The Japanese Paradox: A Systematic Path to Alpha

Key Takeaways

Homogeneity on the Surface, Asymmetry Under the Hood

Japan is the world's third-largest equity market by capitalization. It also represents one-fifth of the MSCI World ex-US Index, and the exposure is consistently the largest within that benchmark.1 On the surface, Japan is a distinctly homogeneous market. However, unlike fragmented Europe, where multiple jurisdictions, exchanges, and languages create complexity, Japan’s equity market operates under a single governmental and regulatory framework, controlled by a single exchange (the Tokyo Stock Exchange), and unified by one language and culture. Yet this simplicity disguises a deeply contrarian and informationally asymmetric market that sets Japan apart from other developed economies. Japan moves to its own contrarian investment rhythm, showcased by its often-distinct monetary policy direction, market reactions to macroeconomic developments, factor performance, and investor behavior. We believe this creates rich alpha potential, and provides opportunities for quantitative approaches with the resources to bridge linguistic and informational gaps, transforming "unseen" data into an informational edge.

Distinct Market Characteristics and Structural Tailwinds

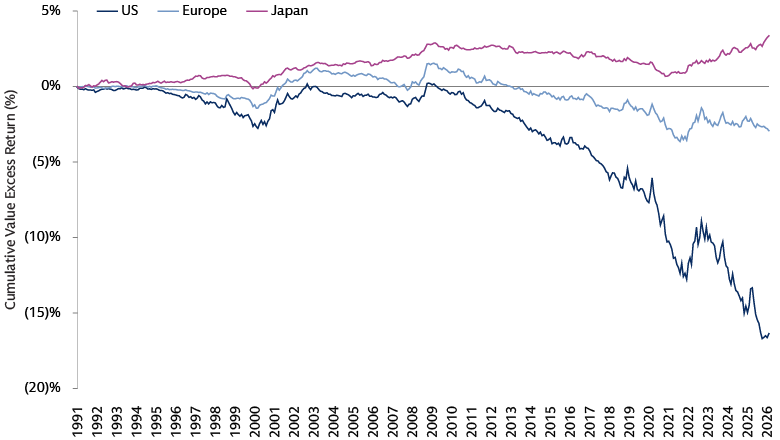

Japan differs from other markets in global factor performance, and we believe understanding this contrarian DNA is essential for capturing alpha. Relative valuation strategies—particularly those based on price-to-book (P/B) ratios—have historically delivered stronger, more persistent returns in Japan than in the US and Europe, where value-based factors have cumulatively underperformed since the 2000s. More recently, since the COVID-19 pandemic, Japan has experienced a renewed rotation toward value, contrary to the US and Europe. This trend has been reinforced by the TSE’s corporate governance reforms, which pressure companies trading below book value to improve capital efficiency, attracting value-oriented capital and potentially creating a structural tailwind for valuation-based strategies.

Source: Goldman Sachs Asset Management, Fama French. Data from January 1,1991 to February 1, 2026. For illustrative purposes only. Past performance does not guarantee future results, which may vary.

Conversely, conventional price momentum strategies have faced challenges in Japan. While trends exist, they tend to differ from traditional conceptions of momentum and revert more quickly, a dynamic likely tied to the market's contrarian nature and the fragmented behavior of its diverse investor base. Value and momentum are largely uncorrelated in Japan, dispelling the myth that momentum is entirely absent; rather, the opportunity lies in understanding how trends manifest and reverse, which we believe requires a more nuanced, data-driven approach.

Japan's macro landscape is also distinct. For decades, Japan maintained ultra-low and negative interest rates while other developed economies tightened, fueling the yen’s carry trade and reinforcing the currency’s safe-haven status. Notably, the Bank of Japan (BoJ) directly purchased equities through ETF buying programs. Following years of negative rates while other markets tightened, Japan’s more recent shift toward policy normalization has triggered equity market reactions that contrast sharply with those seen in response to similar actions by the US Federal Reserve or European Central Bank.

These dynamics coincide with strong earnings momentum. A weak yen and ongoing business restructuring have pushed corporate profits to record highs. Consensus bottom-up estimates of EPS growth in FY 2026 stand at 13% (compared to 14% for S&P 500 and 11% for STOXX 600). Navigating the normalization of the yen carry trade now requires sophisticated risk management.2

Overcoming a Wall of Inefficiency

We believe the informational asymmetries inherent in Japan’s equity market provide a fertile landscape for alpha generation. These inefficiencies stem from equity analyst coverage gaps, language barriers, and a fragmented investor base with divergent behaviors, alongside a vast base of alternative and unstructured data with asymmetrical access. We believe these dynamics form a moat that separates investors with the tools to access Japan's full information ecosystem from those without.

