Prepaid Gas Bonds: Unlocking Yield in a Growing Municipal Sector

The municipal bond market is an extremely fragmented market that can be reshaped over time by issuance cycles, sector-specific trends and legislative changes. After two consecutive years of record municipal new issue supply, we are in the process of seeing one of these composition shifts play out in real time – with the growth of the municipal prepaid gas sector.

Here we highlight four key questions to better understand this growing sector and why an active management approach may be warranted.

1. What are prepaid gas bonds?

The prepaid gas sector is a specialized segment of the municipal bond market where tax-exempt debt is issued to fund the upfront purchase of a long-term energy supply—typically natural gas or electricity—for municipal utilities. These transactions allow municipalities to secure energy at a fixed price that is often discounted to market prices, providing long-term budgetary certainty and operational savings for the utility.

While these bonds are issued by municipal entities, the security of the debt relies on a guarantor (typically a global financial institution). This guarantor is responsible for managing energy delivery and ensuring bond repayment. Consequently, the credit rating of these bonds is generally linked to the creditworthiness of the corporate guarantor rather than the underlying municipal utility. In addition to the corporate credit exposure, these bonds have “pinhole risks” due to necessary commodity swaps and other derivatives to manage the energy price volatility over the long-term delivery period.

Prepaid Gas Bond Market Metrics

- $31.4

- Billion2025 issuance of bonds, a record year

- $100+

- BillionTotal market size

- $9.9

- BillionTax-exempt issuance year to date 2026, another potential record year

Source: Bloomberg, as of March 20, 2026.

2. What is driving the increase in supply of prepaid gas bonds?

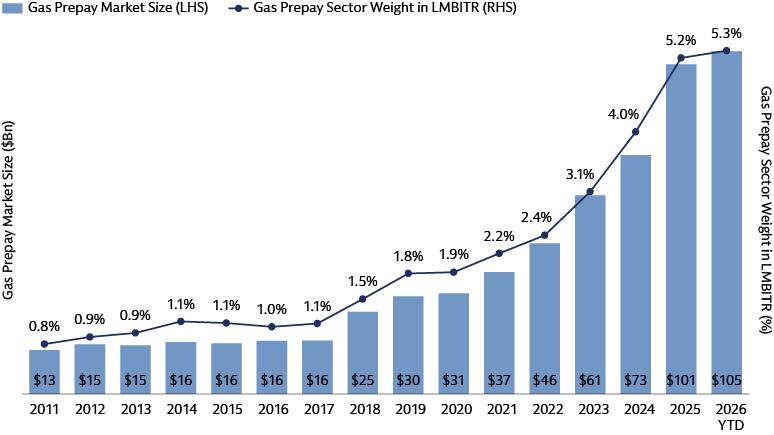

After record new issue supply in 2025 of $31.4 billion and a 27% compound annual growth rate (CAGR) since 2020, the total size of the Prepaid Gas sector now stands at over $100 billion. This outsized sector growth has meaningfully impacted sector weightings across major municipal indices, with sector exposure now reaching 5.3% of the Bloomberg U.S. Municipal Index, 10.3% of the Bloomberg 1-10Yr Municipal Bond Index, and 26% of the Bloomberg California Intermediate Index.

Source: Bloomberg Finance L.P., J.P. Morgan, data as of March 3, 2026.

The growth of this sector is being driven by attractive funding economics, growing corporate guarantor funding needs, and rising energy costs encouraging municipal utility adoption.

- Cost Savings for Utilities and Lower Borrowing Costs for Funding Recipients: Lower front-end nominal rates and ratios are creating lower borrowing costs that benefit both municipal utilities and guarantors. Utilities and third-party funding recipients have taken notice of the favorable economics and are rushing to the market. Historically, issuance in this sector was dominated by a few large banks, but given the funding needs of insurance companies, the issuer base is expanding in recent years.

- Rising Energy Prices: Increased energy demand fueled by artificial intelligence infrastructure buildout will likely result in higher energy prices which should drive more municipal utilities to participate in prepay transactions as it brings certainty to long-term expenses.

