Active ETF Due Diligence: A Combination of Art and Science

Exchange-traded funds have been around for more than 35 years, and during much of that time they were associated primarily with passive investing and index-tracking funds. That is changing. Actively managed ETFs, which debuted in 2008, now outnumber passive ETFs in the US.1 As their numbers increase, the strategies accessible through active ETFs have multiplied in response to investor demand. They offer flexible, cost-effective exposure to an expanding range of markets and asset classes as well as a growing toolbox of portfolio-management solutions.

Active ETFs combine the risk management and alpha potential that traditional asset management can provide with the liquidity, transparency, and cost-effectiveness of the ETF vehicle. Their unique structure requires a new approach to due diligence. Investors who are experienced in due diligence on passive ETFs will also need to account for the “active” or qualitative component of active ETFs, such as the fund’s investment philosophy and the team of professionals who manage it. Those who are new to ETFs, and have traditionally researched actively managed mutual funds, will also need to factor in the specific metrics of the ETF vehicle, such as liquidity and bid-ask spreads.

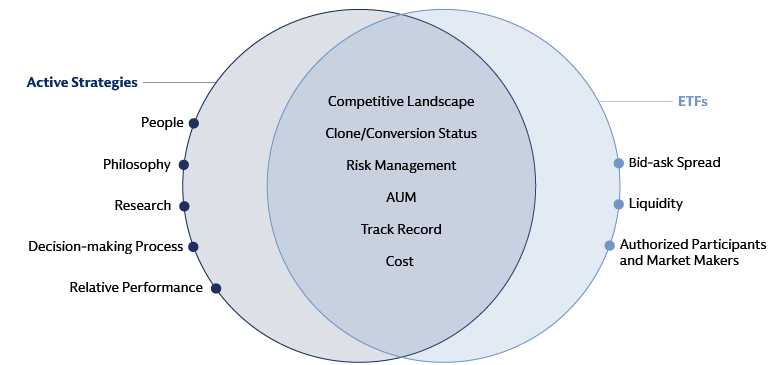

The breadth of considerations for investors who are performing due diligence on active ETFs is encapsulated in the following diagram, which shows some of the topics associated with actively managed strategies on the left, ETFs on the right, and shared considerations in the middle.

Source: Goldman Sachs Asset Management. As of March 31, 2026.

At Goldman Sachs Asset Management, we work with clients around the world who are considering adding active ETFs to their portfolios or enlarging an existing allocation. Here are some of their most frequently asked questions along with our answers.

1. What can active ETFs add to my portfolio?

The first question many investors ask is how an active ETF can help them achieve specific investment outcomes. Active ETFs offer a growing range of innovative solutions, such as fully active funds that pursue alpha, systematic funds that pursue a certain level of alpha within given tracking-error constraints, and solutions-based funds that use derivatives with the goal of achieving specific objectives such as income or a defined outcome. The ease of buying and selling an active ETF makes these products efficient tools for short-term and tactical investments, as well as for longer-term strategic allocations.

The versatility of active ETFs derives from their combination of active management and the ETF structure. This allows them to play many roles in portfolio construction and management, including alpha generation, risk management and diversification. They provide efficient access to public equity and fixed income markets, including parts of these markets, such as small-cap equities and high-yield bonds, where structural inefficiencies make specialist research and rigorous bottom-up security selection essential. Increasingly, active ETFs also target more specialized asset classes, such as collateralized loan obligations (CLOs). The transparency, ease of trading and – in some jurisdictions – tax-efficiency of the ETF wrapper can add value across the board, with tax-efficiency becoming an especially salient benefit for high-turnover strategies.

One example of active ETFs’ potential impact on portfolio outcomes applies to core equity allocations. Passive equity strategies have long been a staple of investors’ long-term allocations thanks to their lower cost and predictability. Yet index-tracking strategies have limitations, particularly the more basic ones: they tend to underperform their benchmarks after fees, provide limited risk controls, and lack the dynamism to manage market volatility, adapt to changing markets, or incorporate investors’ specific preferences. Investors seeking to make more efficient use of their portfolio tracking-error budget may consider an alpha enhanced solution delivered in an active ETF. These solutions are designed to boost the performance of core equity allocations while limiting tracking error by sticking close to a reference benchmark.