The coverage gap

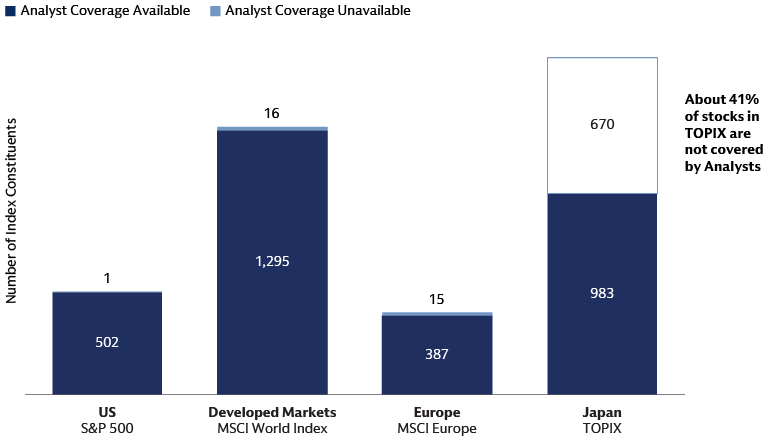

Analyst coverage in Japan is markedly lower than in other developed markets, with a considerably large portion of the market having zero coverage, and with a skew toward the largest stocks. The median number of analysts per stock in the S&P 500 is around 24, and 19 in the MSCI Europe, while in Japan, it drops to as low as 1 for the TOPIX. Notably, 40% of stocks in TOPIX are not covered by any analysts at all, a figure visibly higher than other developed market benchmarks, where the majority of stocks are covered.3 This coverage gap means that a vast portion of Japan's equity market, particularly in the small- and mid-cap segments, operates with limited external scrutiny, creating persistent mispricings that quantitative strategies can potentially exploit.

Source: Goldman Sachs Asset Management, Bloomberg. Proportion of availability of any analyst coverage per stock in the respective benchmark universe. For illustrative purposes only. Index constituents' data are as of March 31, 2026. Analyst coverage data are as of April 16, 2026. The Japan TOPIX Index Value and the Japan TOPIX Marks is subject to the proprietary rights owned by JPX Market Innovation & Research, Inc., or affiliates of JPX Market Innovation & Research, Inc. (hereinafter collectively referred to as "JPX") and JPX owns all rights and know-how relating to Japan TOPIX such as calculation, publication and use of the Japan TOPIX Index Value and relating to the Japan TOPIX Marks. JPX shall not be liable for the miscalculation, incorrect publication, delayed or interrupted publication of the Japan TOPIX Index Value.

The language barrier

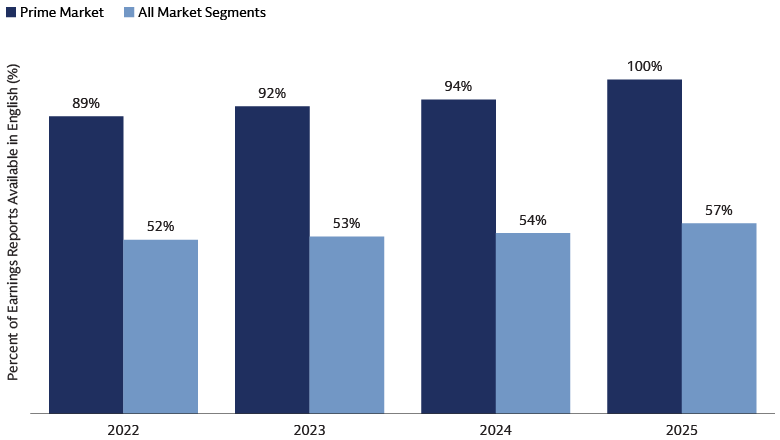

An estimated 96% of the Japanese workforce operates primarily in Japanese, and this linguistic homogeneity penetrates every layer of the market's information ecosystem.4 Japan offers three different accounting standard options (Japanese GAAP, US GAAP, and IFRS), and only companies reporting under US GAAP or IFRS are likely to provide English-language disclosures, which is a small minority of the total universe. Sell-side research is heavily controlled by domestic brokers, whose reports are mostly in Japanese and tailored to domestic reporting conventions. Credit agency reports, local news, and corporate communications are predominately in Japanese. In 2024, only 54% of Japanese earnings reports were available in English, effectively making nearly half the market—mostly small- and mid-caps—difficult for global capital to penetrate. While 90% of the large-cap prime market firms provide some English disclosures, these often lack the depth and nuance of the original Japanese filings. This creates a considerable barrier to entry for international investors, effectively ring-fencing a vast pool of market-moving information from the global investment community.

