Hedge Funds' Role in Today’s Market Environment

Key Takeaways

Why Hedge Funds Matter Now

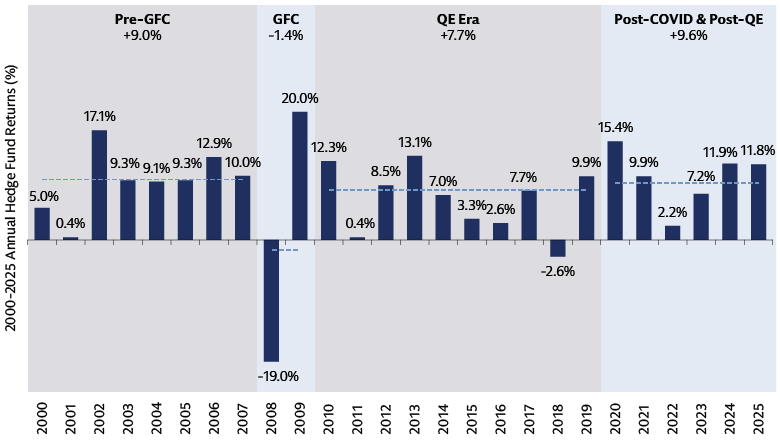

For nearly two decades following the global financial crisis (GFC), quantitative easing, falling interest rates, and low volatility favored traditional long-only portfolios while challenging hedge funds. We believe that era is over.

Source: HF performance: Goldman Sachs Marquee Connect & Goldman Sachs Prime Insights & Analytics analysis. All data as of January 16, 2026, except where otherwise noted. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

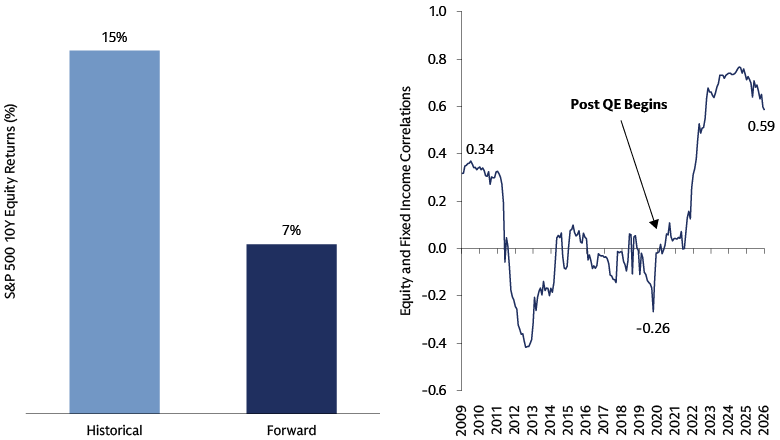

In this new market regime, lower forward return expectations (on most long-only asset classes in both public and private markets) and rising equity-to-fixed-income correlations have increased drawdown risks for traditional 60/40 portfolios, as allocators are not getting the same hedge from fixed income. Consequently, we believe uncorrelated hedge fund returns driven by manager skill and flexibility have become both more valuable and achievable. This shifting dynamic, combined with increasing and broadening allocator demand, creates a highly favorable backdrop for hedge funds.

Source: Goldman Sachs Asset Management. Left-hand Chart: Goldman Sachs Multi-Asset Solutions and Standard & Poor’s as of August 31, 2025. Historical refers to trailing ten years and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. Right-hand Chart: MSCI and Bloomberg as of May 31, 2026. Equities defined as MSCI World NR(USD) and Fixed Income defined as Barclays Global Aggregate TR USD. Past correlations are not indicative of future correlations, which may vary.

The investment backdrop is not only making uncorrelated hedge fund returns more valuable but also potentially more achievable. Macro uncertainty, divergent central bank policy, geopolitical fragmentation, and structurally higher interest rates have contributed to wider performance dispersion both within and across markets, thereby enhancing the potential for alpha generation. Traditional long-only strategies (both passive and active) have become increasingly insufficient to meet investor objectives. These limitations are driven by heightened market concentration in passive indices, which may subsequently impact benchmark-aware long-only active management.

In addition to the improved market backdrop, we believe the hedge fund industry has evolved to better deliver frequent, uncorrelated alpha via improved risk, portfolio construction, business, and talent acquisition practices.