2. How should I approach active ETF due diligence?

The growth of both products and issuers in the active ETF market is accelerating, and we think investors need to adapt their due diligence to keep up. A narrow focus on track record, for example, may lead investors to miss out on innovative offerings. We think investors should follow a process with metrics tailored to active ETFs and the flexibility to evolve as new strategies and solutions enter the market. This begins with an expansive definition of active investing capable of encompassing the rapid proliferation of active strategies offered in the ETF vehicle.

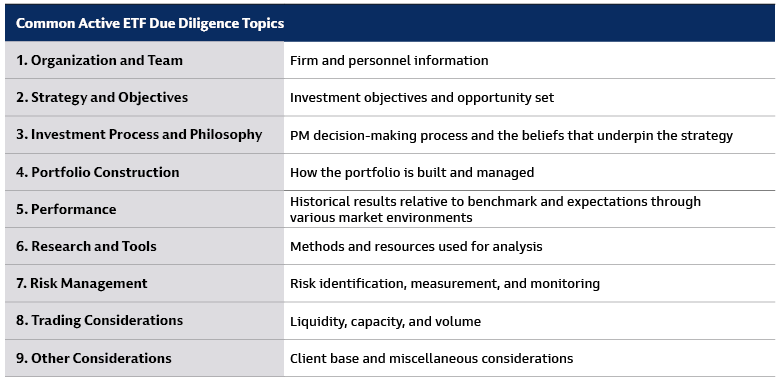

At a high level, the list of topics to cover in active ETF due diligence encompasses both how the portfolio is managed and details related to the ETF wrapper. Common active ETF due diligence topics include:

3. Given the rapid expansion of the active ETF market, and the proliferation of new strategies, how should I assess a fund’s track record?

Analyzing the track record of an active investment strategy is a standard due-diligence task. It can help investors judge a fund manager’s ability to deliver risk-adjusted returns and manage risk over time. If an active ETF is entirely new, the investor may have little to go on in terms of a performance track record. By contrast, if an active ETF has been converted from a mutual fund,2 or is a share class of a mutual fund,3 the investor can examine the products’ shared track record. If this direct link does not exist, but the issuer offers similar strategies in other formats, the track records of these other products may provide useful insights that carry over to the active ETF. Note that in many cases strategies are adapted to suit the ETF vehicle, so investors should be careful to identify any differences and factor them into their analysis. Lastly, if the strategy is systematic in nature, illustrative back-tested data may be available upon request.

A key point to consider is that a due diligence approach that applies the same minimum track record requirement to mutual funds and active ETFs may lead to investors missing out on innovative offerings, and potentially on quality, in the active ETF market. An insistence on a three-year minimum track record, for example, may lead to the selection of a first-generation active ETF that launched early, while overlooking newer funds that have historically benefited from the opportunity to learn from customer feedback, incorporate new features, and seek opportunities to stand out from the crowd.

In addition to conducting due diligence on active ETFs themselves, we believe investors also need to examine the strengths of their issuers. This process has become increasingly critical as the number of issuers globally grows – from 106 in 2020 to 293 in 2025.4 Active ETF issuers just entering the market may not have much in the way of relevant history for investors to examine. We think investors should start by examining issuers of active ETFs as they would providers of any actively managed strategy, including researching the relevant investment teams and the ecosystem supporting active managers within these firms.

4. How should I think about mutual fund to ETF conversions vs. newly launched ETFs?

In our experience, most due diligence teams feel comfortable extending coverage to strategies they previously reviewed and approved in mutual fund form, provided their operational teams are given ample advance notice to process the conversion. Some implement an observation period, while others approve the converted fund immediately.

For newly launched ETFs, the existence of related strategies (whether in a mutual fund or separately managed account) that the due diligence team can assess, is typically viewed as a positive. This is true even when the new ETF is not a direct conversion or a clone, as long as they leverage substantially the same investment team, philosophy, and process.

5. How can I assess a fund’s liquidity?

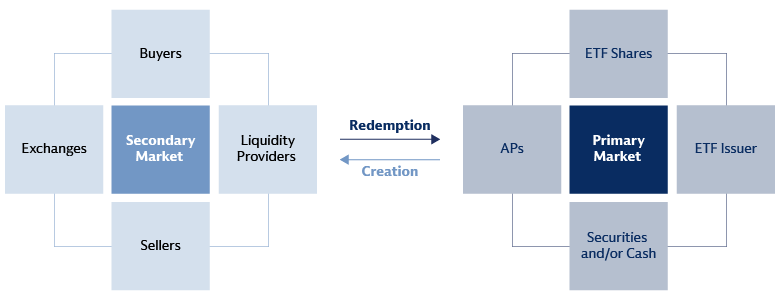

The ability to buy and sell ETFs like stocks – on an exchange at the prevailing market price – is one of the prime benefits these funds offer to investors. Yet in assessing ETF liquidity, investors need to look beyond average daily trading volume on exchanges, average quote size and the bid-ask spread, which are important indicators of liquidity in the traditional stock market.

