Tech Pulse Check: Themes in Focus and Future Opportunities

Key Takeaways

Earlier this year, we shared our outlook for tech equity and highlighted areas that may present opportunity. After an eventful first half of 2025 and a robust 2Q earnings season, this article serves as a pulse check on tech, featuring our investment views on key themes and future opportunities—from semiconductors to fintech—as well as observations on earnings and valuations. Overall, we believe the technology sector continues to demonstrate resilient growth, driven by the secular AI trend, with strong earnings and continued innovation setting the stage for further gains.

Tech Themes in Focus

No slow down for smart components

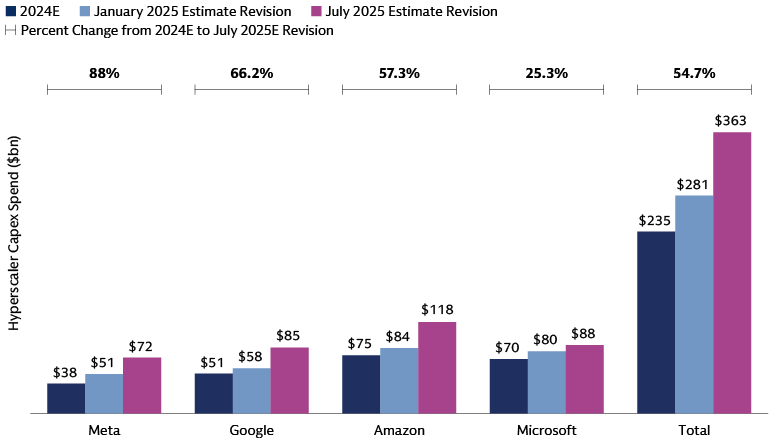

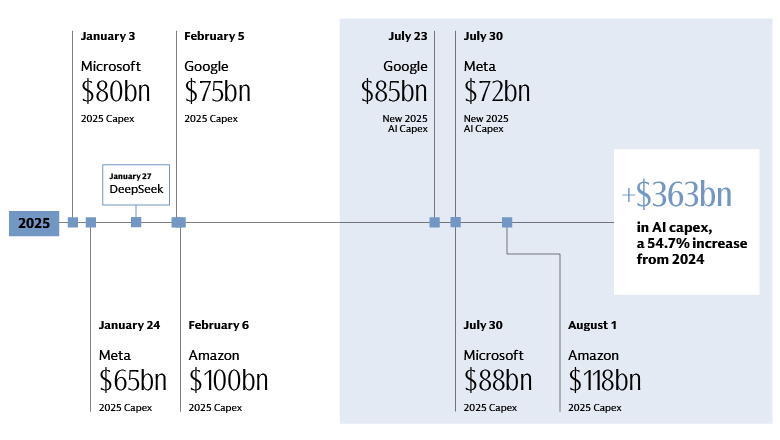

Driven by the accelerating adoption of AI and a global movement towards supply chain resiliency, 2025 is seeing surging demand for semiconductors. This is fuelling unprecedented investment in chip design, fabrication, and supporting technologies. The need for both high-performance chips for AI training and robust inference infrastructure is expected to continue the data center buildout well into 2026, potentially exceeding current capital expenditure (capex) estimates. Smart components, particularly in the semiconductor sector, remain critical to technological progress, and are poised for sustained growth as the essential backbone of the digital economy.

Source: Goldman Sachs Asset Management. Bloomberg, consensus estimates as of Jul-2025. Note: Microsoft capital expenditure numbers includes capital leases. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. There is no guarantee that objectives will be met. Diversification does not protect an investor from market risk and does not ensure a profit.

Source: CNBC, Bloomberg, Apple, TSMC August 2025. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance the forecasts will be achieved. Please see additional disclosures at the end of this presentation. Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities. There is no guarantee that objectives will be met. Diversification does not protect an investor from market risk and does not ensure a profit.

Digital transformation and the importance of data

We have entered a new era of digital transformation, powered by Agentic AI systems that are enhancing enterprise software. These intelligent agents autonomously streamline business processes, make data-driven decisions, and identify operational improvements, orchestrating end-to-end workflows. We believe the full potential of Agentic AI, however, hinges on robust data management practices, making effective data governance crucial for performance, trustworthiness, and compliance. Data is increasingly becoming a critical layer for differentiation at the frontier model level, complementing hardware advancements in the race for Gen AI dominance.

AI’s expanding influence on consumer internet

AI's rapid advancement and integration are reshaping the consumer internet sector, impacting advertising, gaming, social media, and e-commerce. AI-driven algorithms provide hyper-personalized advertising, transform gameplay and development, enhance content curation and user safety on social media, and revolutionize e-commerce with smarter recommendations and predictive analytics. We maintain a bullish outlook as AI's expanding influence continues to supercharge connectivity, engagement, and value creation.

