Unlocking Alpha Potential in Inefficient Markets

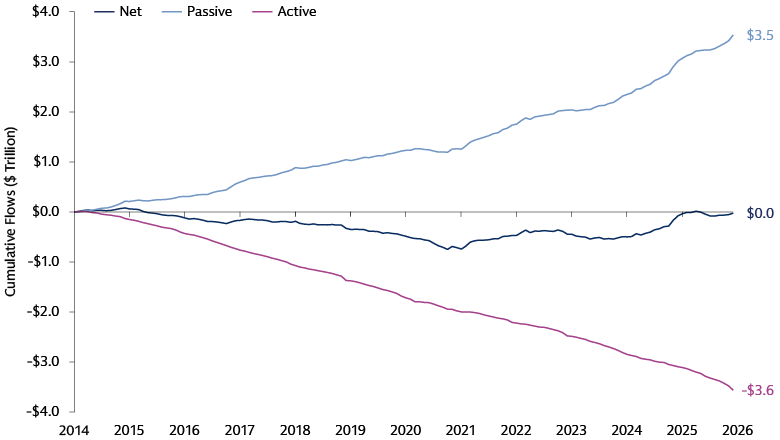

The structure of global equity markets has changed dramatically over the past 30 years. The market was once dominated by actively managed mutual funds that sought to outperform their benchmarks. Over time, asset flows in most developed markets shifted into passive or index-tracking investments, lured by the potential for lower costs and more predictable performance. In the US, the script flipped in 2019, when passive equity funds overtook their active peers by assets under management.1

Some investors and market watchers point to the rise of passive strategies as evidence that equity markets are becoming more efficient. After all, in an efficient market all information affecting the future value of stocks would be rapidly priced in, leaving little room for active fund managers to generate alpha consistently or predictably. We see things differently. In our view, important developments such as the growing share of passive equity ownership and the surge in retail equity trading have reduced market efficiency.

We believe these trends are expanding the alpha opportunity set for data-driven investors who can cut through the noise. We think an active approach to investing is critical in this environment, and a little active can go a long way, especially for investors with large passive allocations who may be missing out on growth opportunities while feeding market inefficiencies.

1) How has the rise of passive and retail investing affected the equity market, and has it improved market efficiency?

These developments have disrupted the traditional approach to equity investing in two ways. First, the sources of information these new investor groups have access to differ widely in quality and depth. Second, their investment decisions are often not based on the fundamentals that professional investors traditionally relied on to assess the fair value of stocks.

As a result, the rising prominence of these investor groups has introduced new sets of inefficiencies, causing markets to become increasingly fragmented and price insensitive. Passive funds account for a growing share of company ownership around the world. In the US, passive funds own nearly a quarter of the Magnificent 7 companies and the S&P 500, up from less than 10% in 2000.2 When passive strategies periodically adjust their holdings in line with the reconstitution of their benchmarks, this process is more or less mechanical because the aim is simply to track the benchmark as closely as possible. We believe these trades are indifferent to fundamental metrics, exacerbate equity crowding and reduce market efficiency.

Source: Goldman Sachs Asset Management, Goldman Sachs Global Investment Research. As of December 31, 2025.

The importance of retail equity investors has also increased significantly. In the US, for example, retail investors’ share of total equity volume has doubled over the past 15 years to about 20%. Retail investors tend to act based on emotion and herd behavior, often favoring stocks with poor financial quality in the hopes of lottery-like payoffs, in our view. As with passive strategies, retail trading tends to be indifferent to fundamental metrics including price. Its growth therefore contributes to reduced market efficiency. We think investors who fail to understand these trends in equity markets are operating at a significant disadvantage.

2) How can understanding the evolution of equity markets help investors identify alpha opportunities?

Passive fund flows are uninformed, but this trading – especially in large volumes – nevertheless impacts the market. Index reconstitution pressure can drive stock prices above their long-term averages, but prices tend to revert over time. Because these trades are passive and price-indifferent, they can translate into crowding so intense on reconstitution days that trading costs for uninformed investors can run three times higher than those paid by institutional investors in similar-sized trades.