There are two reasons for this. First, a sizable proportion of ETF trades occur outside of traditional “lit” exchanges, which display buy and sell orders as well as prices before a trade occurs.5 As a result, the total traded volume of a fund, as well as the best price available – especially for larger transactions – may not be reflected in the data available on exchanges. The second reason is that the ultimate source of ETF liquidity stems from the liquidity of the underlying securities held by the ETF. Through the creation and redemption mechanism in the primary market, authorized participants (APs) can create new ETF shares or redeem existing ones in response to investor demand.6 Thanks to this mechanism, an ETF is always at least as liquid as its underlying assets.

Given the liquidity relationship between the underlying basket of securities and ETF shares, we think investors should assess whether issuers have given sufficient consideration to liquidity during the product design phase to ensure ETF price/spread competitiveness. This means inquiring about the steps the issuer has taken to ensure APs are comfortable with a new product. While active ETFs will take tracking error versus a traditional benchmark, balancing strategy design with the ability of market makers to calculate intraday fair values and hedge appropriately is critical to ETF liquidity.

Source: Goldman Sachs Asset Management, as of March 31, 2026. For illustrative purposes only. There is no guarantee that objectives will be met.

6. How much do active ETFs cost to own?

The total cost of owning any ETF consists of the total expense ratio, which includes fees for services such as administration, management and marketing, plus the transaction costs involved in buying and selling shares. The total expense ratios of active ETFs tend to be lower than those of comparable active mutual funds and higher than index-tracking ETFs. Some funds report both a gross expense ratio, inclusive of all operating fees, and a net expense ratio, which shows the actual cost to investors after discounts or waivers are applied. We think investors should look at both, because discounts may be temporary.

Transaction costs vary according to factors such as the underlying exposure, creation and redemption fees, and market conditions. ETF share prices can change over the course of the trading day based on supply and demand from investors. The bid-ask spread – the difference between what investors pay for shares (the ask) and the price at which they can sell (the bid) – can result in a cost, especially for investors who trade frequently. A tight spread may therefore help reduce the total cost of ownership. Market makers can collect this spread by buying at the bid and selling at the ask, thereby supporting ETF liquidity in the secondary market.

Price fluctuation can result in an ETF trading above or below the value of its underlying holdings. Buying a fund at a premium to its net asset value (NAV), or selling at a discount, can result in a cost for the investor. We think investors should look for funds with stable price deviations from NAV that are narrow relative to the costs associated with transacting in the underlying securities. APs and market makers have an economic incentive to keep an ETF’s share price in line with NAV through the creation and redemption mechanism in the primary market.

7. How important is it for an active ETF to have a scalable investment strategy?

The scalability of an ETF’s investment strategy refers to the ability of the investment manager to invest large amounts of capital following the same strategy without negatively impacting returns or driving up implementation costs. The benefits of a strategy capable of expanding and functioning efficiently at scale potentially include deeper liquidity, lower operating costs and greater diversification. Unlike mutual funds, ETFs cannot close to new money because the ETF market structure allows for the creation of new shares in response to investor demand.

8. What tax benefits do active ETFs provide?

In the US, ETFs – both passive and active – are generally considered more tax-efficient than traditional mutual funds because of their structure. When an AP redeems ETF shares, it receives the corresponding shares of the ETF’s portfolio holdings in return. This “in-kind” redemption is not considered a sale by the ETF and it does not incur a capital gain at the fund level. This reduces otherwise required distributions of capital gains that would be taxable to its remaining investors. Thanks to in-kind redemptions, many ETFs effectively allow tax-free compounding of unrealized capital gains at the fund level. Investors are taxed only when they sell their shares in the fund. By contrast, mutual funds typically sell assets to meet investor redemption requests, which can trigger capital gains distributions that are taxable to remaining investors. Active ETFs may have higher portfolio turnover than passive ETFs, increasing the possibility of taxable events to investors and making the in-kind redemption mechanism potentially even more relevant for investors.

