Allocating Excess Liquidity Within a Portfolio

A bank working under International Financial Reporting Standards 9 (IFRS 9) looking to develop a five-year allocation strategy.

Design a five-year allocation strategy focused on building a high-quality liquid asset portfolio (HQLA) and an excess liquidity allocation, all while managing the consumption of risk-weighted assets (RWA).

- Maximize credit spread generation under RWA constraints.

- Remain mindful of profit and loss volatility under IFRS 9 financial reporting standards.

- Remain mindful of downgrade risk and its impact on RWA.

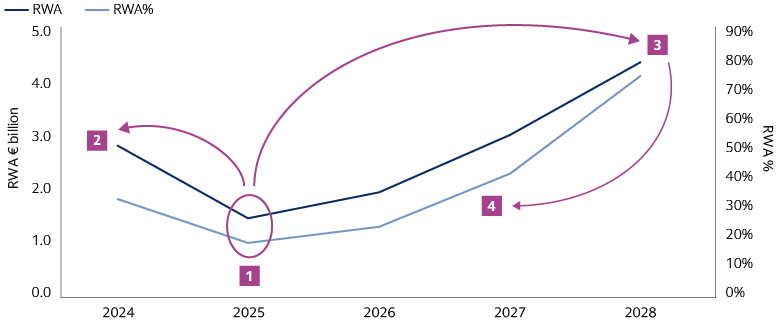

We opted to prioritize Buy & Maintain strategies with low levels of required turnover, given the bank’s focus on profit and loss management control. Anchoring the investment strategy to the lowest RWA budget of Year 2, we employed the following approach:

- We solved for the Year 2 target allocation, where the risk-weighted asset constraint is tightest.

- We planned a Year 1 allocation that would roll forward to the desired Year 2 allocation on a buy-and-maintain basis, allocating the excess liquidity to assets with maturity 0-1y.

- We solved for the Year 5 allocation, which would utilize the larger risk-weighted asset budget while minimizing turnover from the Year 2 allocation.

- We finally derived the Years 3 and 4 allocations as transitions towards the Year 5 allocation.

Our portfolio construction approach focused on the shorter-term Year 2 allocation needs, as well as plotted a course to the future Year 5 requirements. This was based on the following modelling assumptions and five-year target allocation:

- We included components of RWA assuming all assets are part of the banking book, and estimated the impact that a one-letter credit rating downgrade on all securities would have on RWA

- We measured economic risk in terms of annualized mark-to-market volatility, annualized spread volatility (excluding rates), and expected credit losses over the lifetime of the positions, assuming long-term rating migration matrices.

- We designed the allocation to minimize the need to sell securities before maturity, meaning the volatility of IFRS 9 profit and loss was mostly driven by the variability of income over time and the mark-to-market of the securities accounted for under fair-value through profit and loss.

- We focused our Year 1 target allocation on the stability of the allocation and on investing additional excess liquidity in Emerging Market Debt and High Yield.

- For the Year 2 target allocation, we looked towards core government exposures, high-quality covered bonds, and high-quality securitizations.

- We leveraged the maturity profile of the Year 2 allocation to fund the redemption profile, rotating the portfolio towards higher-yield assets and making use of the larger RWA budget for the Years 3-5 target allocation.

The cited case studies represent examples of how we have partnered with various institutional clients on a broad range of services and offerings. The experiences outlined in the case studies may not be representative of the experience of other clients. The case studies have not been selected based on portfolio performance and are not indicative of future performance or success. This is not a testimonial for Goldman Sachs Asset Management’s advisory services.