Cybersecurity a critical concern for corporates

Cybersecurity remains a critical concern for companies due to increasingly sophisticated and pervasive AI-powered cyberattacks. Organizations are investing in zero-trust architectures and advanced threat intelligence to defend against complex risks, while regulatory scrutiny continues to rise. We are bullish on cybersecurity as a foundational sector that underpins trust and operational continuity across all industries in a digital-first world.

Leading-edge semi-cap equipment

Leading-edge semiconductor capital equipment (semi-cap) is a linchpin of technological progress and supply chain resilience. Demand for advanced tools has surged globally as chip sizes shrink and complexity rises. The strategic focus on domestic production capabilities, amplified by government policy and industry investment, is driving robust growth and innovation. We are bullish on this segment which provides critical infrastructure for the digital economy and potential competitive advantages for select countries.

Fintech at the forefront of innovation

Fintech is at the forefront of financial inclusion and innovation. Open banking, embedded finance, and decentralized finance (DeFi) platforms have expanded access to various financial tools. AI-driven risk assessment and personalized financial solutions are enhancing transparency and efficiency, while the evolution of digital currencies and regulatory frameworks continues to reshape the sector. We are confident in fintech's adaptability and its crucial role in democratizing finance for consumers and businesses alike.

Tech Earnings Takeaways

Overall, the technology sector had a 2Q 2025 strong earnings season. The above themes remain healthy with room to grow.

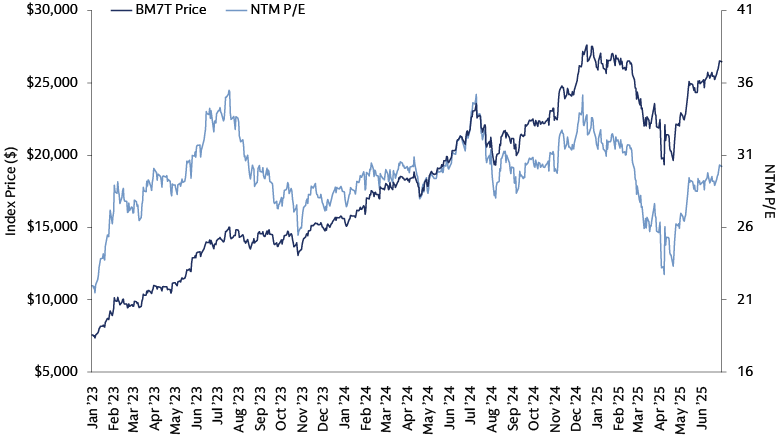

Magnificent 7

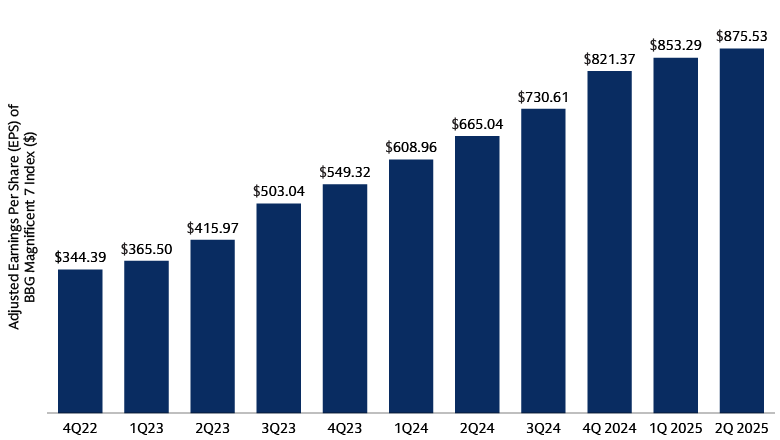

The Magnificent 7 delivered impressive 2Q 2025 earnings, primarily driven by the strength of their core businesses rather than solely new AI features. Future growth remains heavily reliant on AI, with significant investments in AI infrastructure by hyperscalers. However, as fundamental investors, we believe it is crucial that core businesses remain robust, particularly as these companies aggressively invest in AI technology.

The Magnificent 7 has largely been a homogenous group in terms of stock price performance since 2023, due to excitement around AI. However, key points of debate are now emerging that are expected to drive dispersion among them going forward. These include questions surrounding whether their core businesses are genuinely enhanced or possibly cannibalized by AI, and whether AI investment is driven by strengthening existing market leadership or the need to find new markets. Additionally, their strategic position as frontier model builders versus reliance on partnerships with model builders will have important consequences. This necessitates deep research and active management to navigate potential risks and opportunities within this group of companies.

Software

As seen with the Magnificent 7, cloud software infrastructure providers have experienced substantial growth in their core businesses, propelled by the continued shift to cloud infrastructure. This includes the major cloud providers, but beyond these, data management and cybersecurity companies continue to exhibit strength. This area is a critical facilitator for the broader AI transition and has contributed to the growth of software infrastructure providers.

The enterprise and application software segment has continued to struggle year-to-date, primarily due to concerns around how AI might negatively impact the future growth of these businesses or potentially make enterprise software obsolete altogether. This is a key area of debate in the market and the uncertainty has been a headwind for companies in this area. In our portfolios, we are focused on investing in established enterprise software platforms where utilization of services remains high and growth is still intact, while avoiding companies with less scale where customer acquisition will likely be tougher moving forward.

