Gaining an Active Edge in Investment Grade Credit

Investment grade (IG) credit demonstrated robust performance in 2025, with euro- and US dollar-denominated IG credit returning 3% and 7.8% respectively in local terms.1 These gains occurred amid a volatile backdrop, characterized by shifting concerns around tariffs, AI capital expenditure, and fiscal spending. In our view, these factors, coupled with historically tight spreads and elevated dispersion beneath the index surface, necessitate a strategic approach in 2026.

We identify three critical pillars for navigating IG credit in the year ahead: seeking opportunities beyond passive benchmarks, positioning for spread widening, and actively navigating the AI trade.

Seeking Opportunities Beyond Passive Benchmarks

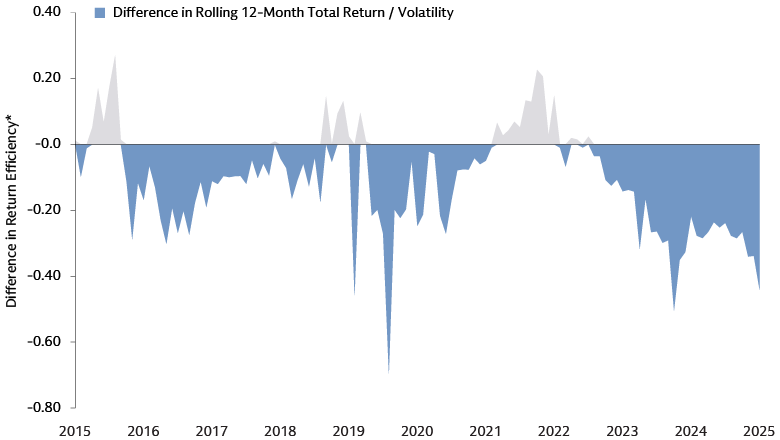

Passive benchmarks, while useful anchors, often don’t fully capture the full IG opportunity set due to rigid construction rules concerning issue size, rating, maturity, and liquidity. We believe this creates exploitable inefficiencies in pre-index and select off-benchmark bonds, even while keeping overall portfolio risk tightly benchmark-aware.

Out of an estimated $2.7 trillion IG issuance in 2026 (encompassing both US dollar and euro markets), only 50-75% is expected to enter commonly tracked passive benchmarks.2 When passive US dollar IG credit indices exclude bonds based on criteria like maturity (e.g., under three years) or specific issue/issuer sizes, for instance, it can lead to suboptimal risk-adjusted returns and a structural duration bias. We believe this dynamic is important for investors to consider in 2026.

Source: Bloomberg. As of December 31, 2025. The chart above compares iBoxx USD Liquid Investment Grade Total Return Index, a liquid subset of the US dollar IG credit universe and the Bloomberg US Corporate Bond Index, a broader measure of the US dollar IG credit universe. The blue color below 0 on chart indicates periods where passive index underperformed in vol adjusted terms and the grey color indicates where it outperformed.

Strategically Positioning Against Potential Spread Widening

While robust credit fundamentals and strong technical demand suggest IG credit spreads will remain near historically tight levels for most of 2026, several headline risks, including evolving AI sentiment, idiosyncratic credit events, elevated M&A activity, and geopolitical tensions, could trigger spread widening. To navigate potential volatility, active portfolios require sufficient ballast and flexibility, enabling managers to selectively underweight deteriorating credits or less attractive sectors, a critical advantage over passive approaches that are constrained by index composition.

