Learnings from Earnings

Key Takeaways

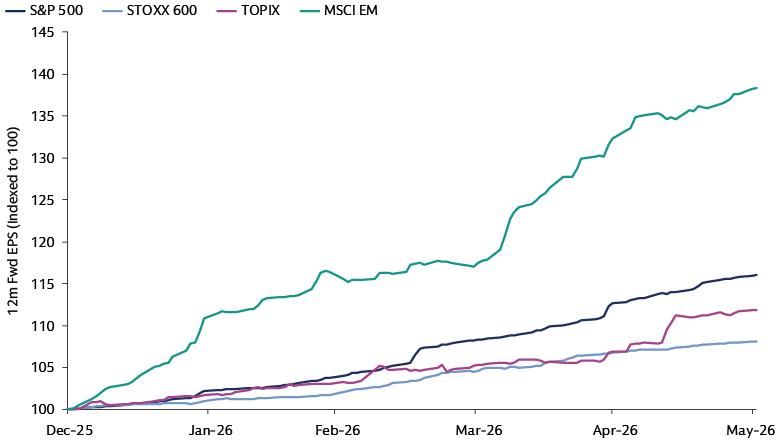

The first-quarter earnings season proved to be one of the strongest in recent S&P 500 history. Year-on-year, aggregate EPS growth reached nearly 30%, marking the fastest pace since the fourth quarter of 2021. Positive surprises were widespread, with 85% of S&P 500 companies exceeding EPS expectations and 81% surpassing revenue forecasts. The corporate strength is broad – while the IT sector led with gains of approximately 50%, non-tech sectors also delivered robust performance, posting around 20% growth on average.1 Here we share three key observations beyond the headline beats.

Source: Goldman Sachs Asset Management, Bloomberg. As of June 2, 2026.

The K-Shaped Consumer: Moving from Broad Exposure to Selective Insulation

The gap between income cohorts continues to widen. The high-income segment, which drives ~40% of total consumption, remains remarkably resilient, bolstered by a $15 trillion increase2 in US household net worth and 6% wage growth.3 This resilience is evident in the strong performance of premium brands, where price is not a factor, and luxury travel providers. In contrast, low-income consumers are under significant pressure due to lower wage growth (1–2%) and the rising costs of essentials like gas and groceries. This stress is showing up as declining traffic at value-oriented establishments and increased price sensitivity at entry-level brands.

The consumer base remains stable overall, despite a more pronounced K-shaped divergence—but foot traffic trends, fluctuating costs, and operational execution are becoming more important. Companies face volatility in energy, freight, and tariffs, balancing margin protection with reinvestment. Growth depends more on transaction volume than ticket size, making traffic unpredictable. Margins stay strong through cost control and productivity, not price increases, highlighting execution over broad trends. Results now vary by company, with execution taking precedence more than general consumer patterns.

In this stock-picker’s environment, we are prioritizing operational alpha over macro beta. We look for companies that protect margins through cost discipline and productivity, without passing costs to the consumer.

The Post-Pricing Era: Prioritizing Strategic M&A

The recent surge in M&A activity is a testament to the positive business sentiment, underpinned by the boom in corporate earnings. Having moved past the post-Covid adjustment phase, we are entering a new era defined by AI implementation and structural expansion. While some deals retain defensive character (for example, to mitigate the impact of buyers’ switch from purchasing premium, national brand-name products to buying cheaper, retailer-owned store brands, or deals in response to the rising adoption of GLP-1 drugs), management teams increasingly use robust balance sheets to proactively capture long-term megatrends.

Today’s dealmaking is characterized by a strategic "refocusing" of corporate portfolios. Leading firms are disposing of adjacent or non-core divisions to sharpen their competitive edge and gain scale within their chosen high-growth verticals. This shift seeks to ensures that M&A is a vehicle for securing technological leadership and differentiated value in a rapidly evolving macro environment.

Highlights of the recent deal activity include:

Hubbell acquired NSI Industries for $3 billion to expand its electrical solutions for data centers,4 while Credo purchased DustPhotonics for $1.3 billion to lead the optical transceiver market.5

Ligand Pharmaceuticals and Neurocrine Biosciences are acquiring assets to strengthen their royalty platforms and pipelines, positioning themselves for the next biotech growth cycle.6

Firms like Watsco and CACI continue to pursue acquisitions to deepen their specialized capabilities and distribution networks.7

This expansion is being executed with a clear commitment to continued balance sheet stability, which in our view signals a sophisticated approach to driving long-term earnings power.

AI Infrastructure: The Transition from Tech Trade to Industrial Reality

The AI capex cycle is broadening far beyond the initial hyperscaler surge. The scale of the investment is unprecedented, with hyperscalers including Microsoft and Alphabet (Google) guiding toward further massive increases in capex in the second half of 2026 and into 2027.8 We remain discerning about which firms are translating this spend into tangible returns and favor companies that can offset higher depreciation and component costs through disciplined headcount management and operational efficiency.

We observe a broadening of the hardware stack as AI adoption moves into enterprise and sovereign cloud customers. The focus is shifting toward the "picks and shovels" of the semiconductor supply chain that may benefit from physical and operational constraints. We are constructive on the memory sector, where the move toward binding Long-Term Agreements (LTAs) is a significant structural shift that reduces historical volatility and may provide some support to valuations. Furthermore, we see opportunities in advanced packaging and testing where lead times of ~12 months and cleanroom availability act as a protective moat for revenue visibility into 2027.

Perhaps the most striking observation this season is how AI demand is revitalizing the industrial and utility sectors. The AI boom is no longer confined to the digital realm; it is driving a cyclical recovery in the physical infrastructure required to power and cool the next generation of data centers. We see opportunities in the "physical layer" of the AI cycle, where companies are often throughput-constrained rather than demand-constrained. We like applied heating, ventilation, and air conditioning (HVAC) and cooling, where we observe market leaders posting consecutive quarters of triple-digit order growth.9 We view the utility sector as a primary beneficiary of this trend. We are also constructive on some companies in building materials, where a significant volume surge in data center segments highlights that the AI buildout is a key driver of non-residential construction strength.

1 FactSet. As of May 30, 2026.

2 Bank of America. As of May 6, 2026.

3 Citigroup. As of May 22, 2026.

4 Hubbell. As of May 4, 2026.

5 Credo Technology. As of May 28, 2026.

6 Ligand Pharmaceuticals. April 27, 2026. Neurocrine Biosciences. As of May 28, 2026.

7 Watsco. As of June 2, 2026. CACI. As of March 9, 2026.

8 Microsoft. Alphabet. Company statements. As of April 29, 2026.

9 Goldman Sachs Asset Management. Fundamental Equity Research. Company statements. As of June 3, 2026.