Source: Japan Exchange Group. Based on news article: Results of the English Disclosure Implementation Status Survey. As of the end of December 2025. Data represents the proportion of Companies Disclosing Earnings Reports in English (based on number of companies) within the Market segment, as of FY end 2025.

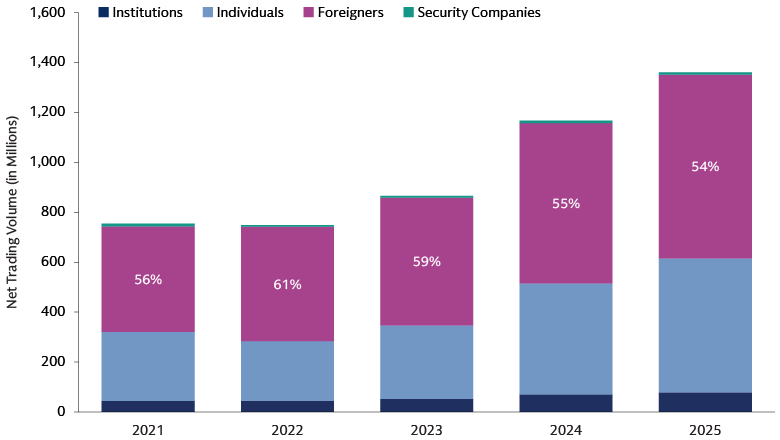

The fragmented investor base

Japan’s market features a fragmented investor base with conflicting motivations. While domestic investors hold most assets, they trade infrequently with a passive, home-biased approach. Conversely, foreign institutional investors—accounting for over 54% of trading volume—act as the marginal price setters. This creates a distinct friction: momentum-driven foreigners focus on large-caps with English disclosures, while contrarian domestic players take the opposing side, triggering sharp reversals. We believe this environment favors systematic, data-driven strategies over traditional fundamental management.

Source: Goldman Sachs Asset Management, Japan Exchange Group. Net Total Trading Volume of Stocks (Net of Sales and Purchase of Shares) of Brokerage Traders in Tokyo & Nagoya markets. https://www.jpx.co.jp/english/markets/statistics-equities/investor-type/00-02.html

The alternative data frontier

Japan has a remarkably rich alternative data ecosystem. Data includes Japanese-language local news and media sources, business and cross-shareholding data, patent documents, employee review datasets, TSE stock selection and governance data, and other unstructured text sources. Most of this alternative data is only accessible in Japanese, meaning that investors without dedicated Japanese-language data processing capabilities are effectively locked out of these insights.

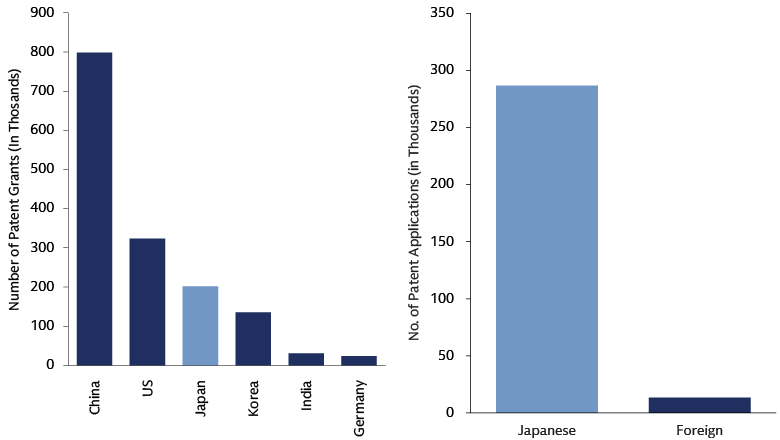

Japan's position as a global leader in patent filings is an example of the alternative data opportunity. Japan consistently ranks among the world's top patent filers, with +300,000 patent grants in 2024 (the third highest globally, behind China and the US), potentially offering a window into corporate innovation that is largely inaccessible without Japanese-language processing capabilities.5 Most of the patent filings are in Japanese, underscoring the extent to which this rich data source is gated by language.

Source: Goldman Sachs Asset Management. LHS: World Population Review. As of December 2023. Dataset does not include patents submitted via intragovernmental collectives, such as the Eurasian Patent Organization or the African Intellectual Property Organization, as those patents are not traced back to a single country by the World Intellectual Property Organization. Countries with most Patent grants are only shown. RHS: IPStart. During 2023, a total of 300,133 patent applications were filed in Japan. Countries that filed patent applications in Japan include Japan, US, China, Korea, Germany, and more. Data as of end of 2023.

