Rethinking Securitized Credit’s Role in Your Portfolio

As investors who have been involved in securitized credit for three decades, we've witnessed significant growth and development in the asset class. In our view, its depth, breadth, and liquidity can complement other fixed-income sectors in delivering income and diversification. We believe market conditions for 2026 appear favorable; explore the asset class characteristics and tailwinds below.

1. What factors could reinforce continued momentum in securitized credit?

In our view, several positive factors, both broad economic trends and those specific to the sector, point to a pathway that could lead to further positive momentum for securitized credit:

Supportive Economic Environment Beyond Near-Term Risks: While uncertainty currently persists, we see the fundamentals underpinning credit markets as supportive, and anticipated government spending could continue to fuel economic growth. This economic strength can be particularly beneficial for assets across the securitized landscape, especially if this growth translates into increased consumer spending.

Selective Opportunity Set with Solid Underpinnings: The strength of securitized credit is also built on improving technical and fundamental pictures. Collateralized loan obligations (CLOs), for example, have remained relatively resilient so far this year; despite turbulence, the J.P. Morgan US CLOIE Index returned 0.74% in the first quarter of 2026, while euro index returns were 0.74%, despite wider volatility.1 However, diligent security selection remains critical, particularly with segments where careful analysis of borrower performance is warranted.

Potential Policy Boosts: Changes in government policies could also provide a positive push. For instance, new rules in the European Union, particularly changes related to Solvency II, have the potential to open the securitized credit market to a broader range of large investors as well as lower the cost of capital for holding securitized assets.

Today’s environment, although uncertain, provides opportunities for active managers to take advantage of the opportunity set that it provides. We see the opportunity today in particular as being selective carry across low-duration spread assets, with specialist securitized exposure standing out.

2. How can securitized credit boost your income?

We believe securitized credit can be an appealing option for individual investors looking to earn additional income.

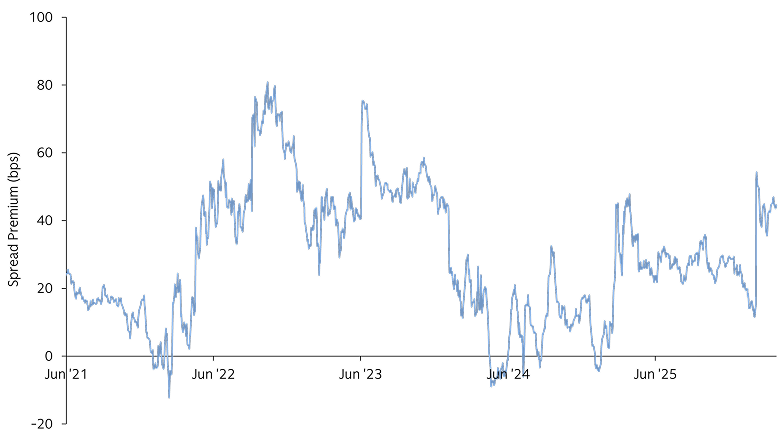

You can see this extra income potential clearly in CLOs. The extra interest on offer on an AAA-rated CLO index above their risk-free benchmark rate (known as the "spread") was comfortably above 120 basis points near the end of April.2 By contrast, bonds in the Bloomberg US Corporate Bond Index—made up of securities BBB- or higher—had an average spread of only 77 above an equivalently dated US Treasury bond, giving CLOs a ‘spread premium’ of nearly 45 basis points.

Source: Bloomberg, Goldman Sachs Asset Management, as of April 22, 2026.

3. How can securitized credit help diversify your investments?

Diversification means spreading your investments across different types of assets to reduce overall risk. Securitized credit can be a powerful tool for this, helping you mitigate risk and invest in various parts of the market. Here's how:

Broad Risk Spectrum: The pools of loans within a securitized product are often segmented into different buckets, called tranches. Some tranches contain loans considered very safe, such as senior debt and typically offer lower risk, while others are made up of debt from lower down in the capital structure but offer the potential for higher returns. Securitized credit lets you choose which level of risk you're comfortable with, allowing you to tailor your choice to your personal risk tolerance within a single investment.

Pooling Many Loans Together: A potential key benefit of securitized credit is that it's made up of many individual loans or mortgages bundled together. Instead of investing in just one loan, you're investing in fixed income instruments that are backed by hundreds or even thousands of loans. This means if one borrower misses a payment, the impact on your overall investment is likely much smaller, making your portfolio more stable and less affected by the problems associated with a single loan.

Investing in Different Kinds of Assets: Securitized credit allows you to invest in a wide range of assets that may not typically move in the same direction as your other investments (meaning they are less correlated). This includes collateralized loan obligations (CLOs), which are bundles of business loans, and asset-backed securities (ABS).

CLOs are an example of an element of the securitized universe that has recently come to the fore. Total global issuance has nearly quadrupled in the past two years, from $172.1 billion in 2023 to $659.9 billion in 2025 (JP Morgan), reflecting likely heightened investor interest in picking up higher yields than similar rated corporate bonds. Other potential advantages of CLOs include their tendency for their interest payments to be marked to a floating interest rate rather than a fixed one, which make them less sensitive to changes in rates.

At a time when rates may remain higher for longer, the role for Securitized is not to replace a core benchmarked bond portfolio, but to provide a liquid, low-duration income allocation for clients and CIOs who still want to carry without extending duration aggressively. In that context, securitized can offer clients a more differentiated approach than remaining in cash or using standard short-duration corporate credit.

Goldman Sachs Asset Management has been managing dedicated securitized portfolios for more than 30 years, with a global presence and deep experience across all securitized sectors.

1 J.P. Morgan JCLOAGTR index and JCLOEAGT index, as of March 31, 2026.

2 Bloomberg as of April 30, 2026. (120 is from 22nd)