Trade’s New Reality: What it Means for Manufacturing and Supply Chains

Key Takeaways

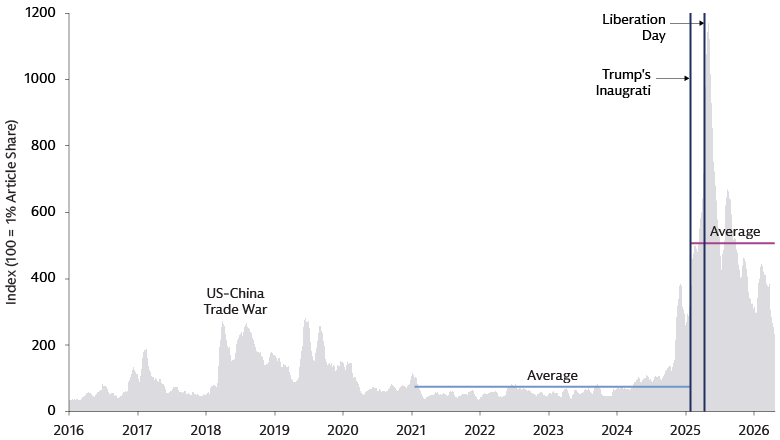

Liberation Day Learnings

One year after the implementation of sweeping US reciprocal tariffs, global trade has shifted. COVID-19 and the Russia-Ukraine conflict initially rerouted trade, and 2026 disruptions in the Middle East and the Strait of Hormuz have introduced further volatility. However, the 2025 "Liberation Day" tariff shock remains the most seismic event to global trade—the largest US tariff hike since the 1930s—designed to catalyze widespread investment in domestic manufacturing. We have identified several key observations regarding this transition.

Trade policy uncertainty has shifted from episodic to chronic

The post-Liberation Day era has ushered in a regime change for trade risk. The Trade Policy Uncertainty (TPU) index—which measures media attention to trade-related risks—has remained persistently elevated. Tariffs also triggered a chain reaction of defensive and offensive maneuvers by states and corporations, including challenges to the legality of tariffs, and subsidies to counter them. In this environment, investors must price trade policy as a continuous factor rather than a transient headline.

Source: Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo, "The Economic Effects of Trade Policy Uncertainty," revised November 2019, Journal of Monetary Economics. As of March 3, 2026. The trade policy uncertainty index (TPU) is constructed by staff in the International Finance Division of the Federal Reserve Board and measures media attention to news related to trade policy uncertainty.

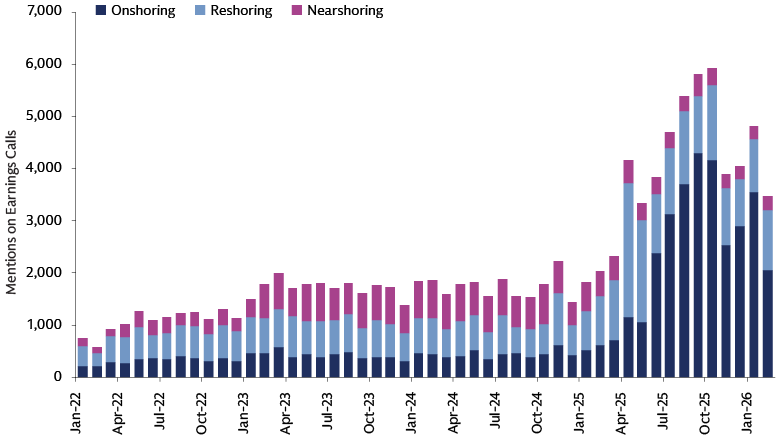

Onshoring and reshoring remain strategic priorities

Onshoring and reshoring mentions in corporate earnings calls remain elevated. The physical movement of manufacturing operations has been most pronounced in sectors deemed critical for supply chain, resource, and national security, such as semiconductors, batteries, and critical minerals. Data center deployment is accelerating (there are more than 3,400 data centers announced or currently under construction in the US).1 In Europe, fiscal reindustrialization initiatives and infrastructure spending are increasingly linked to defense, industrial resilience, and energy security.

Source: Bloomberg and Goldman Sachs Asset Management. As of March 1, 2026.