A Quant Edge in Japan Can Provide a Path to Alpha

Japan’s equity market offers abundant alpha potential due to deep informational asymmetries and distinct contrarian dynamics. However, traditional fundamental analysis may struggle with language barriers and the sheer scale of the under-covered universe. We believe quantitative strategies are uniquely positioned to turn these complexities into a systematic advantage.

Overcoming the information barrier at scale: Quantitative models can process Japanese-language datasets at a scale impossible for human analysts. By utilizing Natural Language Processing (NLP) on over 290,000 analyst reports and 20,000 earnings call transcripts, quants can detect sentiment shifts before they are priced in. Furthermore, analyzing alternative data, such as 50 million patent filings, provides proprietary insights into company valuations and emerging thematic trends.6

Mastering more nuanced market dynamics: Global "one-size-fits-all" models fail in Japan. Successful quantitative managers use historical data to calibrate models to the market's specific "contrarian rhythm." While generic price momentum often struggles, proprietary systematic approaches can identify emerging themes, such as corporate governance improvements, well before they reach consensus.

Systematically capitalizing on ongoing structural reforms: The Tokyo Stock Exchange (TSE) reforms targeting capital efficiency represent a large structural catalyst. Quantitative strategies systematically screen the entire market to identify potential reform beneficiaries early, providing a scalable way to capture upside from corporate governance shifts.

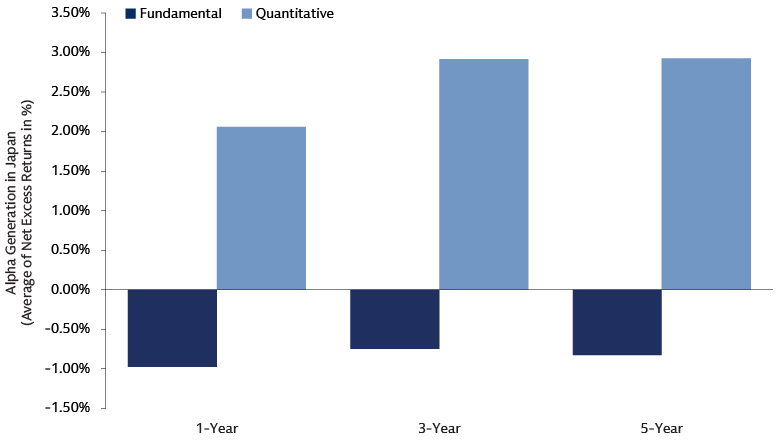

The data-driven edge in performance: Empirical evidence supports a data-driven approach. According to eVestment, quantitative strategies in Japan have historically outperformed both passive and fundamental peers across various time horizons, proving that systematic tools are essential for navigating this complex landscape.

Source: Goldman Sachs Asset Management, eVestment. As of March 31, 2026. Returns are based on Base currency. Under primary investment approach, only quantitative and fundamental strategies are used. Primary universe is All Japan Equity. The average annualized excess returns are computed for each time period across all presented universe. Figures above are arithmetic averages for those groups. Data excludes funds with simulated results or incomplete histories. Past performance does not predict future returns and does not guarantee future results, which may vary.

Turning Obstacles into Advantages?

As we’ve outlined, Japan's equity market is a compelling paradox: a homogeneous system characterized by deep contrarian dynamics and significant informational asymmetries. These characteristics provide investors with distinct factor positioning, and exposure to differentiated local growth drivers and structural tailwinds. The prevalence of the Japanese language and the divergent behaviors of domestic versus foreign investors also may create a high-alpha environment that remains difficult to navigate using conventional fundamental methods. For quantitative investors with the ability to capitalize on Japan’s rich alternative data ecosystem, we believe inefficiencies can transition from obstacles into potential advantages and paths to alpha.

1MSCI. As of April 30, 2026.

2I/E/B/S. MSCI. Toyo Keizai. Goldman Sachs Global Investment Research. As of April 2026.

3Bloomberg. Index constituents. As of Mar 31, 2026. Analyst Coverage Data. As of April 16, 2026.

4Hashimoto, Yuki, Policy Research Institute, Ministry of Finance, Japan, Public Policy Review, Vol.21, No.4, January 2026. As of 2023, foreign workers—who may operate in other languages—account for only 3.4% of the total workforce (approximately 2.05 million people)

5World Population Review. As of Calendar Year 2024.

6Goldman Sachs Asset Management, as of March 31, 2026.