Fixed Income Outlook 3Q 2026

Key Takeaways

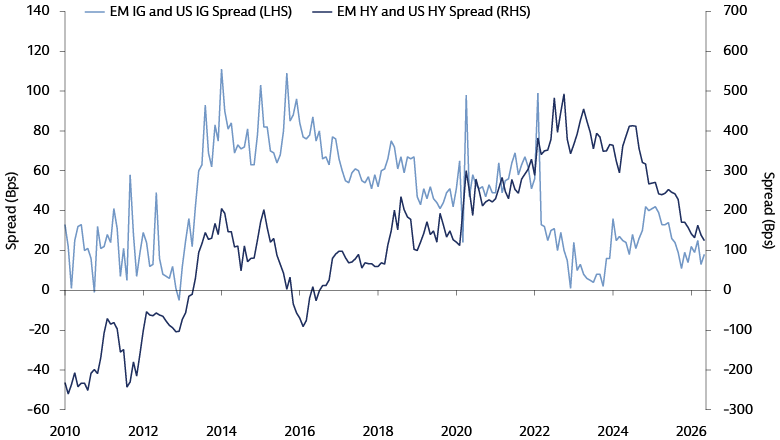

Finding Sources of Attractive Carry

Divergent macro paths across geographies create fertile ground for selective, high-conviction investing.

We believe opportunities within emerging markets (EM) debt provide a solid base to generate attractive carry relative to developed markets corporates; EM hard-currency corporates yield on average around 98 basis points more than global investment-grade counterparts, for example.

EM debt has the additional benefit of being relatively less exposed to the AI trade, positioning it as a natural diversifier away from more-concentrated markets.

Source: Macrobond, Goldman Sachs Asset Management. As of May 2026.

Assessing New Risks as AI Issuance Broadens

The breadth and depth of data center-related issuance require a holistic approach to assess their strengths and risks. These include:

- Construction Risk: Complexities of physical builds, lead times, and labor/equipment procurement should be analyzed.

- Tenant Quality Risk: Preference for data centers with leases directly linked to strongly rated IG tenants over speculative issuers.

- Lease Agreement Strength Risk: Favor contracts that limit tenant termination rights and utilize triple net lease structures, where the lessor agrees to pay expenses, insurance and maintenance as well as rent.

Positioning for Different Rate Paths

Global growth is unequal, demanding active management. The US benefits from AI and fiscal tailwinds, and Japan shows domestic strength. Conversely, Europe struggles with tighter financial conditions, and the UK labor market remains weak.

- Japan: Higher rates as the Bank of Japan (BoJ) risks falling behind the curve as inflation expectations rise.

- UK and Europe: Yields could potentially fall relative to the US due to weaker domestic growth.

- US: Risks to yields on the Treasury curve skew higher given the Fed’s recent hawkish pivot, while strong near-term data prints could clear the path for hikes.

Key Investment Ideas

- Emerging markets debt can provide an alternative source of carry, while also acting as a natural diversifier away from the AI trade.

- Overweight AI-related infrastructure within high yield and bank loans, which we believe offers an opportunity to seek above market returns through upgrades upon construction completion in strong structures with IG-rated lessors, while remaining underweight software and other disrupted sectors.

- Securitized credit remains an attractive source of high-quality carry, particularly in senior ABS, CLO and CMBS structures.

Download the full PDF for our easy-to-read Sector Allocation: Key Exposures and Quarterly Changes on positioning across sovereign bonds, currencies, and spread sectors.