The ETF Effect: How Exchange-Traded Funds Are Transforming Fixed Income

Key Takeaways

We believe exchange-traded funds are revolutionizing fixed income, from the way investors access the market to the plumbing that makes it work. Since their debut in 2002, fixed income ETFs have helped remove barriers to investing in this fragmented market, providing flexible, cost-effective tools for expanding and managing fixed income exposure. Along the way, these funds have driven the streamlining of fixed income market structure, leading to improvements in price discovery and trading efficiency. Fixed income ETFs have proven their value as a source of vital liquidity during periods of market stress. They have opened up parts of the market, such as collateralized loan obligations (CLOs), that once were beyond the reach of many investors.

For investors, ETFs’ impact on fixed income can be seen in lower costs, the flexibility of intraday trading, and the broadening of investment options and use cases. These potential benefits have become possible thanks to a rapid evolution of the machinery of fixed income trading that has reconciled a highly liquid, stock-like investment vehicle with an often opaque market where many securities are thinly traded and most transactions are still over the counter. To explain the evolution of fixed income investing in the ETF era and how the market may change further in the years ahead, we called on specialists from Goldman Sachs’ Global Banking and Markets division and Goldman Sachs Asset Management.

Efficiency and Access: The Evolution of the Fixed Income Market

Fixed income markets have evolved significantly in recent years, propelled by the growth of electronic trading, portfolio trading, and credit derivatives. These changes have increased the liquidity and accessibility of fixed income, improved price discovery and transparency, and contributed to the trend of bond markets functioning increasingly like equity markets.

Traditionally, fixed income trading revolved around dealers – large banks or securities houses – and their networks of customers, including other banks, asset managers, corporations, and insurance companies. Trades were executed over the counter (bilaterally) without the sort of centralized exchanges found in equity markets. The parties in a trade typically negotiated terms by telephone or electronic chat, and the process of matching buyers and sellers involved the expenditure of significant time and money. Customers seeking to buy a bond had to contact dealers individually to inquire about price and availability.

This began to change in the late 1990s with the advent of electronic trading, including multi-dealer platforms that allow investors to request quotes from multiple dealers at once. This effectively puts dealers in competition with one another to fill a transaction and tends to reduce the costs for investors compared with seeking quotes one at a time. Platforms based on this request-for-quote (RFQ) system have also brought down costs by automating the processing and settlement of trades. By lowering costs, increasing transparency, and streamlining price discovery, electronic trading has helped boost fixed income market liquidity.

A second innovation that has revolutionized fixed income markets is portfolio trading, in which investors buy or sell bundled assets in an all-or-nothing package deal. This mechanism, which was developed by electronic fixed income trading platforms, has increased the speed and efficiency of transactions. Rather than trading one bond at a time, portfolio trading powered by algorithms enables transactions involving hundreds or even thousands of bonds at once, reducing costs. For investors, portfolio trades have become an efficient way to rebalance portfolios and manage liquidity and risk.

Electronic and portfolio trading are the technological advances that underpin the fixed income ETF market. They provide the foundation for the creation/redemption mechanism in the ETF primary market, where transactions involve customized bundles of securities that must be priced and traded quickly and efficiently. These mechanisms also support liquidity and transparency in the ETF secondary market. At the same time, increased demand for fixed income ETFs has spurred the need for advances in trading technologies, accelerating the development and implementation of electronic and portfolio trading.

The expansion of the market in credit derivatives such as credit default swaps (CDSs) and collateralized debt obligations (CDOs) has also contributed to the evolution of the fixed income market, primarily by separating credit risk from funding risk. By allowing investors to take a position on an issuer’s creditworthiness without the need to borrow or buy its cash bonds, derivatives have made fixed income more accessible for operations such as hedging. This has contributed to increased liquidity in the market.

The Role of ETFs in Increasing Fixed Income Market Liquidity

As the fixed income market has evolved, ETFs have emerged as an important mechanism through which liquidity and price discovery are transmitted through this new ecosystem. Rather than replacing the underlying bond market, ETFs increasingly sit alongside other liquidity channels, helping connect investors, market makers, and the cash bond market.