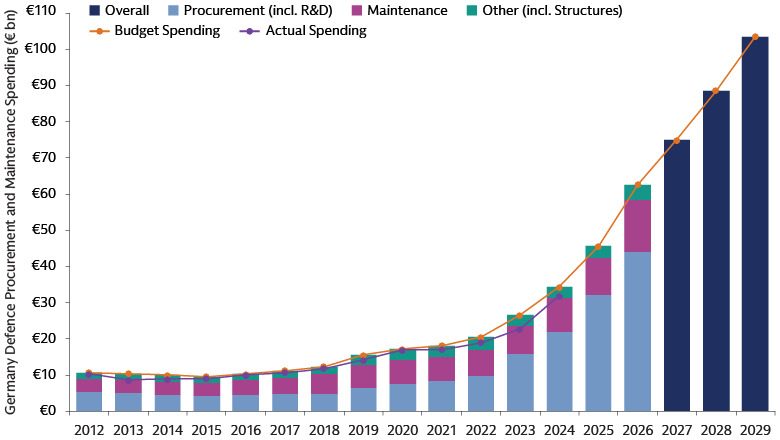

Europe is prioritizing resilience through trade diversification and defense

While exports to the US fluctuated due to tariff frontrunning, the EU maintained year-on-year growth by deepening ties with Switzerland, Norway, Turkey, and the UK. This "reshuffling" strategy, rather than a total "decoupling", buffers the region against external shocks. Nearshoring activity has been more prominent than reshoring in the eurozone.2 Germany continues to strengthen domestic defense production. Europe’s defense and electrification goals are currently constrained by limited access to critical raw materials, a challenge the EU Critical Raw Materials Act aims to resolve.

Source: Goldman Sachs Global Investment Research, Bundesministerium der Finanzen and Goldman Sachs Asset Management. As of January 14, 2026.

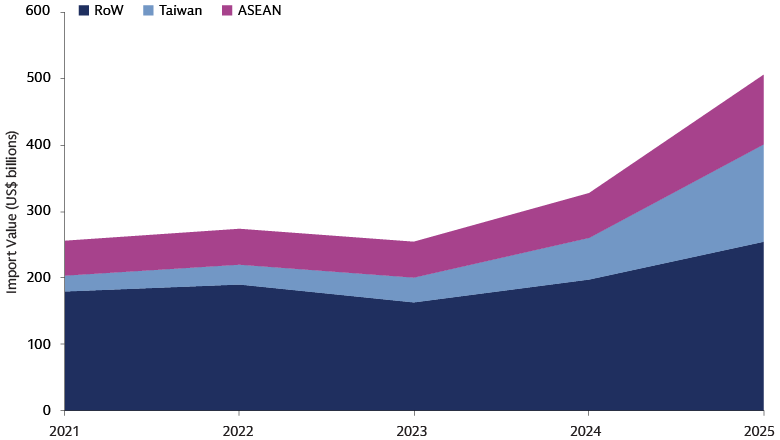

Continued demand for AI hardware and strategic goods

Demand for AI hardware, defense, and energy resources remains steadfast. US imports from Taiwan and other Asian tech hubs have expanded despite higher prices, driven by the critical need for semiconductors.3 Both the US (Chips and Science Act) and Europe (European Chips Act) are aggressively subsidizing domestic capabilities in AI and advanced machinery to mitigate geopolitical risks surrounding Taiwan. US semiconductor plant construction times are also accelerating due to enhanced familiarity with regulations and construction learning curves.

Source: US Census and United Nations COMTRADE. As of December 31, 2025.

Figures in Focus

- 206bn

- US construction spendingin 4Q 2025; nearly triple the amount in 4Q 2020.

- 95%

- US industrial business plan to introduce new automation over the next three years.

- 100%

- Rare earth processing is done outside the EU, mostly in China.

US construction spending source: Federal Reserve Bank of St. Louis. As of March 2026. US industrial automation source: RobCo Automation Readiness Index. As of December 2025. Rare earth processing source: European Court of Auditors. Publications Office of the European Union. As of 2026.

Manufacturing Renaissance and Supply Chain Security

Where do we see potential opportunities?

We believe the industrial renaissance and focus from governments and corporates on supply chain security presents long-term equity investment opportunities in developed markets.

