2026 US Corporate Pension Review and Preview

Towards A New Tipping Point

A year ago, we highlighted that the US defined benefit (DB) system was at a tipping point. Sustained high-funded levels had strengthened many plans, prompting sponsors to explore strategic asset allocation shifts like adding to liability-hedging fixed income allocations, full or partial PRTs, or new governance models such as OCIO engagements. Some of those actions played out in 2025.

Entering 2026, we believe the DB system is at a new tipping point, poised around whether corporate DB plans could have a role in American retirement, or continue to shrink due to closures, freezes, PRTs, and accelerating benefit payments as more participants retire. In our view, DB plans can play a vital role in securing worker retirements and allow plan sponsors to deliver benefits in a cost-effective way, through policy changes and sponsors’ willingness to embrace new plan designs play an important role in these decisions.

Many overfunded plans face regulatory constraints on economically accessing their surplus. Trade groups like the American Benefits Council (ABC) and the Committee on Investment of Employee Benefit Assets (CIEBA) advocate for loosening these restrictions, enabling sponsors to use surplus for other employee benefits, such as medical costs related to current employees or defined contribution (DC) retirement plans. We believe greater flexibility in utilizing surplus would significantly incentivize some organizations to maintain their DB plans.

Despite the corporate DB system’s overfunded status and the minimal risk many of these plans pose to their sponsors, flat-rate premiums due to the Pension Benefit Guaranty Corporation (PBGC) continue to rise annually, as required by law. The PBGC’s single-employer program is itself overfunded, and projects further surplus growth. These premiums provide an incentive for some plan sponsors to remove participants from their plans through PRTs, and disincentivize opening a plan to new participants. Actions by Congress to cap or reduce these premiums, as advocated by ABC and others, may help sustain those DB plans.

Sponsors themselves could also consider plan design changes that would be mutually beneficial for the corporation and plan participants. For example, surplus can fund future DB service accruals, a common strategy used by sponsors that still offer a DB plan to at least part of its employee population. But if a plan is frozen, accessing that surplus to fund new benefits would require re-opening that plan. Following IBM’s lead several years ago, a few sponsors have re-opened DB plans to utilize surplus.

A robust DB system can help complement defined contribution (DC) offerings, as well. Importantly, the financial services industry remains focused on services and products to help DC participants generate a steady stream of income in retirement. Our work suggests that one of the most cost-efficient methods of achieving this (both from a participant and employer perspective), may be to allow DC participants to roll some or all their assets into a DB plan to “purchase” an annuity.

Our estimates suggest this strategy could allow retirees to generate about 20% more annual income than if they purchased an annuity through the retail market, with minimal sponsor cost, delivering more value to their employees without increasing any benefits through higher DC matching contributions, for instance.

Glancing Back

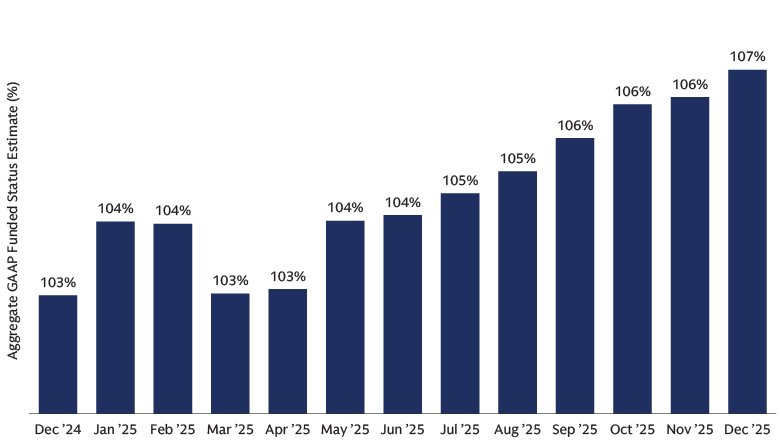

Funded status likely crept higher in 2025 and we are closing in on the highest funded levels since the global financial crisis

Robust global equity market returns and liability hedging programs, which offset the rise in liabilities from falling interest rates, boosted funded levels once again in 2025. As seen below, we estimate the aggregate funded status of the US corporate DB system crept higher during the year, ending around 107% funded, up from 103% at year-end 2024. Over the coming weeks, as annual 10-K reports are filed with the Securities and Exchange Commission, we will compile data on actual funded levels, asset allocations, and actuarial assumptions as part of our “First Take” annual pension review.