The ultimate source of liquidity in the ETF market stems from the liquidity of the underlying securities held by the funds. Liquidity circulates through the market thanks to its unique two-layer structure. In the primary market, authorized participants (APs) can create new ETF shares or redeem existing ones in response to investor demand. As a result of this mechanism, an ETF is always at least as liquid as its underlying assets. Fixed income ETFs are further supported by the ability of market makers to recycle underlying bond inventory to help improve overall trading economics. In the secondary market, fresh capital enters the market through exchange trading, which is supported by market makers.1

While exchange trading is vital to the ETF ecosystem, a sizable proportion of ETF trades occur outside of traditional exchanges on venues such as RFQ platforms,2 directly between investors, or through other bilateral channels. As a result, the total traded volume of a fund, as well as the best price available – especially for larger transactions – may not be reflected in the data available on exchanges. Market makers are able to access deeper liquidity in an ETF’s underlying bonds, potentially allowing them to execute large trades at prices below those available on exchanges.

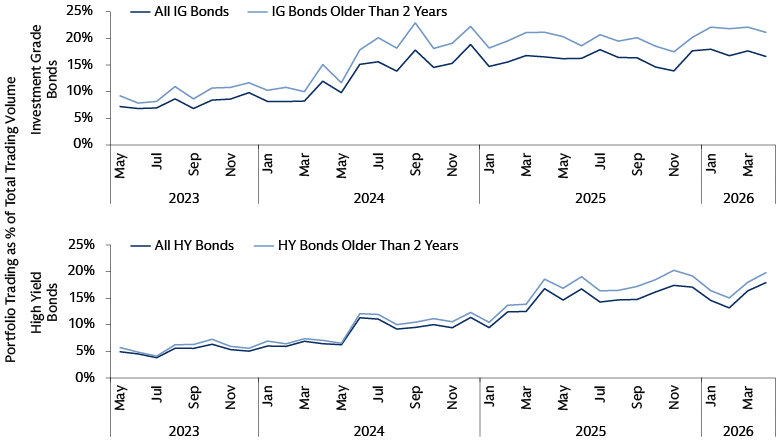

The liquidity that ETFs bring to fixed income has boosted parts of the market that previously traded less. A decade ago, most of the trading in fixed income – roughly 80% – was in the top 20% of liquid bonds. In the middle of the distribution, from the 20th to the 80th percentile, dealers would be less willing to provide liquidity because of concerns that the bonds would remain on their balance sheets for longer and could prove difficult to sell. Thanks in part to ETFs and portfolio trading, there is now far more trading in the middle of the distribution, and dealers are finding these bonds easier to sell. Bonds in the bottom 20% of the market by liquidity remain thinly traded.3

Source: TRACE, Goldman Sachs Global Investment Research. As of March 31, 2026. We exclude retail trades below $1 million and use estimated volumes from TRACE.

Delivering Liquidity in Periods of Underlying Market Stress

Fixed income is a dealer-driven asset class, which means you can buy only what is available from brokers and dealers. What ETFs have done well is to maximize integration between the buy-side and the sell-side, which helps support liquidity. This starts with full transparency on holdings, a feature of most ETFs, which enhances the ability of market makers to price a fund’s underlying assets accurately, make competitive bids, and maintain liquidity in the market. This transparency is also critical for investors who rely on it for risk-management purposes.

In addition, many fund providers’ capital markets teams work closely with their market makers and APs to explain their products and investment strategies. As more information is shared between the buy-side and sell-side, the spread between bid and ask may narrow, potentially benefiting both parties and the end investor. By having this dynamic in mind as they develop ETFs, fund providers may increase the likelihood of efficient trading. This is especially important in active fixed income ETFs, which are packaging not just bonds but less liquid asset classes and more complex strategies based on derivatives which are inherently harder to price.

