

Asset Class Forecasts: Price targets of major asset classes are provided by Goldman Sachs Global Investment Research. As of August 3, 2026.

AI Job Apocalypse or Labor Transformation?

Generative artificial intelligence may be a new technology, but disruption is not a new phenomenon. Similar to past periods of innovation, we believe that AI will increase productivity, change the way we work, and transform the labor market. There will likely be disruption, but we are already seeing potential across companies and economies. GS Research estimates that widespread adoption of AI may increase labor productivity by ~15% over 10 years, contributing to a $7tn increase in annual global GDP.

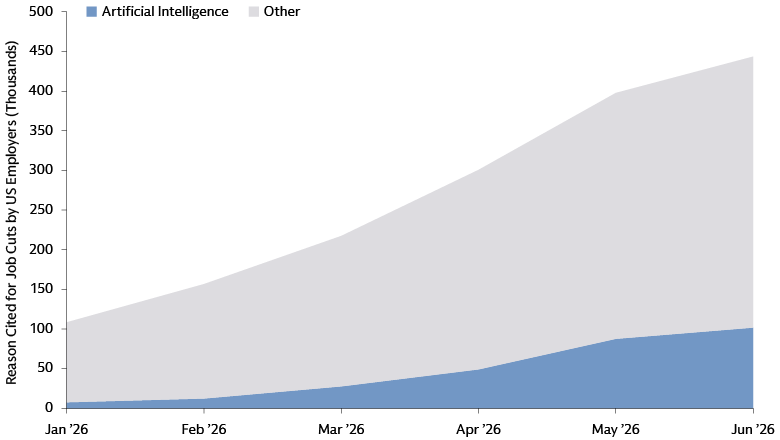

Source: Challenger and Goldman Sachs Asset Management. As of June 30, 2026. Chart shows the cumulative 2026 job cuts, grouped by reason according to data from Challenger, Gray & Christmas.

As AI capabilities improve, we are beginning to see examples of AI-related job losses in the US. This year, employers have cut 444k jobs and cited AI as the reason in 23% of cases. However, that number likely includes both the roles and the budgets that have been replaced by AI. We estimate that over time 7% of jobs are likely to be displaced, but leading AI labs have suggested that the technology can do just 2-3% of all jobs today.

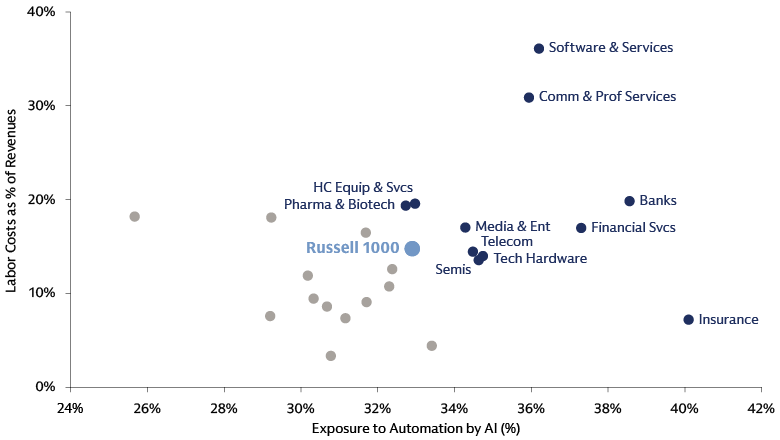

Source: Goldman Sachs Global Investment Research. As of December 31, 2025. Chart shows the estimated exposure to automation by AI and labor costs as a percentage of revenues for sectors in the Russell 1000 Index, and for the median company in the index.

We believe the majority of jobs are likely to be complemented by AI, though some sectors may be more exposed than others. Roles with defined tasks in predictable environments are more likely to be substituted, while industries involving data, problem solving, and human elements are more likely to be augmented. Here, technology, financials, healthcare, and service sectors stand out to us as potential long-term AI beneficiaries. We assume a 10-year timeline, with faster adoption causing more disruption.

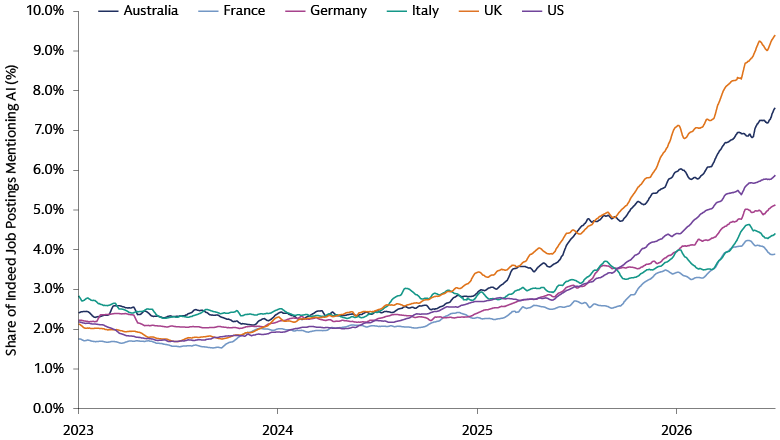

Source: Macrobond and Goldman Sachs Asset Management. As of June 30, 2026. Chart shows the share of Indeed job postings that mention AI across different countries.

As in past periods of innovation, we believe that AI will ultimately reshape the labor force. For example, roughly 60% of workers today are employed in occupations that did not exist in 1940. Already we are seeing AI create new roles and requirements, with the share of job postings mentioning AI increase meaningfully in the last year. This has been particularly true in service economies such as the UK, Australia, and the US, though we also expect a pickup in trade jobs related to data center construction.