Source: Goldman Sachs Asset Management and company reports. As of December 2025. Based upon all the US (when specified) defined benefit plans of S&P 500 companies. For illustrative purposes only. All figures are estimated and unaudited as of December 31, 2025, and are subject to potentially significant revisions over time. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

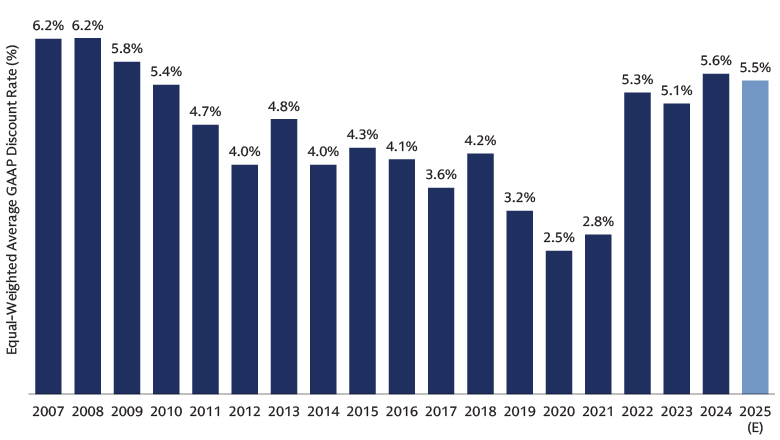

Funded levels are likely up despite discount rates likely down

This improvement in funded levels occurred despite many plans likely needing to lower their GAAP accounting discount rate at the end of 2025. Liability hedging programs did their job in 2025, helping to offset increases in liabilities from lower interest rates. Given declines in interest rates during 2025, we expect companies that file their annual 10-K reports at calendar year-end likely lowered their accounting discount rates by around 12 basis points in 2025.

Source: Goldman Sachs Asset Management and company reports. As of FY 2025. Based upon the arithmetic average of US plan discount rates (when specified) of S&P 500 companies with December fiscal year-ends. For illustrative purposes only. The 2025 (E) figure is estimated and unaudited as of December 2025 and is subject to potentially significant revisions over time. The economic and market forecasts presented herein are for informational purposes as of the date of this presentation. There can be no assurance that the forecasts will be achieved. Please see additional disclosures at the end of this presentation.

Pension risk transfer slowed in 2025 – a pause or a re-setting of strategy?

PRT activity slowed in 2025, both in transaction counts and cumulative dollar amount consummated. There have been ongoing lawsuits concerning certain PRT transactions that continue to work their way through the courts.

In addition, while many sponsors couldn’t wait to terminate their plans when they were only 80% funded many years ago, some may now be reconsidering that endgame goal as their plans become overfunded, require no contributions, and generate pension income. Any loosening of rules around the use of surplus assets could further incentivize sponsors to maintain their DB plans. It remains uncertain whether the slowdown in PRT activity in 2025 is a temporary pause or a strategic reset, which may see some conclude that maintaining (rather than transferring) pension obligations makes more sense.

Source: LIMRA US Group Annuity Transfer Study and Goldman Sachs Asset Management. As of Q3 2025 (latest available). 2025 data is year-to-date through September 30, 2025.

Looking Forward

Cutting and Pasting from Last Year

We believe our previous year’s suggestions, some proving prescient, remain highly relevant as we enter 2026.

Last year, we indicated that sponsors may want to increase hedging of their interest rate and credit spread risk, given the well-funded nature of many plans. This played out well in 2025, as interest rates fell and credit spreads remained relatively unchanged year-over-year. Consequently, GAAP accounting discount rates for corporate pension plans will likely fall around 10 basis points, in our estimation. Robust hedging programs by many sponsors enabled them to offset increases in liabilities in 2025 due to lower discount rates.

We would encourage plans that have not leaned into hedging more of their interest rate and credit spread risk to consider doing so in 2026. The future path of Fed rate movements in the US would appear to be lower rather than higher, and strong corporate balance sheets should keep credit spreads well-behaved. Given the aforementioned improvement in funded levels that we believe occurred in 2025, protecting those gains should take precedence for many sponsors.

Last year, we also suggested diversifying the growth portfolio away from large cap US equities as we expected to see a broadening out of the equity market. Investors in non-US equity markets, both developed and emerging, were rewarded by taking such actions. We foresee continued strong performance for international equities in 2026, driven by European fiscal reforms, attractive valuations relative to US equities, high dividend yields, and expected Fed rate cuts (twice in 2026).

As part of this diversification, we also anticipated a strong year for US small-capitalization stocks. While they performed well recently with the Fed's easing cycle, they lagged large caps in 2025. However, we believe 2026 is ripe for small-cap outperformance, supported by higher expected earnings growth and a projected revival in the M&A market, where smaller companies are often targets.

Finally, we also encouraged plan sponsors to evaluate their governance models given the growth of the OCIO market. Several large, high-profile organizations engaged OCIO providers in 2025, and we expect that momentum to continue into 2026.

Some of that may be spurred by succession issues as some pension managers and Chief Investment Officers retire without a natural in-house replacement. In other cases, sponsors may recognize the size of some OCIO providers enables them to have significantly more pricing power with external asset management organizations than the DB plans themselves.

Read our 2026 Investment Outlook for more views from our asset management investing teams.