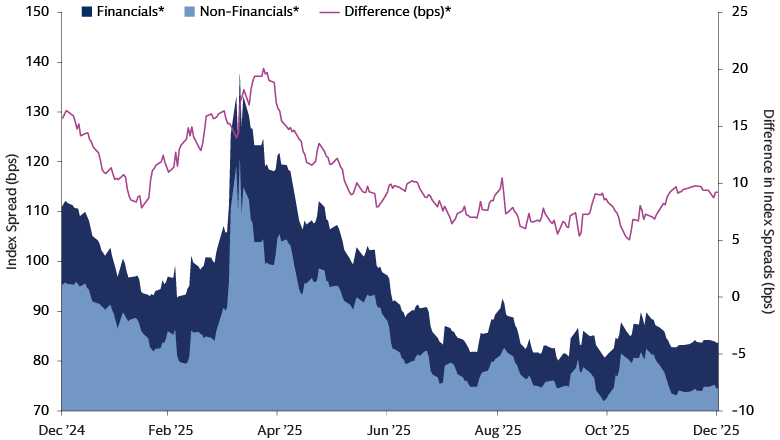

Strategic sector positioning, such as an overweight to financials (potentially benefiting from regulatory easing) and an underweight to non-financials (facing marginal M&A supply pressure), could provide both balance and alpha.3 Positioning can also extend to country and region exposures, alongside sectors, to mitigate concentrated issuance or sentiment risks. Implementation matters as well: managers can dynamically allocate between cash bonds and index-level credit default swaps (CDS) based on supply and technicals, and use cost-effective hedges within credit (for example, balancing higher-quality and lower-quality exposures) to improve resilience if spreads widen. These active strategies proved meaningful contributors to returns in Euro-denominated IG credit in 2025 and we expect this to continue in 2026.

Source: Bloomberg. As of December 31, 2025. The chart above compares Bloomberg Euro-Aggregate Financials Index, a subset of the euro IG credit universe focused on financials and the Bloomberg Euro Corporate Excluding Financials Index, a subset of the euro IG credit universe focused on non-financials.

Actively Navigating the AI Trade

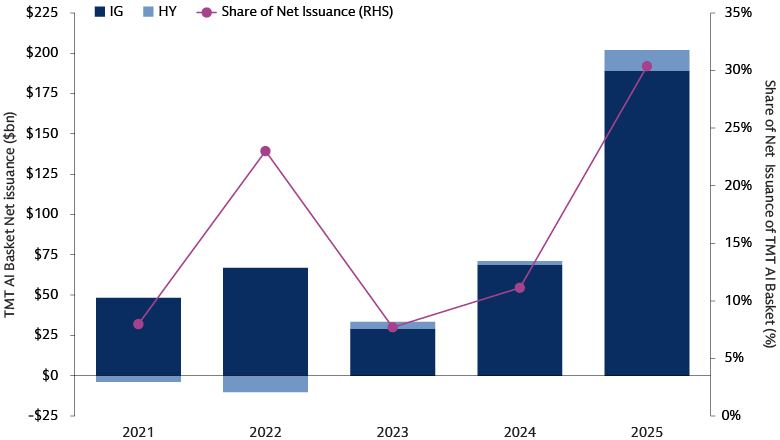

Geographic diversification, particularly into Euro-denominated IG credit via "reverse Yankee" deals (US companies issuing bonds in a foreign currency) and AI-linked issuance, is gaining momentum. This creates a tension for benchmark-aware investors: while the opportunity set broadens, market-value-weighted indices are increasingly concentrated in a handful of large AI-linked issuers.

The surge in US hyperscaler issuance exemplifies this, with approximately $87 billion in US dollar-denominated issuance in 4Q 2025 alone, compared to roughly $82 billion over the prior four years combined.4 The average cohort-spread ended 2025 20bps off their tights and underperformed the index over the period. We believe this meeting of heavy primary supply, compelling AI-related growth narratives, and concentrated benchmarks underscores the importance of actively selecting investments, especially new issues, and maintaining tactical and structural discipline.

Source: Goldman Sachs FICC and Equities, Bloomberg, Goldman Sachs Global Investment Research. As of December 31, 2025. AI-related issuers refer to the constituents of the GS TMT AI Basket developed by Goldman Sachs Global Banking & Markets.

Source: Bloomberg. As of December 2025. Average spread of US hyperscalers over time in USD vs USD benchmark spread, next to recent notable hyperscaler debt issuance: 1) Oracle 2) Google 3) Meta.

Unlocking an Edge in IG credit in 2026

With 2026 total return expectations exceeding 3% in euro and 5% in US dollar terms, IG credit offers a robust starting point and inherent resilience against potential downturns. However, historically tight spreads and other market complexities present distinct challenges. Achieving risk-adjusted returns demands conscious navigation: actively seeking opportunities within and beyond benchmarks, strategically positioning against potential spread widening, and adeptly navigating the evolving AI trade in credit.

1 Source: Bloomberg. As of January 12, 2026.

2 Goldman Sachs Global Investment Research. As of December 15, 2025.

3 Goldman Sachs Global Investment Research. As of December 12, 2025.

4 Goldman Sachs Global Banking & Markets. As of January 3, 2026.