Investing in the Architecture of AI’s Future

Key Takeaways

We believe the infrastructure foundation on which AI has been constructed will not sustain the AI of tomorrow. AI agents are rapidly maturing, while their foundational building blocks remain stagnant. Agentic AI tools are anticipated to be roughly 60-130x more energy-intensive than AI chatbots,1 necessitating a fundamental infrastructure rebuild. Beyond data centers, this creates a broad opportunity set across the physical bottlenecks that ultimately determine how fast and whether Agentic AI can scale, with inference load only amplifying the magnitude of the potential opportunity.

To date, investors have largely viewed chips, memory and manufacturing—currently capturing roughly 90% of AI profit pools2—as the core elements of the AI infrastructure ecosystem. Yet this perspective is incomplete and overlooks the critical chokepoints that enable these assets to operate at scale. As AI evolves towards Agentic, always-on systems, the pressure intensifies across the broader infrastructure stack. Solving these challenges requires a multitude of cross-industry solutions and companies to bridge the gap. This includes modernizing data centers, power generation and grid infrastructure, advanced cooling, connectivity, high-voltage components, and mission‑critical infrastructure services, each indispensable, and increasingly constrained. As these constraints tighten, we expect value to shift downstream to these nascent enablers, potentially creating a compelling investment opportunity.

Studies suggest that agents typically use about 4x more tokens than chat interactions, and multi-agent systems use about 15x more tokens than chats.3 What this understates is the structural shift in frequency: agents are expected to operate persistently across workflows rather than being accessed episodically. The combined effect is an exponential increase in aggregate inference demand, fundamentally reshaping infrastructure requirements. As inference intensity rises, latency and proximity become critical, pushing compute closer to where people live and work and necessitating a broad re-architecture of the AI infrastructure stack, encompassing data centers but also extending across the broader ecosystem.

Digital Infrastructure: Investors Want to Replicate Past Performance and the Bar is High

We’ve witnessed digital infrastructure evolve over decades, from broadband and telecom towers to fiber and data centers. Evidence suggests strong outperformance relative to other infrastructure sectors. For example, digital-focused infrastructure funds from 2009-2020 vintages have achieved a significantly higher net internal rate of return (IRR) when compared with diversified, renewable or power infrastructure funds. Digital infrastructure, specifically data center platforms, have been attractive for their public equity-like return profile paired with their infrastructure characteristics, including long-term contracts, asset intensity and historically low loss ratios.4

As Agentic AI emerges, experienced Limited Partners (LPs) are now seeking diversification within their data center-heavy portfolios and looking to replicate the strong return profile they have experienced over the last decade. There is simultaneously demand for “what’s next”, with caution surrounding investing in a perceived sector “bubble”. In their quest for the next generation of AI-related opportunities, we observe a greater willingness among LPs to go beyond traditional infrastructure characteristics (stable cash flows) and explore more private equity-like investments (growth-oriented, focused on value creation) tied to underlying AI infrastructure tailwinds.

Source: Cambridge Associates. As of July 25, 2025. Returns are horizon internal rates of return calculated since inception to December 2024. These returns are net of management fees, expenses and performance fees that take the form of carried interest. Diversified has 76 funds, Renewables has 28 funds, Power has 14 funds, and Digital has 8 funds. Past performance does not predict future returns and does not guarantee future results, which may vary.

We See Bottlenecks, Not Bubbles

The surge in AI capex among US hyperscalers has sparked concerns around the sustainability of these investments. However, market estimates suggest that rather than a speculative bubble, we are witnessing a structural shift. In 2026, companies’ AI-related capex is expected to continue to rise, surpassing $750 billion.5 At the same time, data center deployment is also accelerating, with more than 3,400 data centers having been announced or currently under construction in the US.6

We believe the primary catalyst for continued capital expenditure is the transition to Agentic AI, or AI 2.0. In our view, the evolution toward autonomous, always-on systems marks a new paradigm that is expected to drive over 90% of future digital infrastructure demand, signaling a massive buildout ahead. This shift moves beyond legacy requirements to necessitate persistent compute for continuous workloads, 24/7 power and cooling at an unprecedented scale, and sophisticated security to attempt to safeguard hundreds of millions of autonomous processes.

