2025 Private Markets Diagnostic Survey: Turning the Corner?

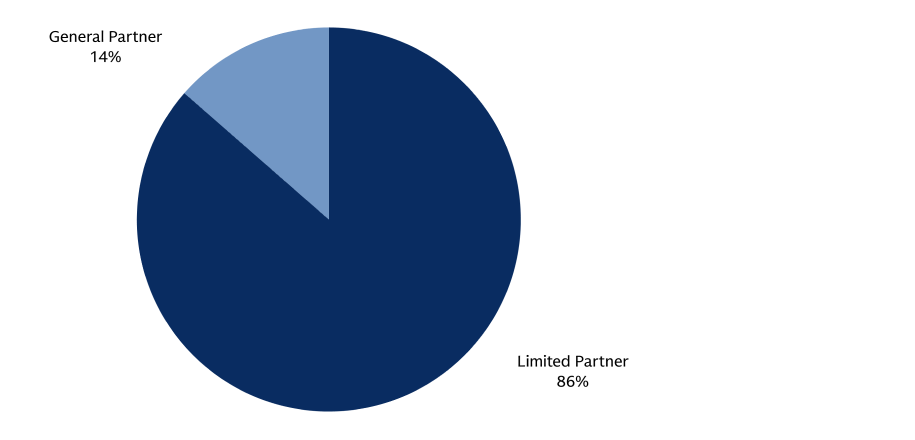

Who We Surveyed

- 223

- Limited Partnersacross pensions, insurance, asset / wealth managers, and others

- 35

- General Partners across private equity, private credit, real estate and infrastructure

Key Survey Findings

Investor Sentiment

Across private market asset classes, and especially in real assets, most investors are feeling the same or better about investment opportunities compared to a year ago. A lack of distributions has led many investors to adjust at the margin, but GPs are increasingly optimistic about delivering liquidity across exit routes.