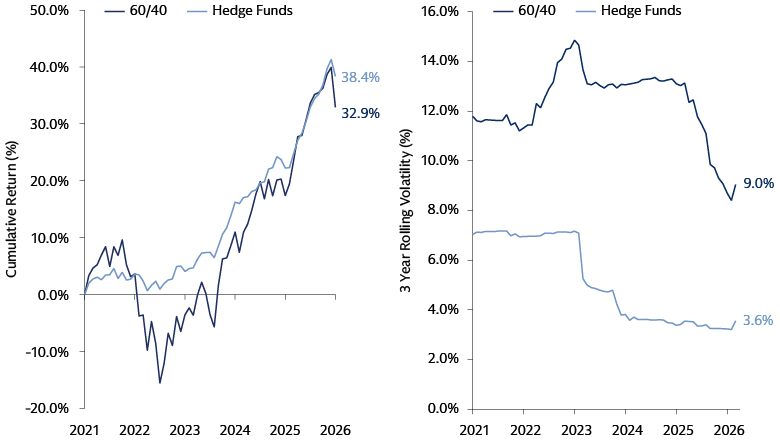

The combination of these two forces has been translated into improved returns for hedge funds. Since the end of quantitative easing in 2022, hedge funds have outperformed a traditional 60/40 portfolio, with significantly lower volatility, reinforcing their role as a portfolio stabilizer in a more uncertain environment.

Source: Goldman Sachs Prime Services, MSCI and Bloomberg as of March 2026. “Hedge Funds”: Pivotal Path Composite Index. “60-40”: 60% MSCI World NR USD + 40% Barclays Global Aggregate TR USD. Performance is shown net of all fees/expenses. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur. Net performance reflects the deduction of all fees and expenses that a client or investor has paid or would have paid in connection with the investment adviser’s investment advisory services to the relevant portfolio, including advisory fees.

New Buyers, New Structures

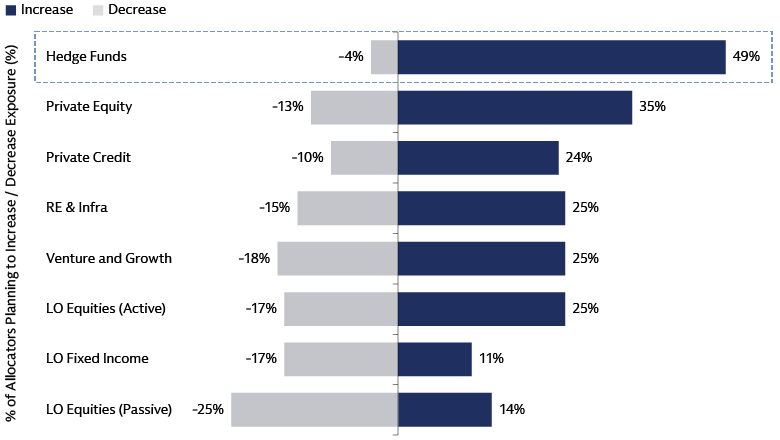

Investor demand is increasingly reflecting these shifting market dynamics. The hedge fund industry saw $116 billion in inflows in 2025, the highest since pre–Global Financial Crisis, with approximately 49% of allocators planning to increase their exposure.

Source: GS Prime Insights & Analytics Allocator Survey. As of January 16, 2026.

While institutional allocator interest has been increasing, demand has also broadened to include traditional long-only investors seeking more capital-efficient ways to enhance returns and improve diversification. Specifically, for allocators seeking higher net exposure, we believe active extension and portable alpha solutions serve as highly efficient mechanisms to achieve beta-1 exposure. These long/short beta-1 solutions may allow investors to blur the lines between traditional hedge fund structures and long-only allocations, while potentially capturing valuable, uncorrelated alpha.

From Conviction to Implementation

In our view, the convergence of a more favorable alpha environment, evolved hedge fund practices, and broadening allocator demand provides a compelling long-term outlook for hedge funds. As traditional portfolios face structural headwinds, hedge funds may offer a vital source of uncorrelated returns and portfolio stability. While the case for hedge funds is compelling, implementing hedge fund exposure may be more challenging.

We believe investors are navigating a structural transition in markets—one where lower beta returns, higher macro volatility, and reduced diversification from traditional assets are likely to persist relative to the prior decade. At the same time, allocator demand is broadening, access to top managers is becoming more constrained, and the dispersion opportunity set remains elevated. In our view, these dynamics collectively support a stronger strategic case for hedge funds to potentially unlock customized liquidity, enhanced transparency, and differentiated return streams.

We will continue to explore this topic and the alternative implementations tools available including funds of hedge funds, hedge fund replicators as well as alternative access points, including separately managed accounts (SMAs) and co-investments.

We are here to help you unlock the hedge fund opportunity and strengthen your portfolio.

1 GS Prime Insights & Analytics Allocator Survey. As of January 16, 2026. GS Prime Insights & Analytics Allocator Survey. The GS Prime Insights & Analytics team conducted an interview with multi-manager firms. For the purposes of this study, they identified a group of nearly 40 managers managing a little over $300 billion. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur. This material is for discussion purposes only and does not purport to contain a comprehensive analysis of the risks / rewards of any idea or strategy.