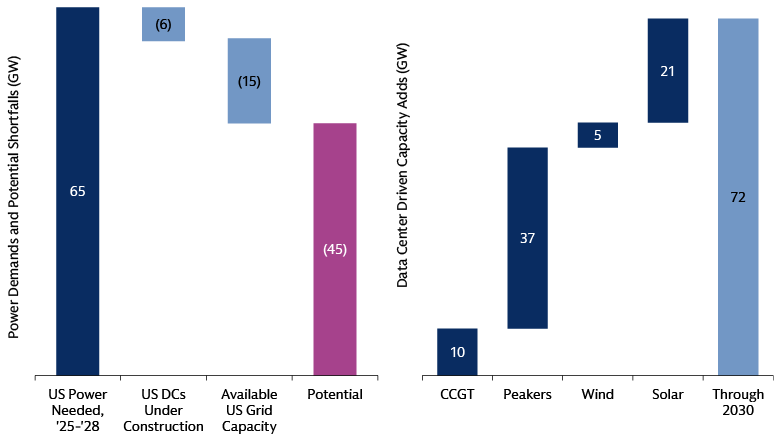

Source: Goldman Sachs Global Investment Research. As of January 12, 2025. CCGT is combined cycle gas turbine. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

The advancement of Agentic AI, in our view, is contingent upon successfully addressing several critical impediments. Estimates suggest that 72 gigawatts of new power capacity is needed in the US for data centers through 2030, a demand equivalent to 72 large nuclear power plants. By 2030, approximately 760,000 additional power and grid workers will also be needed, with 207,000 skilled US transmission & distribution roles requiring 3-4 years of training.7 Beyond people and power, there is limited land capacity suitable for large-scale projects. Compounding these issues are extended supply chain wait times for essential components like substations, high-voltage cables and steel.

Finding Future-Ready Companies

We believe these bottlenecks will create opportunities for private market investors to strategically deploy capital into high-margin, operationally efficient businesses that will form the backbone of the emerging Agentic AI opportunity set. We highlight four areas of focus below.

Powering AI necessitates robust energy infrastructure to enable AI compute across the entire power value chain, ensuring continuous 24/7 availability for high-density computing. Potential investment opportunities exist in grid-connected generation, "behind-the-meter" and distributed energy solutions, as well as thermal/backup systems.

Infrastructure services are crucial for supporting data center environments, encompassing design, engineering, and build services. Energy optimization, maintenance, and facility management are also vital for the efficient operation of high-density computing. Potential investment opportunities include companies offering specialized data center fiber splicing, which is currently a bottleneck for large data center buildouts, or end-to-end design engineering across site selection, power and cooling, and operational support.

Critical hardware and component providers are positioned at chokepoints within the AI supply chain. Potential investment opportunities include companies supplying advanced power distribution equipment or ultra-high-speed networking and memory ecosystems. This encompasses providers of components with meaningful differentiation sold directly to hyperscalers, as well as providers of grid components that drive power scaling.

Not all data centers will be able to support the accelerating demands of Agentic AI. Focusing on grid-powered data centers in established and urban locations, where demand is resilient and less susceptible to speculative oversupply, may prove resilient in the long run. High-performance computing data centers designed for Agentic AI workloads, differentiated by their compute-centric capabilities rather than just real estate, may also emerge as beneficiaries.