Top Concerns

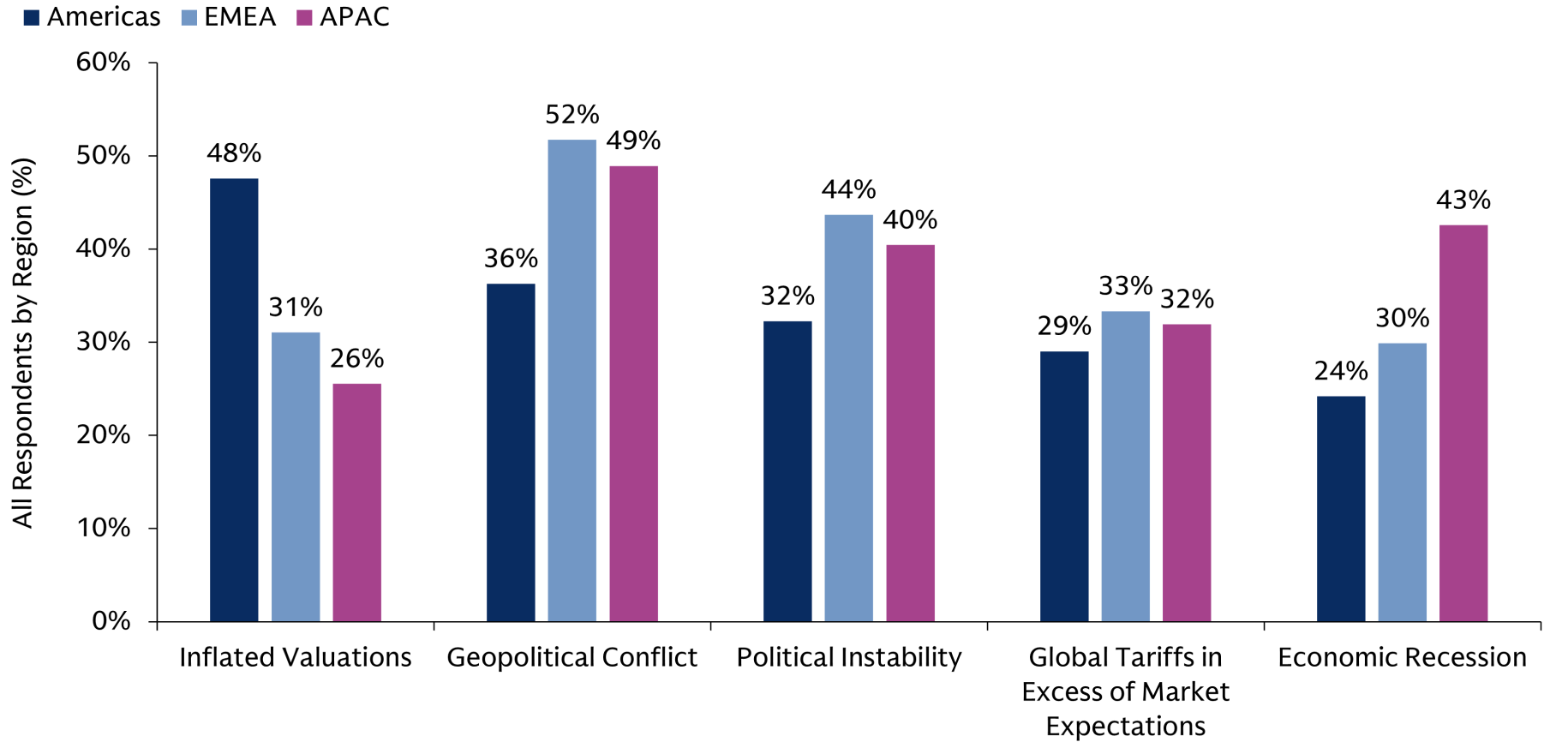

Main concerns differ by region: geopolitics are foremost in EMEA and APAC, while valuations are top of mind in the Americas. Valuations were cited by GPs as the main impediment to capital deployment, and the second biggest hurdle for exits.

Allocations Snapshot

Despite the much-discussed dearth of distributions, few investors are over their target allocations. Many LPs with mature programs continue to consolidate relationships, but investors generally continue to seek out new managers who can add value to their programs.

Manager Relationships

As LPs consolidate relationships, competition for capital has increased, with GPs expecting headwinds for flagship fundraises. When it comes to evaluating managers, LPs prioritize fees and terms, track records, and team stability; on the other hand, GPs view their differentiators primarily through an investment lens.

Evergreen Expansion

The Wealth market continues to be seen as one of the biggest drivers of industry evolution, but evergreen structures are not just a Wealth phenomenon.