Semiconductor Capital Equipment and Manufacturing

Between 1995 and 2020, the US share of global GDP related to high-tech manufacturing (semiconductors, but also precision tools and communication equipment) fell to 10%.4 This multi-decade decline is now undergoing a major reversal. Major US players are bringing semiconductor production back to domestic soil. Asia-centric giants are also evolving into distributed producers, with billions of dollars invested in Arizona, alongside new facilities in Japan and Germany. This drive towards semiconductor self-sufficiency acts as a massive tailwind for specialist equipment providers. We see companies in the US, Europe, and Japan with machinery required for the construction of new domestic mega-fabs (mega fabrication plants) and nearly every step of the chip-making process. This includes firms with systems that enable the growth of compound semiconductor materials critical for high-efficiency power conversion, and companies with a dominant market share in chip contamination control technology.

Modern Infrastructure and Logistics

The "multiplier effect" of mega-projects, notably data centers powering the growth of AI, benefits firms providing the underlying infrastructure and logistics. We see heavy machinery rental companies supporting multi-billion-dollar construction in developed markets sites by providing industrial tools. Businesses are also providing key maintenance and repair services to ensure around-the-clock production. Meanwhile, the construction and operation of factories, particularly those producing batteries for electric vehicles, generate massive waste streams, driving demand for localized disposal and recycling services.

Electronics and Industrial Automation

The return of manufacturing to high-cost regions is predicated on cutting-edge electronics and automation. As US-based manufacturers in sectors like semiconductors, EVs and life sciences build new domestic facilities, they require sophisticated automation infrastructure, including sensors, control valves, measurement devices and centralized control platforms that serve as the operational nervous system of a modern factory. Semiconductor factories are expensive to build and operate, so companies are building systems that enable robots to move materials through the production line 24/7 without stopping, with ultra-precise measurement, ensuring factories never clog up. Plant operators seek to build virtual models of their facilities and optimize throughput, creating virtual replicas of factory floors. Before a single piece of equipment is installed in a new US mega-fab, engineers use these digital twins to simulate production and identify bottlenecks. Automated defect and damage detection sensors that identify flaws in manufactured products as they move through the production line are also in high demand.

Strategic Metals and Rare Earth Resilience

Rare earth minerals and other essential metals, such as copper and lithium, are indispensable to modern manufacturing. The US is net-import reliant on critical minerals and has plans for a strategic stockpile of them. Even where the US has domestic mining capacity, such as for cobalt, nickel, and rare earth elements, the country lacks the domestic processing capacity to avoid downstream net-import reliance. EU demand for rare earth metals is expected to increase six-fold by 2030 and seven-fold by 2050.5 There are significant rare earth reserves in Europe, but no mining takes place.16,000 tons of rare earth permanent magnets are exported from China to Europe each year, representing approximately 98% of the EU market.6 We see companies helping to ease the dependency on China and strengthening the resilience of supply, including firms with scaled rare earth mining and processing sites in North America, and companies in Europe providing the industrial gases and chemicals processing infrastructure required for refining rare earths.

Investing in Trade’s New Reality

The global trade landscape has shifted toward a reality defined by geopolitical uncertainty and a structural pivot toward security. In developed markets, prioritizing supply chain strength, resource resilience, and national security is now a permanent fixture.

We are in the early stages of a multi-year investment cycle benefiting companies driving this manufacturing renaissance, from semiconductor equipment providers to logistics innovators. Investing in reshoring‑driven areas provides exposure toward parts of the economy where returns are anchored in physical assets, infrastructure and industrial ecosystems. These ecosystems span advanced manufacturing, power, logistics, materials and equipment suppliers, which are capital‑intensive, location‑specific areas shaped by regulation, supply‑chain complexity and long investment cycles. As AI increasingly reshapes software, services and data‑driven sectors, reshoring‑linked investments may potentially offer a differentiated source of growth tied to real‑world production and strategic supply resilience.

We believe active investors with cross-sector and global expertise are well positioned to capture these opportunities. In our view, success requires a holistic understanding of the ecosystems and careful stock selection to identify potential winners.

1 Goldman Sachs Global Investment Research. As of February 5, 2026.

2 European Restructuring Monitor (ERM). As of March 31, 2026.

3 US Census and United Nations COMTRADE. As of December 31, 2025.

4 McKinsey. As of April 12, 2021.

5 European Commission. As of March 31, 2026.

6 World Economic Forum. As of October 29, 2025.