Capitalizing on the Agentic Opportunity Set

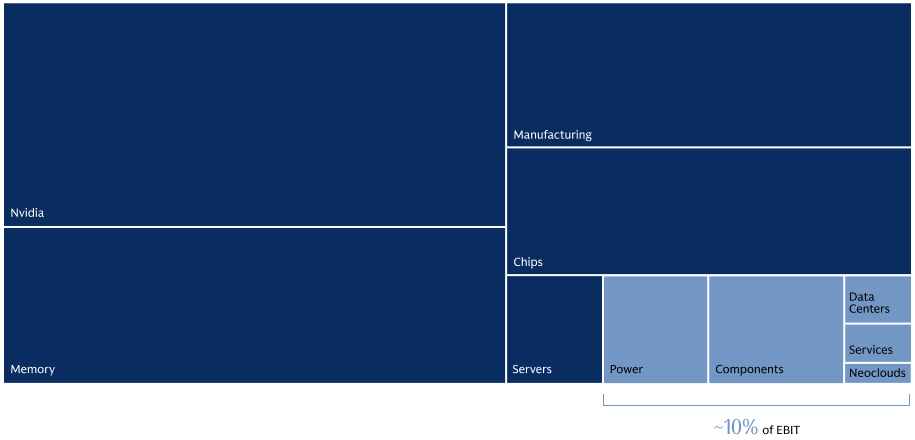

While the market has been fixated on data centers and chips, the visible peaks of AI innovation, we believe the bottlenecks will dictate the pace and scale of the expansion of the entire AI ecosystem. This oversight is starkly reflected in the current value attribution: the combined EBIT of chips, manufacturing, memory, and servers is nearly nine times that of power, components, and data center service companies.

Source: FactSet as of February 26, 2026. Any reference to a specific company or security does not constitute a recommendation to buy, sell, hold or directly invest in the company or its securities.

We believe this imbalance suggests a mispricing of the essential infrastructure that underpins the entire AI ecosystem, which signals a significant investment opportunity for digital infrastructure investors. Consider the extended supply chain wait-times for critical components like substations and high-voltage cables—these are not just logistical hurdles, but fundamental constraints that directly impact the speed and cost of Agentic AI infrastructure deployment, representing potential value for those who can address them.

We believe seasoned investors with a time-tested track record of identifying, executing, and scaling transformative digital investments globally are in an advantageous position to capitalize on these potential opportunities. Those with expertise in complex transactions (e.g., taking a public company private), developing differentiated financing solutions, and strong global sourcing capabilities to secure proprietary deal flow, are especially well placed to succeed in this new era. Once invested, we believe, rapid and strategic deployment of operating resources will be required to help drive efficient and successful value creation over time.

Don’t Overlook the AI Architecture of Tomorrow

The advancement of Agentic AI is contingent upon successfully addressing several critical structural impediments that the market has yet to appreciate. This transition to autonomous, always-on systems creates unprecedented demand across the physical infrastructure stack, including power generation and grid infrastructure, advanced cooling, connectivity, high-voltage components, and mission critical infrastructure services. Ultimately, we believe these physical constraints have transformed the AI race into a competition for infrastructure readiness, shifting the investment opportunity from the models themselves to the nascent enablers of the broader ecosystem.

1 “The Cost of Dynamic Reasoning: Demystifying AI Agents and Test-Time Scaling from an AI Infrastructure Perspective,” As of January 7, 2026.

arXiv:2506.04301 These figures correspond to a 62.1×–136.5× increase in GPU energy per query under agent-based test-time scaling (vs. single-turn LLM inference).

2 FactSet, as of February 26, 2026.

3 Anthropic. As of June 13, 2025.

4 Cambridge Associates, “Powering the Future: Infrastructure Trends, Performance, and Portfolio Impact” as of July 25, 2025 Returns are net of management fees, expenses, and performance fees.

5 Goldman Sachs Global Investment Research, “Q1 2026 mid-season S&P 500 earnings update,” as of May 1 2026.

6 Aterio, data compiled by Goldman Sachs Global Investment Research. Number of data center facilities in the US. As of January 19, 2026.

7 Goldman Sachs: The Power Industry May Need More Than 750,000 New Workers By 2030. As of July 2025.