Highlights from Respondents

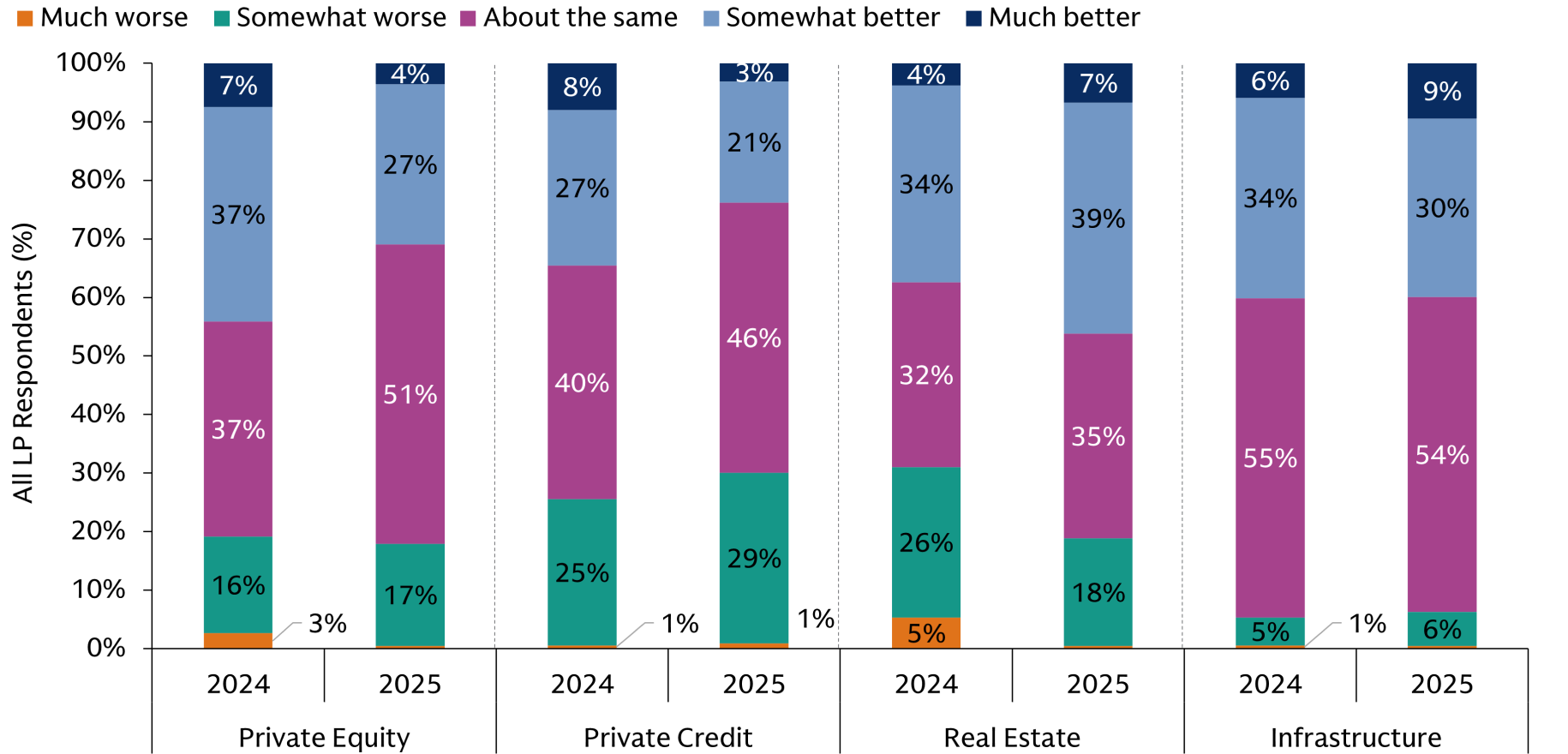

Investment sentiment is generally positive, with the most optimism for real asset Strategies.

How do you feel about current investment opportunities, compared to a year ago?