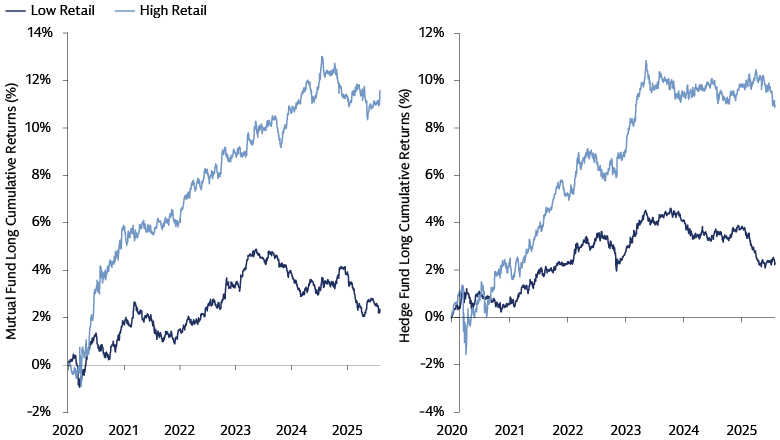

We find that retail investors can also drive sharp, short-term price surges followed by a longer-term reversal as prices move back toward fair value. While retail trading is generally uninformed, its patterns based on behavioral biases tend to be predictable, potentially allowing informed investors such as mutual and hedge funds to profit. We believe this is reflected in the fact that since 2020, long bets by mutual and hedge funds on stocks with high retail participation have significantly outperformed their bets on stocks that attract less interest from retail investors.

Source: Goldman Sachs Asset Management. As of December 31, 2025.

3) What makes Europe a fertile market for alpha?

Europe’s equity markets are structurally more fragmented, heterogeneous, and complex than the US market. Information tends to diffuse more slowly. A wide dispersion across countries, sectors, business models, and macro regimes means a broader opportunity set, while informational coverage is thinner and more uneven, leading to slower and less efficient price discovery – even when price discovery is the driver of investor actions.

The trend toward increased price-indifferent trading that we see in the US is also changing the European equity market. For example, we believe that alpha opportunities from retail-driven dislocations can be found in countries with high retail participation such as Germany, Spain, Switzerland, and the UK.3 Consider the behavior of retail investors around “Liberation Day” in 2025, when US President Donald Trump announced a raft of new import duties on goods from around the world, including Europe. Institutional investors initially adopted a risk-off stance that led to a sell-off in European equity markets. Retail investors initially bought the dip, creating a price dislocation, but soon reverted to selling. Institutional investors took the other side of this trade, resulting in net flows between the two investor groups being -74.5% correlated for the period between January and October 2025.

These dynamics increase the prevalence of informational asymmetries and cross‑sectional dispersion, conditions under which active management has historically been more successful. Quantitative strategies are particularly well suited to this environment because they can systematically process fragmented and high‑dimensional data, uncover subtle and non‑obvious relationships between stocks, and consistently exploit inefficiencies at scale. These capabilities have the potential to turn Europe’s structural complexity from a challenge into a durable source of alpha. As a result, we have seen quant managers in Europe outperform fundamental managers across various time horizons.4

4) What tools do investors need to gain an informational advantage, navigate underlying market dynamics and potentially generate alpha?

The information available in equity markets is expanding all the time. Traditional data such as return on equity and profit margins are essential in identifying high-quality companies that are suitably priced, while at the same time, alternative data derived from analyzing everything from earnings calls and customer transaction data to media coverage and social media can help determine the right time to invest as markets become increasingly sentiment driven. This data is increasingly unstructured and dispersed, however, and is not accessible to all investors.

Given the rise in uninformed, price-indifferent investing, an informational edge is available to investors with access to critical alternative data sets and the resources and infrastructure to process them using proprietary techniques. Examples include advanced inference techniques to detect retail trades among exchange or broker trading data and applying natural language processing techniques with deep learning models to text or audio data from news, earnings calls or analyst reports to assess the sentiment of different investor types and company management.

Overall, alternative data assumes greater importance in markets whose complexity and inefficiency make it harder for investors to access valuable information. Quant strategies with the tools to capture this data and derive actionable insights from it can potentially expand the alpha opportunity set available to investors.

5) How important are the intuition and expertise of active managers in data-driven investing? It is vital to have an experienced professional at the wheel?

At Goldman Sachs Asset Management, we believe that while technology such as artificial intelligence (AI) can boost investment capabilities, it is also important to understand the risks involved and arrive at a balanced implementation strategy. Our investment signals are always based on an underlying economic hypothesis and rationale. Systematic investment models incorporate a powerful engine that can scan thousands of companies at once, but they still need an experienced operator. Machines are adept at identifying complex patterns across vast amounts of information, but they cannot fully account for sudden market shifts, changes in government policy, or the unpredictability of human behavior.

Human expertise is vital because portfolio managers provide the contextual understanding needed to interpret real-world dynamics. They act as a critical safeguard, ensuring that the investment models aren't being misled by data errors or patterns that won't repeat in the future, and intervening to address risk events that are not captured by the data. By combining the analytical speed of technology with human intuition, the investment process becomes more flexible and better at spotting risks. This partnership ensures that every investment decision is backed by both rigorous data and a coherent, sensible strategy.

1 “End of Era: Passive Equity Funds Surpass Active in Epic Shift,” Bloomberg News. As of September 11, 2019.

2 Goldman Sachs Asset Management, Goldman Sachs Global Investment Research. As of September 2025.

3 Goldman Sachs Asset Management. As of December 31, 2025.

4 Goldman Sachs Asset Management, eVestment. As of December 31, 2025. Data retrieved on February 2, 2026.