The ETF market has proven to be robust, even in periods of market stress. A well-known example of this occurred during the market stress induced by the COVID-19 pandemic in 2020, when the US Federal Reserve sought to inject liquidity into the corporate bond market. As market liquidity deteriorated, the Fed’s Secondary Market Corporate Credit Facility elected to purchase not just bonds but also fixed income ETFs, which remained liquid and even saw trading volumes surge. When the Secondary Market Corporate Credit Facility’s purchases ceased, ETFs designed to provide broad exposure to the corporate bond market accounted for more than half of its $14 billion portfolio.4

ETF Liquidity Has Enhanced Price Discovery in Fixed Income

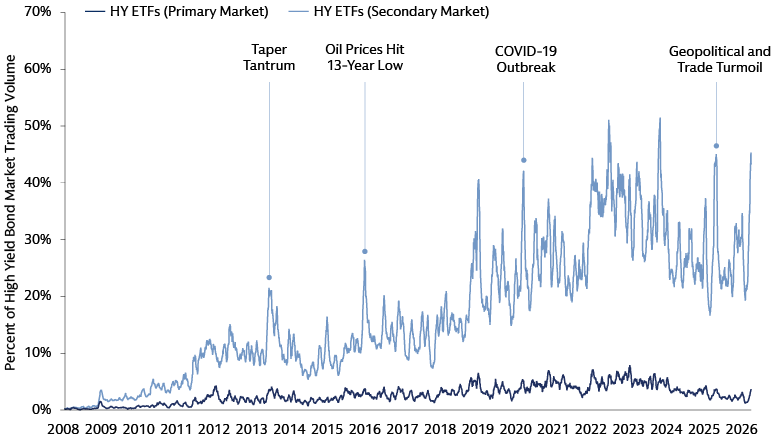

In addition to lowering costs for investors, ETFs have improved price discovery for asset managers, APs, and market makers. This is essential to ensuring that liquidity continues to flow in the primary and secondary markets. The continuous trading in the ETF market, coupled with transparent, real-time pricing for ETF shares, can provide a guide for the APs who create and redeem baskets of securities in the primary market and the market makers who provide liquidity in the secondary market.

This pricing function of ETFs can be especially critical during periods of market stress, when traditional credit markets can seize up, leaving market participants without up-to-date pricing information. ETFs have historically maintained or increased trading volumes during these periods of market dislocation. As a result, ETF pricing can potentially adjust more quickly than the underlying bond market, effectively providing a real-time indicator of where a diversified basket of bonds could clear. In our view, this represents a meaningful shift in how price discovery works in fixed income.

Source: Bloomberg, Goldman Sachs Asset Management. As of March 31, 2026.

The market’s ability to price the baskets of fixed income securities underlying ETFs also helps it price other products more efficiently. For example, say an investor wants to sell a portfolio of bonds. For buyer and seller, this transaction is similar to trading an ETF basket. The more diversified and ETF-like the portfolio, the more its pricing should align with the pricing of ETFs. After all, ETFs are just an equity wrapper around a basket of bonds. The pricing of bonds and the pricing of ETFs are increasingly linked. It’s becoming a circular loop.

For a small subset of large, heavily traded fixed income ETFs, the liquidity on exchanges allows the bid-ask spread of the ETF to trade well inside the bid-ask of the underlying basket of securities. These products may serve as benchmarks and bellwethers for price discovery of a given asset class.