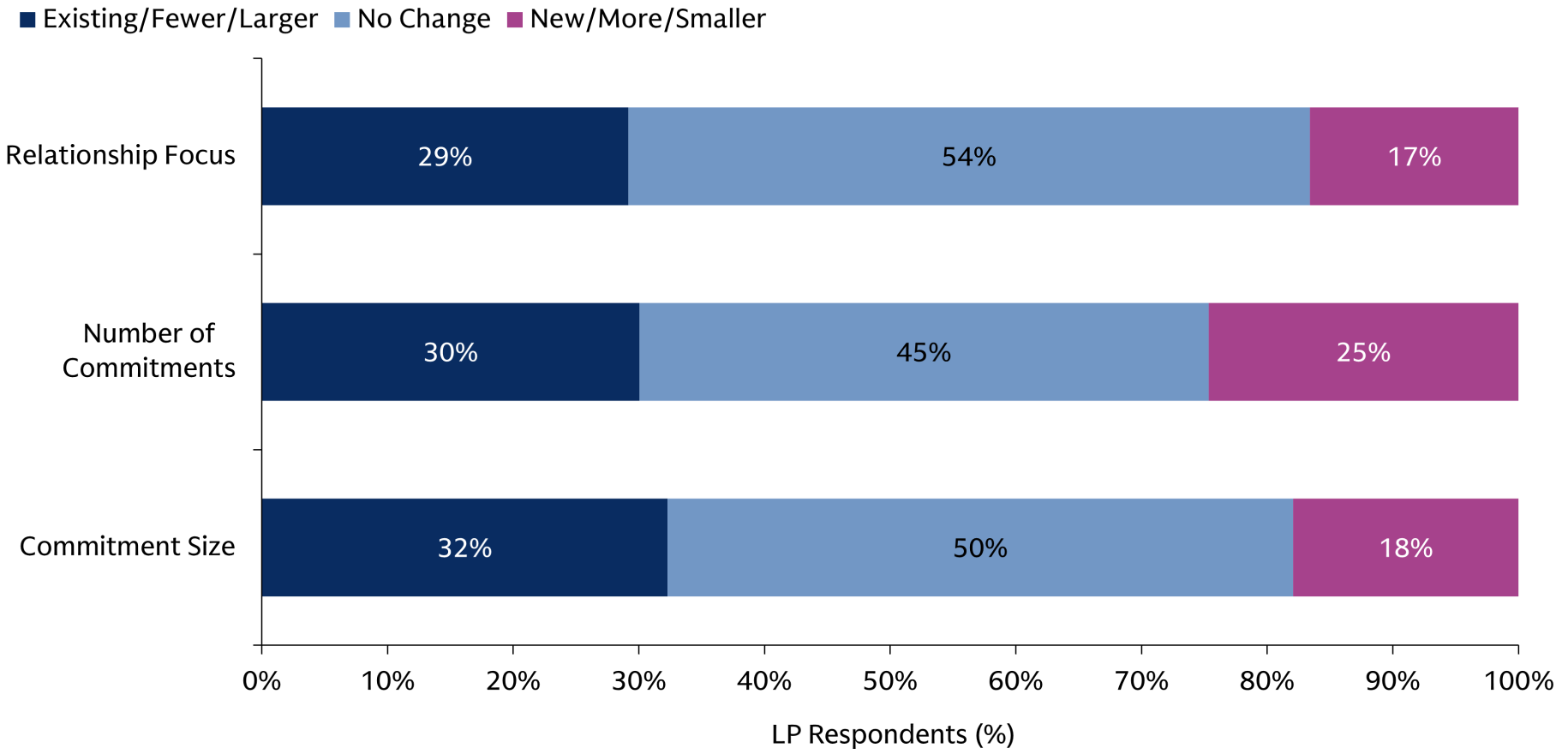

The shift towards fewer but larger commitments with existing managers remains intact.

How would you characterize your fund commitments compared to last year?

While evergreen funds often target wealth investors, many institutions continue to use them or are considering the structure-especially for income-oriented asset classes.