Outside the US, the tax treatment of ETFs varies widely. The ability for an ETF to not recognize capital gains upon an in-kind redemption does not exist in Europe. The rules for taxing capital gains in ETFs vary by country. Additionally, some countries restrict the transfer of ownership of locally listed securities through in-kind redemptions. Investors should acquaint themselves with the relevant rules in their jurisdiction.

9. How can I organize my due diligence efforts?

Institutional investors tend to streamline their due diligence by sending a questionnaire to fund issuers to request detailed information they want to review before investing. These questionnaires vary by investor, but the table below contains topics we encounter frequently.

Team and Approach

- Parent or group firm, adviser entity, legal domiciles

- Public equity business history, platform scale, milestones

- Concise bios of key investment personnel, organizational chart of investment team, hiring and departures of key investment personnel, culture, personal co-investment

- Name, inception date, investment objective, benchmark rationale

- Does the strategy exist in other forms (mutual funds, SMA, UCITS, etc)

- Features e.g. distributions, defined outcomes, etc.

- Permissible instruments (e.g. derivatives)

- Core beliefs, sources of competitive edge, empirical support or back-tests, decision making process, valuation views, adaptability

- End-to-end process summary, macro-view setting, periodic reviews

- Decision makers, contributors, succession and contingency, meeting cadence, documentation

Key risks, oversight, escalation and overrides, tools (proprietary versus third-party), operation to a risk budget, postmortems

- Research structure, idea generation, systems and data, external research, macro inputs

- AI or machine-learning and quantitative model usage

- Personnel Tools

Portfolio and Performance

- Eligible universe, inclusions/exclusions, security selection framework, typical investment horizon

- Position sizing, currency hedging, short exposures, derivatives or overlays (if any), constraints, cash management, equitization practices

- Typical number of holdings (range) and turnover range

- Multi‑year performance (NAV, market price, and benchmark)

- Return and risk attribution versus parent benchmark

- Active share versus benchmark and tracking error (historical and/or expected)

- Context for relative out/underperformance

- Capacity analysis and closure history

- Average bid/ask spread, premium discount

- Vehicle-level assets (annual growth since inception)

- Client base (top holders, seed)

- Cost vs. category average

- Is the fund a new strategy, a clone, the result of a mutual fund conversion, or part of a broader suite

10. What’s next?

What quant screens did for passive ETF due diligence, AI is likely to accomplish for active ETF due diligence - and then some. In the same way thoughtful quant screens have allowed savvy research teams to scale their efforts by helping them identify and monitor ETFs matching certain criteria, AI is already being tested or even deployed by certain platforms. Issuers can use it to draft and/or polish answers, drawing from approved sources. Gatekeepers may use it to draft summaries ahead of committee presentations, to identify salient differences between competing products and to spot trends or inconsistencies year over year. Coming of age at a time when many platforms are struggling to qualitatively assess a rapidly expanding universe of active ETFs, AI may offer a welcome bridge between the art and science of due diligence.

1 The number of US-listed active ETFs surpassed passive peers in June 2025. See “The Big Winners in the Active ETF Race, So Far,” Morningstar. As of November 4, 2025.

2 Converted ETFs have increased steadily the first conversion was launched by Guinness Atkinson Funds in March 2021. On the first converted ETFs, see “History Made as First Mutual Fund Converts Into an ETF,” Bloomberg News. As of March 29, 2021. By the end of 2025, 185 ETFs had been created through conversion, and all but one of them were actively managed. Source: Morningstar. Data as of December 31, 2025.

3 As of end-2025, only Vanguard offered ETF share classes of mutual funds. Source: Morningstar. Data as of December 31, 2025. The number of ETF share classes may increase if additional firms receive regulatory approval for this purpose. See “US SEC Readies Relief for Asset Managers to Add ETFs to Mutual Funds,” Reuters. As of September 29, 2025.

4 Morningstar. Data as of December 31, 2025.

5 In the US, 53% of ETF trading occurs on lit exchanges and the remainder off-exchange. Source: Bloomberg. Year-to-date data as of September 4, 2025. The significance of off-exchange trading is even greater in Europe, where just 28% of ETF trades occur on exchanges. Source: Bloomberg Intelligence. Data as of June 30, 2025. The distribution of trading can vary over time.

6 In creation, an AP delivers a basket of portfolio securities (or cash) to the fund issuer in exchange for ETF units comprised of new shares, which can then be sold on in the secondary market. In redemption, this process is reversed: the AP exchanges ETF units for underlying assets (or cash).