Semi-cap

Despite some downward share price movements observed in the semiconductor and wafer fabrication equipment markets earlier in the quarter, our long-term outlook for the space remains positive. We anticipate a greater divergence among semi-cap names going forward, based on their exposure to specific customers and end markets. KLA Corp and Lam Research reported strong quarters due to their higher quality customers and technology versus Tokyo Electron. We favor exposure to AI-driven end markets, including leading-edge chips, high-bandwidth memory, process control, and exposure via capital expenditure to companies like TSMC.

Consumer

Leading consumer platforms such as Meta, Netflix, and Spotify, are continuing to expand in size. In our view, dispersion between market leaders and fringe players in this segment is likely to widen. Dominant platforms are leveraging their scale and vast user data to train their AI models, thereby extending their competitive advantage. This strategic utilization of AI has fostered a durable "flywheel" effect for the leading players, which we expect to persist over the long term.

Observations on Tech Valuations

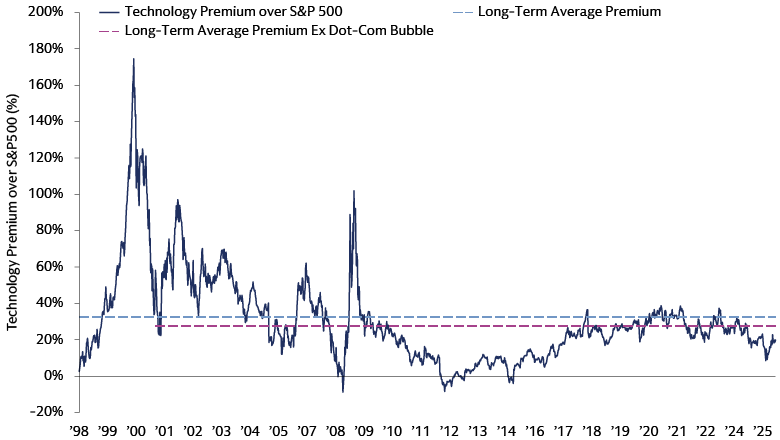

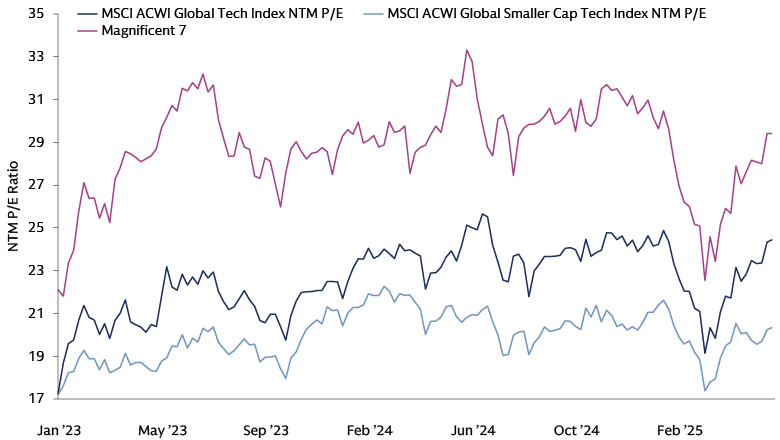

Despite the significant returns delivered by the technology sector over the past three years, current valuations suggest that tech is still trading at a lower premium to the S&P500 relative to long-term averages. In our view, the robust earnings power of the largest tech companies within the index provides near-term support to current valuation levels. In addition, while these mega-cap tech companies have dominated recent returns, we anticipate a broadening of performance across the tech sector. Specifically, companies further down the market capitalization spectrum may present a more attractive long-term opportunity for investors seeking technology equity exposure. By focusing on high-quality businesses, maintaining balance, and being disciplined around valuation, we believe investors can capitalize on this opportunity and generate alpha versus the broad market. We illustrate these points below.

Source: Factset. As of July 31, 2025. The above data looks at P/E ratios to create a percentage estimate of the difference (premium) between tech valuations and broader S&P500 valuations.

Source: Bloomberg. As of June 30, 2025.

Source: Bloomberg. As of June 30, 2025.

Source: Factset. As of June 30, 2025.

Looking Ahead

Investors have a unique opportunity to invest in innovative tech companies at attractive valuations. While short-term factors like consumer health, enterprise spending, and geopolitical tensions warrant monitoring, the long-term outlook for technology is robust, primarily driven by AI, which is expected to drive significant economic growth. Technology innovation is providing solutions and improvements across all sectors, offering secular growth opportunities. In the environment of increased volatility and uncertainty, deep research and active management becomes crucial for navigating market shifts and identifying quality companies. Companies demonstrating strong free cash flow generation and earnings growth are well-positioned to outperform, leading to continued growth for the tech sector this year and beyond.