3. Why might prepaid gas bonds be an attractive investment opportunity within the municipal asset class?

Given the sector's structural complexity, prepaid gas bonds were historically held by traditional buyers such as mutual funds, broker-dealers, and insurance companies. However, with the continued expansion of issuance, the sector has seen growing interest from separately managed accounts (SMAs). These platforms have become increasingly institutionalized and have taken notice of the meaningful yield pickup the sector provides in the intermediate range versus other similarly rated sectors.

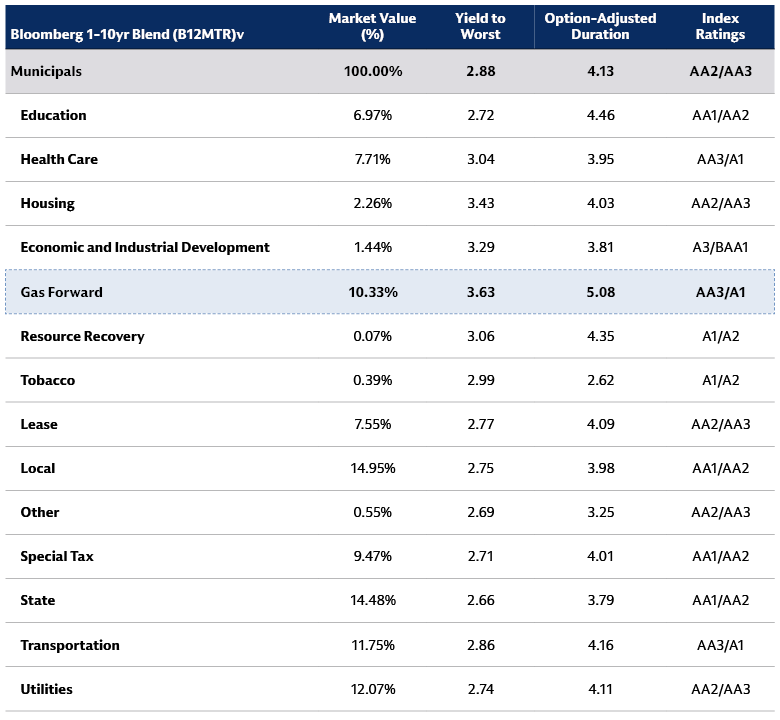

The relative value of this sector is most evident when assessing the opportunity set within the short/intermediate range of the municipal curve. When analyzing the yield to worst of individual sectors within the Bloomberg 1-10yr Blend Index (table below), the prepaid gas sector yields 3.63% and provides a 59bp and 77bp yield pickup compared to health care and transportation sectors respectively.

As mentioned in our 2026 outlook, the front end of the municipal yield curve should remain well bid, given expectations for continued federal rate cuts and persistent strong demand for short duration municipal bonds. As such, an allocation to Prepaid Gas, if sized appropriately and within a suitable investment strategy, could be an appropriate sector allocation to capture additional yield.

Source: Bloomberg, as of March 16, 2026.

4. What are the risks that need to be considered when assessing municipal prepaid gas bonds?

While the sector does exhibit significant yield pickup over similarly rated securities in the intermediate range, investors need to understand that the additional yield is a factor of the complex structure of these credits, relative illiquidity for retail sizes, and corporate credit exposure within a tax-exempt wrapper.

The sector is considered credit-intensive given not only the reliance on the corporate guarantor, but also due to necessary commodity swaps and other derivatives to manage the energy price volatility over the long-term delivery period that creates “pinhole risks”. Some of these risks include exposure to swap counterparties, early termination risk for contracts, and any physical disruptions from pipeline failures or weather that can prevent delivery, which could lead to a failed contract.

Even with these complexities the sector’s only default was as a result of Lehman’s bankruptcy rather than risks inherent to financial engineering or “pinhole risks”. Because of the direct credit linkage to corporate guarantors, the sector often exhibits higher volatility and spread widening in tandem with the corporate financial institutions during times of stress, such as the 2024 regional banking crisis. Furthermore, while the entry of new guarantors such as insurance companies is diversifying the space, outstanding issuance remains concentrated among a limited number of issuers, which can lead to sector underperformance vs traditional municipals. It is also important to note that the credit quality and credit analysis of underlying corporate guarantors is not one-size-fits-all, as the risks of a traditional financial institution such as a commercial bank are different than an insurance company.

Exposure to this sector should be limited to institutional investors with deep credit expertise and portfolio management teams that can assess relative value and liquidity risks.