Diversifying for Income: Core Building Blocks to Strengthen your Portfolio

Income generation has become a primary driver of total returns for investors, with all-in yields for investment grade, for example, hovering around 5%. In our view, strategies across the fixed income offering are flexible and differentiated enough to suit investor appetites across the risk spectrum, with some also possessing robust, ‘safe-haven’ properties that provide support for portfolios as other asset classes wane.

Diversification and income generation: Why it matters now

Fixed income was historically viewed as a one-stop shop for diversifying wider portfolios, due to its general negative correlation with equity prices. This was most expressed through a traditional ‘60/40’ portfolio, consisting of 60% equities and 40% fixed income instruments. The negative correlation meant that equities would generate most outperformance during periods of positive economic momentum, while the fixed income portion would provide a degree of downside protection through downturns.

This has changed in recent times, and investors need to diversify not just with fixed income, but within fixed income. Correlations in traditionally harmonious bond markets have become increasingly decoupled in an era of higher rates and volatility; for example, return profiles in US and global aggregate indices have become increasingly disparate. In addition, income has become a key driver of fixed income returns in the past three years. This means it is imperative for investors to consider how to appropriately diversify their portfolios while also maximising income potential.

Here, we explore four different ways investors of various risk appetites can rethink their fixed income allocations with diversification and income optimisation in mind:

Exploring income and diversification across the fixed income universe

- Core government bonds: Investments in developed market sovereign bonds such as US Treasuries can help give portfolios a solid underpinning of high-quality assets that may offer resilience in periods of uncertainty, potentially providing a source of returns as riskier assets underperform.

We believe the current environment also provides core bond investors with the additional opportunity of locking in higher starting yields rather than just downside protection and capital appreciation.

- Investment grade corporate bonds: Holding bonds issued by high-quality corporates—known as investment grade bonds—can also assist in portfolio diversification. Blue-chip names with robust balance sheets and diverse business lines can provide investors not just with a steady stream of income supported by strong underlying fundamentals, but could also act as another form of ballast for a portfolio in times of stress. Long-dated notes in investment grade credit, for example, can appreciate in volatile times should interest rates come down in that period. The additional yield relative to sovereign debt can also increase the income component of returns, emphasizing the primary role carry has for fixed income investors in 2026.

Some assets within fixed income can also offer increased income opportunities as well as potential diversification, further along the risk spectrum:

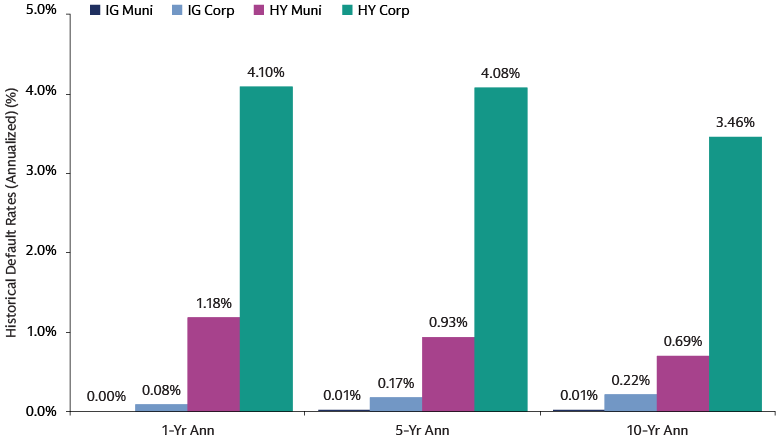

- Municipal bonds: Fixed income instruments issued by US states, cities and counties and other local government entities can also provide investors with compelling income opportunities. This in part stems from their relative tax efficiency; interest income from municipal bonds is generally exempt from federal taxes, and could also potentially be exempt from state and local taxes as well.1 When factoring in the tax advantage, municipal bonds may offer more yield than other taxable alternatives. This income boost is also backed by the asset class’s relative stability, high credit quality and low default rates; between 1970–2024, for instance, 10-year annualized default rates for investment grade munis stood at just 0.01% compared with 0.22% for IG corporate bonds.2 The difference was even more marked in the high yield space, with a 10-year annualized default rate of 0.69% for munis and 3.46% for corporates.3

These qualities are complemented by the muni market’s potential diversification characteristics. Munis’ close relationship with the public sector means the bonds somewhat mirror the direction of Treasuries, making them a potential diversifier against movements in equities and lower-quality credit sectors.

- High yield bonds: Corporate bonds below the investment grade threshold can offer even greater potential for investors seeking higher income levels. This comes at a time when the fundamental picture for the asset class has improved in recent years, despite investments in the space coming with additional risk given the assessed lower creditworthiness and lower-quality balance sheets. For example, the credit quality of the US high yield index is now more than 55% BB-rated compared with under 37% in March 2007.4

The current high yield environment could offer selective opportunities for active investors to take advantage of pockets of weakness, in our view. The recent selloff in the software space, for example, has been indiscriminate, with spreads in the sector widening significantly relative to the benchmark on AI concerns. We think this creates a window for active managers to pick up names facing relatively less AI disruption risk, such as mission-critical software providers, for instance, at relatively cheap valuations.

Source: Goldman Sachs Asset Management and Moody’s as of December 31, 2024. This data covers the period from 1970–2024.

Listen to our leaders and learn more about our Fixed Income Platform.

1 https://www.msrb.org/Education/Municipal-Bond-Basics-0

2 Moody’s Ratings, ‘US municipal bond default and recovery rates, 1970–2024’, Goldman Sachs Asset Management. As of August 4, 2025.

3 Moody’s Ratings, ‘US municipal bond default and recovery rates, 1970–2024’, Goldman Sachs Asset Management. As of August 4, 2025.

4 Bloomberg, As of March 31, 2026.