Describe your use of evergreen strategies in the following asset classes

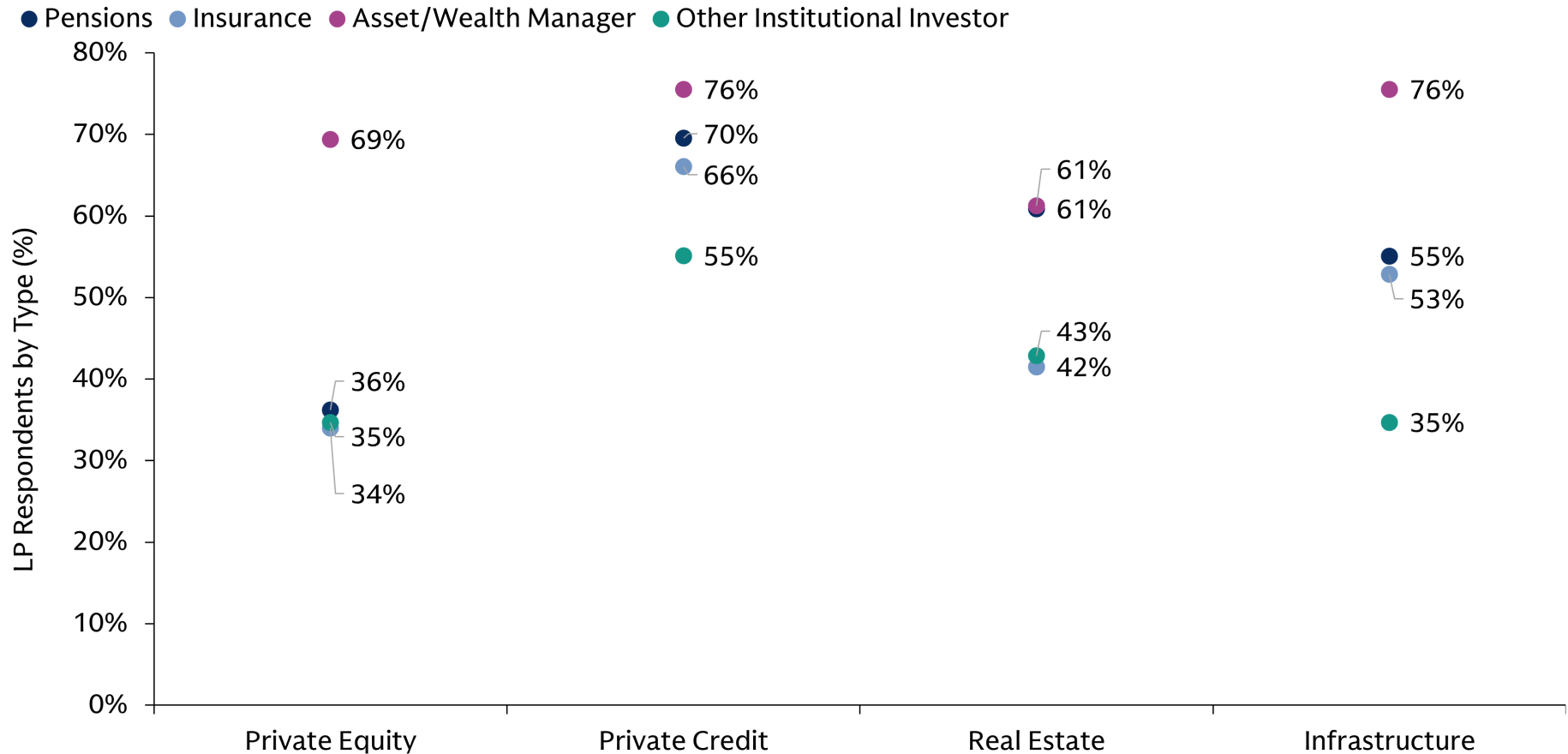

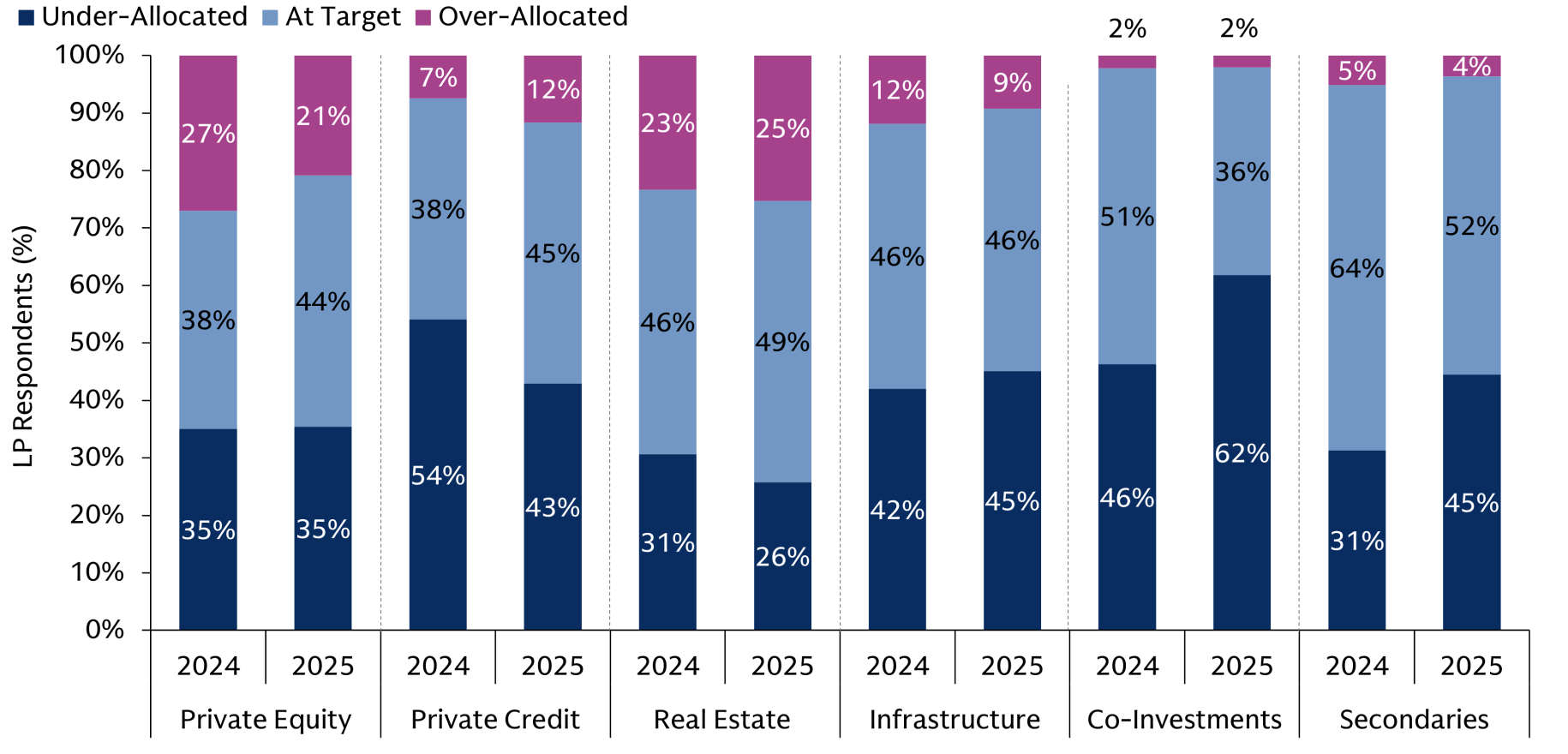

On net, LPs are under-allocated across private market strategies

What is the current allocation status for the following strategies?

Investors in the Americas are most focused on risks from valuations, while those in EMEA and APAC are more concerned about geopolitics and policy uncertainty.

What do you believe are the greatist investment risks today?

Methodology

Data for the 2025 Private Markets Diagnostic Survey was collected between June 30 and August 25, 2025. The survey includes responses from 223 Limited Partner respondents and 35 General Partner respondents from around the world.

Source: Goldman Sachs Alternatives 2025 Private Markets Diagnostic Survey compiled as of August 30, 2025.