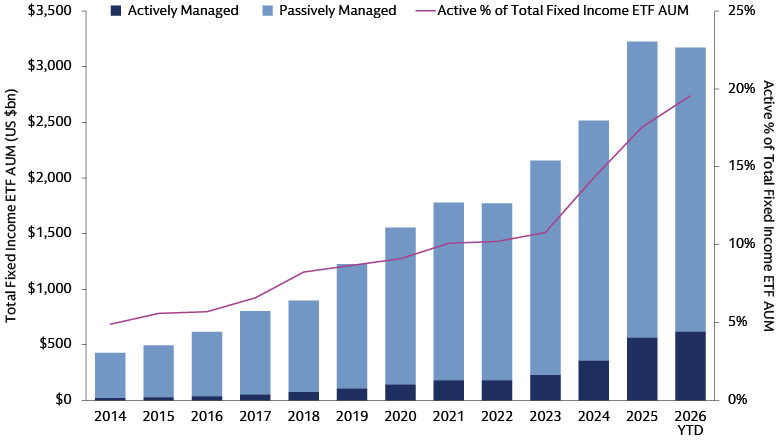

The Future of Fixed Income ETFs Is Active

ETFs have already had a transformative impact on fixed income and the ways investors access this market. The rise of actively managed fixed income ETFs is accelerating these changes. In addition to the potential benefits of the ETF vehicle, these funds offer the alpha potential, in-depth research and risk management that professional managers can provide. This unique combination makes active ETFs an effective way to expand investor access to asset classes once considered too complex, illiquid or broad, including high-yield, short-duration and municipal bonds, where structural inefficiencies make rigorous bottom-up security selection essential, in our view. Thanks to their flexibility, cost effectiveness, and growing list of use cases, active fixed income ETFs are gaining ground on their passive counterparts.

Source: Morningstar, Goldman Sachs Asset Management. As of March 31, 2026.

The push toward greater innovation will support the continued growth of active fixed income ETFs, bringing enhanced liquidity and improved price discovery into new areas of the market, in our view. Thanks to active ETFs, sophisticated strategies long used by institutional investors are now widely available. We have seen rapid growth in products that are opening up asset classes such as CLOs and private credit, for example. As trading volumes in these products increase, they may begin to support spread-tightening in these asset classes and attract new investors to these markets. Active ETFs are also an option for investors seeking exposure to more complicated strategies with higher return potential as well as solutions-based products that incorporate derivatives, such as defined outcome and derivative income ETFs.

As the complexity of active fixed income ETFs increases and their reach expands to new, less liquid asset classes, fund providers, market makers, and APs are working together to help ensure smooth trading in the primary and secondary markets. The ETF push into private markets has already begun, and we think this will accelerate as innovative fund providers find ways to reconcile the illiquidity of many private assets with the intraday trading and transparency that come with most ETFs. As new products are developed, fund providers will need to keep the specifics of the ETF market in mind and ensure that new products will be commercially viable, in our view.

The use cases for fixed income ETFs are also set to expand. Fixed income ETFs have been around for more than two decades, and for much of that time they were primarily associated with passive, index-tracking strategies used as building blocks in a core allocation. The rise of active ETFs is changing that. Rather than using ETFs for passive exposures and mutual funds or segregated accounts to access active strategies, active ETFs combine the two.

Active ETFs provide the flexibility for professional fund managers to pursue specific objectives, such as outperforming a benchmark. As ETFs expand into new markets, fund managers will have more tools at their disposal, enabling the use of ETFs for tactical shifts, managing risks such as duration, currency, and inflation, as well as enhancing liquidity during periods of market stress – all without the complexity of trading individual bonds.

Improving Fixed Income Market Structure and the Client Experience

ETFs arrived in fixed income much later than they did in equities for several reasons. Perhaps the most important is how these markets function. ETFs are equity-like products; they trade on the same exchanges as stocks. In fixed income, however, technological advances were required to accommodate ETFs. Vital mechanisms such as portfolio trading had to be developed and brought online. In turn, rising demand for ETFs drove the need for continued advances in fixed income market structure.

In the space of a decade, asset managers, banks, and market-making firms have worked together to make the fixed income ETF market work to the benefit of everyone involved. For investors from retail to institutional, this rapidly expanding market is opening up new areas of fixed income and providing a large and growing toolkit of flexible investment products and strategies. The rise of active fixed income ETFs is now taking these accomplishments to the next level.

1 In the US, nearly 50% of ETF trading occurs off exchange. Bloomberg. Year-to-date data. As of September 4, 2025. In Europe, the figure is close to 75%. Source: Bloomberg Intelligence. Data as of June 30, 2025. The distribution of trading can vary over time.

2 Request-for-quote platforms such as Bloomberg and Tradeweb allow buyers to request price quotes for products such as ETFs from potential sellers.

3 Portfolio Trading in Corporate Bond Markets. As of December 21, 2023.

4 “The Primary and Secondary Corporate Credit Facilities,” Federal Reserve Bank of New York Economic Policy Review. As of June 2022.