Pension Review “First Take”

Pension Power

Despite a year marked by significant macroeconomic and market uncertainty, US corporate defined benefit (DB) pension plans demonstrated notable resilience in 2025. Plan sponsors navigated a complex environment shaped by rising tariffs, disruption due to rapid advances in artificial intelligence, and heightened geopolitical tensions, all of which contributed to volatility across global financial markets.

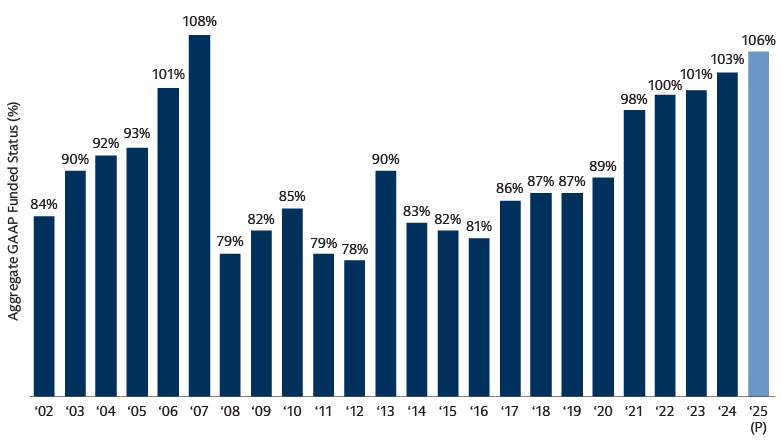

Yet, against this backdrop, pension funding levels rose again in 2025, marking the fourth consecutive year the system has ended in a fully or over-funded position. By several measures, the overall system has never been in better shape. Funded levels are hovering near their highest point this century and plan assets are better aligned with liabilities than they had been in the past given the increased adoption of liability-driven investment programs.

In addition, many DB plans are much smaller today in relation to the operations of their sponsors. This mitigates the potential for notable financial risk for sponsors from their DB plans.

As a result, US corporate DB plans today stand in a position of relative strength compared with prior periods. This strong funding backdrop is shaping a new set of strategic considerations for plan sponsors, including opportunities to further reduce risk, evaluate endgame strategies, and reassess the role of pensions within broader retirement programs. In some cases, it has led some plans to re-risk, potentially with an eye towards utilizing funding surpluses in the future.

Of course, the volatile start to 2026, driven in no small part by further geopolitical tensions, has served as another reminder that positions of strength can evaporate quickly if a sound pension risk management strategy is not in place.

What We Saw in the Data

As this is the 24th year of our annual review, we have developed a robust and consistent data set that allows us to provide detailed analysis across a wide range of pension‑related topics.

Source: Goldman Sachs Asset Management and company reports as of FY 2025. Based upon the US (when specified) defined benefit plans of S&P 500 companies. For illustrative purposes only. The 2025 (P) figure is preliminary and is derived from the “First Take” population. Past performance does not guarantee future results, which may vary.

A sample of the data sets analyzed includes:

- Impact of Positive Asset Returns on Higher Funded Levels

- Relationship between Asset Returns and Strategic Long-Term Expected Return on Assets (EROA) Assumptions

- Asset Allocation Strategies for Each Plan’s Different “End State”

- Potentially Attractive Entry Point for De-Risking Actions based on Historical Discount Rates

- US Pension Plan Materiality to the Plan Sponsor

Our full report includes our views on additional data sets as well as what we are watching for 2026. The company-specific data underlying this analysis, including information on funded levels, asset allocation and actuarial assumptions, are also included in the appendix of the report.